In 2025, private equity and venture capital deployed more capital into global aerospace and defense assets than in any previous year on record surpassing the prior peak by nearly 60%. Yet at the same time, traditional M&A deal volumes in the sector have declined. It is the signature of a market undergoing deep structural transformation and the organizations that read that signal clearly will define the competitive landscape for the decade ahead.

A Record That Rewrites the Rules: The New Architecture of Defense Capital

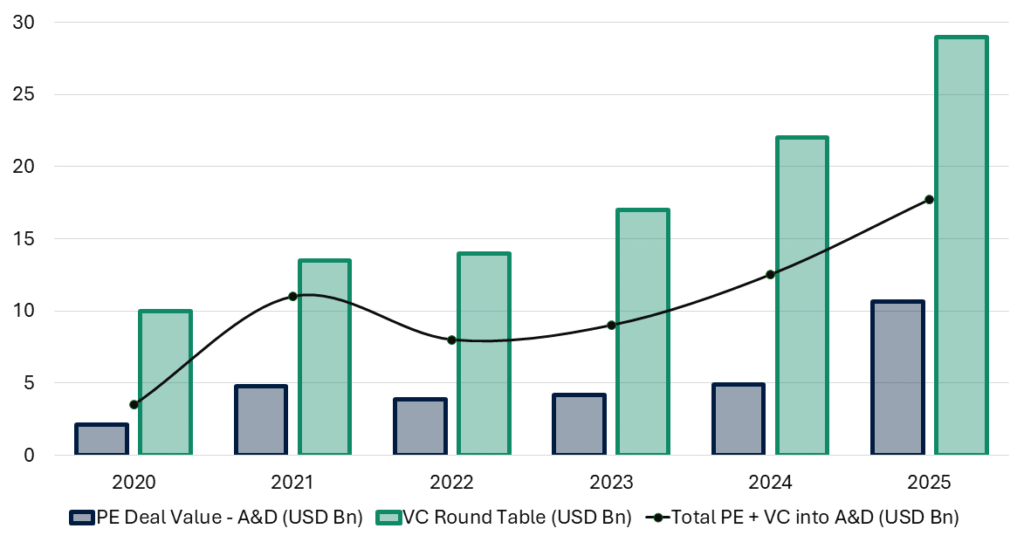

The global defense capital market has entered a phase that has no historical precedent. Private equity and venture capital investment in aerospace and defense reached $17.7 billion in deal value through November 2025 already exceeding the previous full-year record of $11 billion set in 2021. Venture capital transaction counts climbed to a peak of 629 deals in 2024, up from 414 in 2020, with round values reaching $29 billion in 2025 nearly triple the 2020 total. They represent a structural rerating of defense as a mainstream asset class for global institutional capital.

Classic strategic combinations among legacy defense suppliers have moderated from their 2021 peaks, with deal counts and values declining as the pool of large transformational targets has narrowed. The market has not slowed but it has bifurcated. Private equity is building new platforms from the ground up; strategic buyers are repositioning through carve-outs, minority stakes, and enterprise partnerships rather than traditional full acquisitions. Understanding which mode applies to your organization is the first and most consequential strategic decision any defense entity faces in 2026.

Five Structural Forces Driving the Global Defense Tech M&A and Private Equity

Five interlocking forces explain why defense technology has become one of the most actively pursued asset classes in global private markets and why that dynamic is self-reinforcing rather than speculative.

The geopolitical demand shock is real and multi-year. NATO’s estimated total defense expenditure crossed $1.4 trillion in 2025. Europe alone is projected to increase collective defense spending by an additional €300 billion by 2030, reaching approximately €800 billion, a trajectory driven not by political choice but by a security environment that has materially and permanently changed. This is the foundation beneath every valuation model in the sector.

Innovation gaps at incumbent organizations are structural, not cyclical. Traditional prime contractors, i.e. engineering-intensive organizations built around hardware integration and long-cycle program delivery cannot develop artificial intelligence, autonomy, cyber, and mission software capabilities at the pace that modern warfare demands. Acquisition is not one path to speed. In most cases, it is the only viable path. That reality sustains deal flow irrespective of macroeconomic conditions.

Portfolio rationalization is releasing assets. As large conglomerates refocus on their highest-priority programs, they are divesting businesses that were once considered strategic but are no longer central to their competitive position. These carve-outs, often well-managed, profitable, and undercapitalized, represent the most attractive entry point for private equity buyers capable of executing complex separations and accelerating growth in standalone structures.

Procurement reform is lowering the barrier to entry. Defense acquisition frameworks across United States, United Kingdom, and Europe have been materially updated to facilitate participation by non-traditional contractors. This structural change means that a defense-tech startup or a PE-backed platform can win government contracts on the basis of capability rather than historical contractor status fundamentally changing the risk calculus for private investment.

Private equity dry powder is seeking yield in durable, government-backed revenue streams. In a world of compressed returns across traditional asset classes, defense offers something rare: multi-year government contracts, high switching costs, and performance characteristics largely decoupled from consumer sentiment or commodity cycles. For institutional allocators under return pressure, this combination is highly attractive.

How Private Equity Is Playing the Defense Technology Opportunity

The preferred entry mode is the carve-out. As prime contractors and diversified industrial groups rationalize portfolios, the assets they release such as defense electronics divisions, maintenance and repair operations, mission software businesses, test and measurement units are precisely the type of high-margin, recurring-revenue, government-contracted businesses that PE underwriting models find most compelling. These assets arrive with established customer relationships, certified supply chains, and often with multi-year contract backlogs reducing the revenue uncertainty that typically inflates required returns in other sectors.

The preferred target profile combines three characteristics: dual-use capability, structural defensibility (high switching costs, regulatory certification requirements, or classified technology that creates durable competitive moats), and a growth thesis anchored in government spending commitments that are visible several years forward. Assets that demonstrate all three routinely command premium multiples and attract competitive processes.

Deal Value Growth in Global Defense Tech Private Capital Investment (2020–2025)

The geographic dimension of PE’s defense pivot is equally notable. In Europe, a market that was largely inaccessible to general PE funds due to mandate restrictions on defense investment, a new generation of defense-focused vehicles is being raised specifically to capture the rearmament opportunity. European PE and VC deal value in the sector rose approximately 4.8 times year-over-year in 2025, reaching $658.8 million. New funds are being launched across United Kingdom and continental Europe with investment mandates explicitly designed to support the defense industrial base.

PE funds are also increasingly co-investing alongside strategic buyers structuring deals that give PE access to the government customer relationships and integration expertise of incumbent contractors, while giving strategic access to PE’s capital flexibility and carve-out execution capability. This model, the PE-strategic co-investment, is emerging as the dominant deal architecture for mid-market defense transactions globally.

Strategic M&A: How Primes and Technology Leaders Are Acquiring Defense Innovation

Globally, aerospace and defense M&A recorded nearly 250 transactions in first half of 2025, up from 175 in the second half of 2024 with strategic buyers accounting for nearly 70% of transactions. Cross-border deal activity increased approximately 27% quarter-over-quarter in early 2025, reflecting the genuinely global nature of the capability gaps being addressed. The focus areas are consistent across acquirer geographies: artificial intelligence and machine learning, autonomous systems, cyber resilience, electronic warfare, and the software platforms that integrate these capabilities into operational architectures.

The structural shift in how primes are approaching capability acquisition deserves particular attention. Rather than pursuing full acquisitions that trigger lengthy integration cycles and CFIUS review timelines, leading buyers are pioneering a new deal architecture: the enterprise partnership agreement. Under this model, a strategic buyer consolidates dozens of previously separate contracts into a single, long-term framework that establishes fixed terms, pricing, and rights giving the buyer platform-level access to a supplier’s evolving capabilities without triggering formal acquisition review. This model accelerates capability access, reduces regulatory friction, and creates a structured pathway to full acquisition as the relationship matures.

In the space economy, deal strategy is increasingly oriented around vertical integration. Acquirers are targeting assets that span satellite manufacturing, launch, ground systems, and services recognizing that capability in any single segment is insufficient when end-to-end value chain control determines competitive position. This consolidation logic applies to both commercial space and government-contracted capabilities, and the two markets are increasingly overlapping as dual-use satellite architectures become standard.

The Valuation Reality: Premium Multiples, Elevated Expectations, and the Credibility Premium

Average transaction multiples in defense M&A have risen from approximately 13 times EBITDA in 2021 to above 20 times in 2025. In United States, median sector multiples over the twelve months through the third quarter of 2025 stood at 17.82 times enterprise value to EBITDA and 3.22 times enterprise value to revenue, across 122 transactions.

Most buyers are no longer valuing assets on the basis of trailing twelve-month earnings. They are underwriting forward EBITDA, building financial models anchored to projected 2026 and 2027 earnings that reflect anticipated contract wins, production ramps, and program escalations. In a sector where multi-year government contracts provide genuine earnings visibility, this approach is defensible. But it places enormous weight on forecast credibility, and assets that cannot demonstrate the quality of their backlog distinguishing funded from unfunded commitments, cost-plus from fixed-price contracts, program-of-record status from discretionary spending will face aggressive challenge in due diligence.

Supply chain resilience has emerged as a new and direct valuation variable. Buyers are conducting component-level provenance analysis by mapping exposure to geopolitically constrained materials, rare earths, and electronics from restricted jurisdictions. Assets that can demonstrate clean sourcing, alternative supply relationships, and documented re-shoring plans command demonstrably higher multiples than comparable businesses with unresolved supply chain exposure.

The Regulatory Minefield: Navigating CFIUS, the COINS Act, and the Global FDI Landscape

The regulatory environment surrounding defense technology transactions has become one of the most complex and consequential deal variables in the global M&A landscape. In United States, the national security review framework has expanded materially. The most recent national defense authorization legislation significantly broadened the scope of covered transactions, extended review jurisdiction to additional sensitive site categories across more than thirty states, and enhanced the investigative authorities available to the reviewing committee. Critically, the legislation introduced a statutory basis for an entirely new regime governing outbound investment restricting or requiring notification of U.S. capital flows into entities with connections to specified technology sectors in countries of concern. This is not a marginal addition to the existing framework. It creates a new compliance obligation that applies to investment decisions that would previously have received no regulatory attention.

For cross-border transactions, the practical consequences are significant. All defense M&A transactions in Europe in 2025 were domestic deals. Cross-regional combinations were effectively precluded by national security scrutiny, government preference for domestic champions, and the complexity of multi-jurisdictional regulatory pathways. Strategic buyers and PE funds seeking European defense exposure are navigating a market where the most direct routes to scale are either closed or require mitigation structures that materially affect transaction economics.

The European Union’s foreign direct investment screening framework is being expanded with mandatory review requirements for critical sectors, harmonized national procedures, and new powers for the Commission to intervene in transactions that raise systemic concerns. Member states are simultaneously conducting reviews of outbound investments in semiconductors, artificial intelligence, and quantum technology made between 2021 and June 2026 generating a significant compliance and reporting burden for funds with cross-border exposure.

There is, however, a positive development for allied-nation investors. A new pilot program launched in early 2026 is designed to streamline review processes for low-risk, repeat investors from allied countries. Funds that engage proactively with this program stand to gain a meaningful process advantage in future transactions.

Regional Spotlight: Where the Most Compelling Opportunities Lie in 2026

A global perspective on defense technology M&A reveals three distinct opportunity landscapes, each with different deal structures, competitive dynamics, and regulatory frameworks.

North America remains the world’s deepest and most liquid defense technology market, anchored by the largest defense AI budget in history and a procurement reform agenda explicitly designed to accelerate participation by non-traditional technology suppliers. The primary deal themes are AI and software capabilities, autonomous systems, space-based assets aligned to national security priorities, and cyber resilience platforms. The most active deal structures are enterprise partnership agreements, minority stakes by primes in growth-stage technology companies, and carve-outs of non-core divisions by diversified defense contractors.

Europe represents the most rapidly evolving opportunity in global defense M&A where PE market is structurally just opening to defense investment, IPO-ready companies following successful recent public listings, and a growing number of government mandates requiring domestic sourcing. All of these create conditions for a sustained multi-year deal cycle. The key constraint remains target availability: the low historical focus on defense M&A means there are few pure-play assets of relevant scale, and valuation expectations from sellers are elevated relative to the maturity of the assets on offer. Early relationship-building, minority stake strategies, and structured partnerships that create optionality for future full acquisitions are the most effective entry approaches for funds without pre-existing European defense relationships.

Asia-Pacific presents the fastest-growing defense technology market in the world, with Japan, South Korea, India, and Australia all implementing significant defense spending increases alongside industrial policy frameworks designed to develop domestic capability. The primary challenge for non-domestic investors is regulatory: each of these markets has distinct and increasingly stringent foreign investment screening requirements, and the definition of “sensitive” assets is expanding as governments broaden their conception of economic security. For funds with long-term regional ambitions, the investment required to establish compliant structures and government relationships in each market is substantial but the competitive advantage it creates, once established, is correspondingly durable.

Indo-Pacific Signal

Naval readiness investment across the Indo-Pacific spanning shipbuilding, maintenance and repair, and submarine ecosystem development represents an emerging deal catalyst beyond the more widely discussed AI and autonomy themes. Defense organizations with established naval technology capabilities are seeing elevated interest from regional governments seeking to accelerate indigenous capacity development through partnership structures that retain domestic ownership while accessing international expertise.

Conclusion

The confluence of geopolitical demand, private capital deployment, and structural innovation gaps has created a defense technology M&A environment. The record capital flows of 2025 are not the peak of a speculative cycle but they are the opening chapters of a multi-year structural realignment of the global defense industrial base.

Valuation multiple expansion creates its own ceiling. Regulatory frameworks are tightening and will continue to do so. The pool of high-quality carve-out targets will shrink as portfolios rationalize and the first-mover advantages in allied-nation relationship-building accrue disproportionately to the organizations that act before the opportunity is fully visible to the broader market.

For defense organizations, and PE funds, the imperative is the same, i.e. develop the strategic clarity to identify your role in this restructuring (buyer, seller, partner, or platform builder) and invest in the regulatory, financial, and operational preparation that allows you to execute decisively when the right opportunity presents itself.