The Return of Firm Power

The global energy landscape is undergoing a structural shift that few anticipated even five years ago. Nuclear energy, long sidelined by cost overruns and post-Fukushima anxiety, is staging its most significant comeback since the 1980s. Simultaneously, advanced geothermal, powered by drilling innovations borrowed from the shale revolution, is also emerging from lab into the commercial mainstream.

Three forces are driving this convergence: an unprecedented surge in electricity demand from artificial intelligence and data centers, escalating geopolitical urgency around energy security, and binding net-zero commitments that demand firm, carbon-free baseload power that solar and wind alone cannot deliver.

The Demand Catalyst: Why The Urgency Is Real

Global investment in data centers is expected to reach $580 billion in 2025-26, surpassing the $540 billion being spent on global oil supply. Global data center electricity consumption is projected to reach 1,100 TWh in 2026, equivalent to Japan’s entire national consumption. By 2035, this figure could reach 1,300 TWh. In 2026 alone, hyperscalers i.e. Amazon, Google, Meta, and Microsoft are planning to spend nearly $700 billion on data center infrastructure.

This demand is qualitatively different from prior electricity growth. Data centers require uninterrupted, 24/7 power with near-perfect reliability. Solar and wind, while cost-competitive and rapidly scaling, are intermittent. Battery storage helps but remains expensive at the multi-day durations needed for true grid reliability. The result is a structural market opening for firm clean power and both nuclear and advanced geothermal are positioned to fill it.

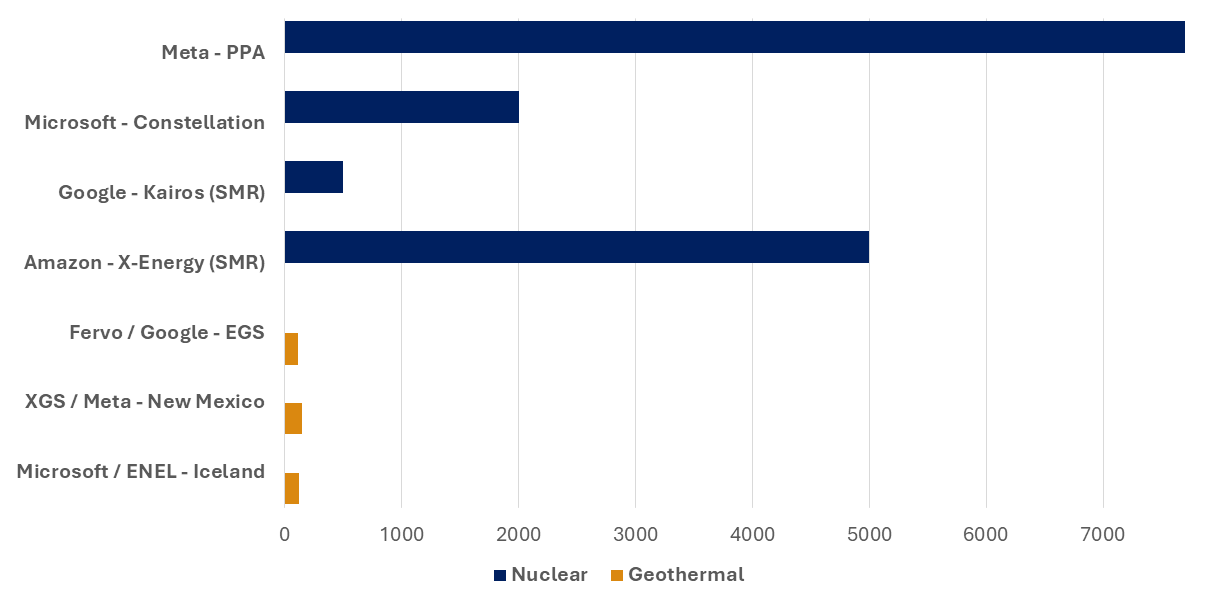

Close to 18% of corporate clean energy deals in 2025 involved nuclear, fusion, geothermal, or hydropower showing a major shift from previous years dominated almost entirely by wind and solar. Microsoft signed a 2 GW nuclear commitment with Constellation Energy through 2040, the largest corporate nuclear agreement in history. Google backed Kairos Power with a 500 MW SMR fleet agreement. Amazon led a $500 million financing round for X-energy’s SMR development, targeting at least 5 GW by 2039. Meta contracted approximately 7.7 GW of nuclear power, more than any other U.S. corporation.

On the geothermal side, technology companies signed 14 geothermal power purchase agreements totaling 635 MW in 2025 alone, a threefold increase from 2024. Data centers now drive an estimated 60% of new geothermal capacity globally.

The Nuclear Renaissance: From Stagnation To Strategic Asset

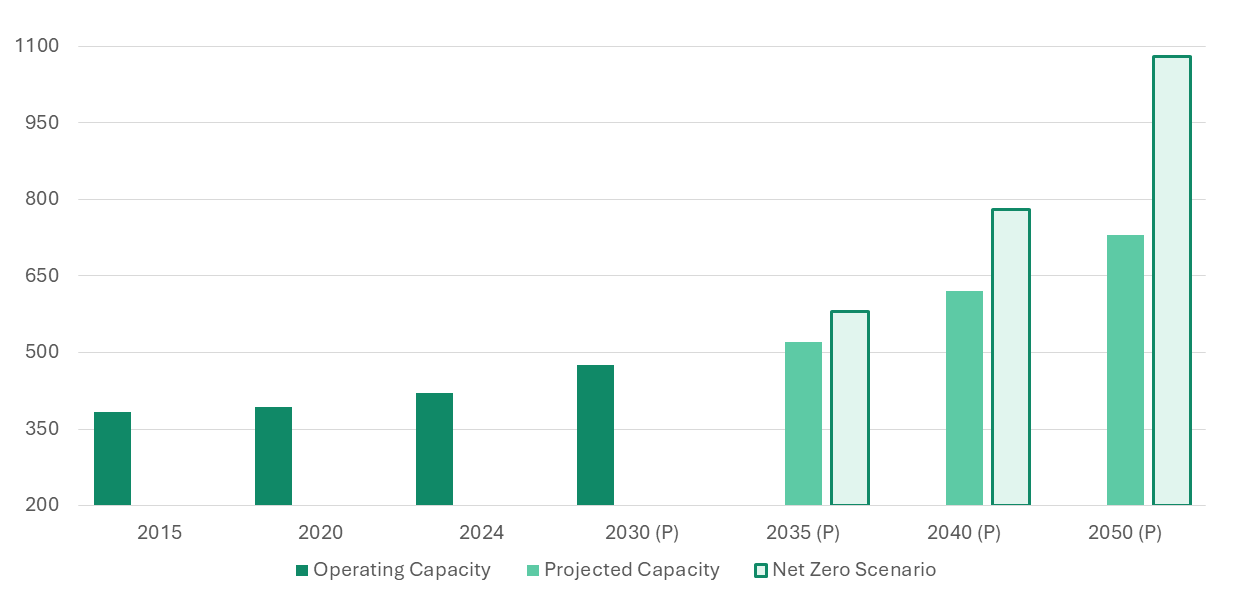

Nuclear energy now provides approximately 9% of the world’s electricity from around 440 reactors operating across 31 countries. More than 70 GWe of new capacity is currently under construction, presenting highest levels in last 30 years. More than 40 countries now include nuclear power in their national energy strategies and approximately 15 reactors to come online in 2026, adding close to 12 GW of new capacity.

Global Nuclear Capacity: Current Pipeline and Projections in GWe

The nuclear revival is not uniform. China is leading the construction wave with 29 reactors under construction, adding to 57 already operating. United States, still the world’s largest nuclear power producer with 94 reactors, has issued executive orders targeting 400 GW of nuclear capacity by 2050, a fourfold increase from current levels. India achieved a historic milestone in April 2026 when its Prototype Fast Breeder Reactor at Kalpakkam attained criticality, becoming only the second country after Russia to operate a commercial fast breeder reactor. The SHANTI Act, passed in December 2025, ended India’s decades-old state monopoly on nuclear energy, targeting 100 GW by 2047.

| Country | Current Status | Key Initiative / Target |

| China | Operating 57, 29 under construction | Linglong One SMR commercial launch expected 2026; world’s largest build-out programme |

| United States | 94 reactors, 97 GWe installed | Executive order: 400 GW by 2050; Palisades restart; DOE $800M SMR funding programme |

| India | 25 reactors, 8.9 GW installed | PFBR criticality (Apr 2026); SHANTI Act; 100 GW target by 2047; 5 SMRs by 2033 |

| France | 57 reactors, 63 GWe | 67% of electricity from nuclear; fleet extension + new EPR2 programme |

| United Kingdom | Hinkley Point C under construction | 24 GWe target by 2050; Nuclear Acceleration Office; SMR deployment via GBN |

| Poland | New entrant | Up to 9 GWe planned by the 2040s; first large reactor + SMR programme |

| Egypt | 4 reactors (4.4 GWe) under construction | First nuclear power plant on the African continent outside South Africa |

Beyond these, a new wave of first-time nuclear nations is emerging. Bangladesh is constructing its first two reactors. Vietnam has revived its Ninh Thuan project. The Philippines is targeting 1.2 GWe by 2032. Kenya, Ghana, and Nigeria are advancing plans with varying timelines. Switzerland, which adopted a post-Fukushima phase-out policy, proposed lifting its ban on new nuclear construction in 2025.

The SMR Frontier

Small modular reactors represent the most watched innovation in the nuclear sector. Seventy-four SMR designs are now in active development worldwide, with 51 in pre-licensing or licensing activities across 15 countries representing a 65% increase in regulatory engagement. At least $15 billion in public and private financing is flowing into the SMR space.

However, commercialization remains nascent. Only two SMRs operate commercially today: Russia’s floating KLT-40S (since 2020) and China’s HTR-PM (since 2023). China’s Linglong One is expected to become the first land-based commercial SMR in the first half of 2026. In United States, DOE is pushing for at least three pilot reactors to achieve criticality by July 2026. India has allocated INR 20,000 crore toward developing at least five indigenous SMRs operational by 2033.

Advanced Geothermal: From Earth’s Crust To The Grid

Conventional geothermal energy, i.e. drawing steam or hot water from naturally occurring hydrothermal reservoirs has been commercially viable for decades but remains geographically constrained. It supplies less than 1% of global electricity, concentrated in a handful of countries near tectonic boundaries: United States, Indonesia, the Philippines, Turkey, and New Zealand.

What has changed is the emergence of next-generation geothermal technologies that can access heat almost anywhere on Earth. Enhanced Geothermal Systems (EGS) use horizontal drilling and hydraulic stimulation techniques adapted directly from the shale oil and gas revolution to create artificial hydrothermal reservoirs in hot, dry rock formations. Superhot Rock (SHR) systems target temperatures above 375°C, where water reaches a supercritical state that could produce up to ten times the power from a single well compared to conventional geothermal. Closed-loop systems, pioneered by companies like Eavor, circulate fluid through sealed underground loops without direct contact with the rock, reducing seismicity risk.

A 2025 study calculated that next-generation geothermal deployed at depths up to 5 kilometers in contiguous United States alone could produce more than 5 terawatts, roughly four times total U.S. generating capacity. Geothermal could meet 15% of global electricity demand growth between 2024 and 2050 if costs continue to decline.

Capital is flowing into geothermal at an unprecedented rate. Financing for next-generation geothermal reached nearly $2.2 billion in 2025, an 80% increase year-over-year with investment estimation of approximately $9 billion by 2030. U.S. Department of Energy announced $171.5 million in February 2026 specifically for next-generation geothermal field-scale tests and exploration drilling.

Three factors are converging to drive this acceleration:

-

-

- Drilling cost reductions of up to 30% from new technologies and real-time downhole sensor data.

- Commercial offtake agreements with data center operators hungry for 24/7 clean power.

- The emerging co-production opportunity: geothermal projects in EU and U.S. could yield 47 kilotons of lithium per year by 2035, meeting 5% of global demand adding a critical minerals revenue stream to the energy economics.

-

Projects Defining the Frontier

Fervo Energy’s Cape Station in Beaver County, Utah, is set to become the first large-scale commercial EGS plant in United States. The first 53 MW phase is scheduled to come online in June 2026, with expansion to 400 MW by 2028. Fervo has signed 320 MW in power purchase agreements with Southern California Edison and a 115 MW agreement with Google via NV Energy.

XGS Energy is constructing a $1.2 billion, 150 MW project with Meta in New Mexico set to expand the state’s geothermal capacity tenfold. The company holds a 3 GW pipeline across the western United States. Mazama Energy is advancing a SuperHot Rock pilot at Newberry Volcano in Oregon, with 2026 plans targeting temperatures above 400°C using supercritical CO₂ drilling.

In Europe, Eavor’s closed-loop geothermal system in Germany became the first commercial advanced geothermal plant to deliver electricity to the grid in December 2025. Vulcan Energy’s Phase 1 Lionheart project in Germany, fully financed in 2025, integrates geothermal heat production with lithium extraction, with offtake agreements from Glencore, Stellantis, and LG Corp.

Microsoft and ENEL have established what is described as the world’s largest geothermal-to-data-center link: a 120 MW supply agreement at Hellisheidi in Iceland, operational in 2026.

The Corporate Power Play: Big Tech as Energy Principals

The entry of major technology companies into nuclear and geothermal procurement represents a paradigm shift in energy markets. These are not exploratory pilot programmes. They are multi-billion-dollar, multi-decade commitments that are restructuring how clean energy projects get financed, built, and operated.

Big Tech’s firm clean energy commitments in MW

AI workloads are power-intensive and must run continuously. A single large language model training run can consume as much electricity as thousands of homes for months. As these companies scale toward exascale computing, they need power sources that are carbon-free, available around the clock, and contractable at scale characteristics that define both nuclear and geothermal.

The Policy Accelerators: Governments Clearing The Path

Governments across the world are enacting legislative and regulatory reforms that would have been politically unthinkable a decade ago.

1. Nuclear Policy Milestones

In the United States, executive orders issued in 2025 target expanding nuclear capacity from 100 GW to 400 GW by 2050, with directives to add 5 GW through upgrades to existing reactors and have 10 newly designed large reactors under construction by 2030. The DOE issued categorical exclusions for advanced nuclear reactors, streamlining environmental review. Two SMR developers, TVA and Holtec, were each awarded $400 million in cost-shared federal funding.

India’s SHANTI Act, passed in December 2025, represents arguably the most transformative nuclear reform in the developing world. By repealing the 1962 Atomic Energy Act and allowing private companies to build, own, and operate nuclear plants, it opens the door to an estimated ₹4-6 lakh crore ($50-70 billion) in potential private investment by 2035.

The European Union has included nuclear in its sustainable investment taxonomy. Switzerland proposed lifting its post-Fukushima construction ban. At COP28, more than 25 nations committed to tripling nuclear capacity by 2050.

2. Geothermal Policy Momentum

Geothermal policy, while less prominent in global headlines, is advancing on multiple fronts. The U.S. DOE announced $171.5 million in February 2026 for next-generation geothermal field tests, with bipartisan legislation introduced to promote superhot rock research and development. Indonesia’s state-owned utility set a 5.1 GW geothermal target in its 2025–2034 investment plan, with 4.5 GW earmarked for private developers.

Mexico enacted 2025 energy law reforms to streamline geothermal development. The Philippines launched new financial incentives including a $250 million facility to stimulate geothermal investment.

A critical enabling factor for both sectors is the growing recognition that “technology-neutral” clean energy policy which gives equal credit to nuclear, geothermal, and renewables is more effective than picking winners. Also, U.S. Inflation Reduction Act’s production tax credits, applicable across clean energy sources, exemplify this approach and have been instrumental in improving project economics for both nuclear and geothermal developers.

Navigating The Headwinds

Enthusiasm must be tempered by the real and persistent risks facing both technologies. Credible analysis requires acknowledgment that neither sector has fully resolved its core challenges.

Nuclear Energy Risks

-

-

- Capital intensity and construction delays remain structural (Plant Vogtle: 15 years, $36.8B)

- HALEU fuel supply bottleneck for advanced SMR designs

- Geopolitical concentration of uranium supply chain: Russia and Kazakhstan dominate enrichment and supply

- Public acceptance and long-term waste management lack resolution at scale

- SMR cost-competitiveness remains unproven; FOAK units likely $90–160/MWh

-

Advanced Geothermal Risks

-

-

- Drilling costs represent up to 80% of total project cost

- Geological Uncertainty: Limited subsurface data in many regions raises exploration risk

- Induced seismicity concerns (the 2017 Pohang incident in South Korea halted a project after a magnitude 5.4 earthquake)

- Zero commercial-scale EGS plants operating as of early 2026

- Current EGS electricity costs remain above conventional renewables

-

For investors and policymakers, the risk calculus must be weighed against the counterfactual: what happens if firm clean power is not deployed at scale? Also, without nuclear and geothermal expansion, meeting net-zero targets becomes significantly more expensive and technically constrained, requiring implausible levels of battery storage deployment or continued reliance on unabated fossil fuels for grid stability.

Strategic Outlook: Positioning For The Firm-Power Era

The combination of AI-driven demand, geopolitical energy security imperatives, and climate commitments has created a structural tailwind that is unlikely to reverse in the near term.

1. For Investors

Nuclear SMRs and enhanced geothermal systems represent high-conviction, long-duration investment themes. The presence of creditworthy offtakers i.e. hyperscalers with multi-decade power needs materially de-risks project finance. Priority should be given to companies with secured PPAs, government cost-sharing, and operational demonstration projects. The uranium supply chain, HALEU fuel production, and geothermal drilling services are adjacent opportunities with nearer-term revenue potential.

2. For Policymakers

Streamlined permitting, technology-neutral clean energy credits, and risk-sharing mechanisms are the three critical enablers. Countries that move early on regulatory reform as India has done with the SHANTI Act, or U.S. with its categorical exclusions for advanced reactors will attract capital and build domestic industrial capacity. Those that delay will find themselves importing technology rather than exporting it.

3. For Corporates

The lesson from Big Tech’s energy procurement strategy is clear i.e. diversification beyond wind and solar is no longer optional for companies with serious decarbonization and reliability commitments. Nuclear and geothermal PPAs provide 24/7 carbon-free baseload that strengthens sustainability credentials, reduces exposure to gas price volatility, and offers long-term cost visibility.

4. For Energy Companies

Oil and gas expertise in drilling, subsurface engineering, large-scale project execution, and safety culture is directly transferable to both sectors. The workforce transition from hydrocarbons to firm clean power is not a threat narrative but it is a strategic opportunity for companies willing to invest early.