In an era where decarbonization imperatives are reshaping energy systems, methane pyrolysis, also termed turquoise hydrogen, emerges as a pivotal technology for bridging fossil fuel dependencies with renewable futures. Methane pyrolysis is not merely a hydrogen production method but its a strategic enabler for achieving net-zero targets while unlocking new value chains in carbon materials.

This process thermally decomposes methane (CH4) into hydrogen gas and solid carbon, eliminating direct CO2 emissions and producing a valuable byproduct, solid carbon, that can be sequestered or commercialized. Unlike steam methane reforming (SMR), which dominates current hydrogen production and emits 9-12 kg CO2 per kg of hydrogen, pyrolysis offers a low-carbon alternative with energy requirements as low as 7-12 kWh per kg of hydrogen. However, methane-pyrolysis outcomes are highly sensitive to upstream methane leakage and electricity source; lifecycle GHG estimates range widely.

Technical and LCA Realities

-

-

- Process: high-temperature decomposition of CH₄ → H₂ + C (solid). Multiple reactor types (plasma, catalytic, Joule-heating, molten metal) are in development.

- Energy intensity: SMR ~44.5 kWh/kg H₂; electrolytic low-emission electrolysis ~50 kWh/kg H₂; methane pyrolysis reported as low as ~7–12 kWh/kg H₂ in some experimental assessments, depending on process and heat integration. Methane pyrolysis therefore often shows lower electrical energy demand than electrolysis but requires careful heat/electricity balance.

- Emissions: SMR without abatement emits roughly 9 to 12 kg CO₂-eq/kg H₂ (point-of-production). Life-cycle greenhouse-gas results for methane pyrolysis vary: peer-reviewed LCAs report spans from ~0.8 to >8 kg CO₂-eq/kg H₂, driven primarily by upstream methane leakage, transport of feedstock, and electricity source for reactor heating. Policy-grade assessments warn that lifecycle emissions must be audited to claim low-carbon credentials.

-

Comparative Analysis of Methane Pyrolysis Technologies

|

Technology Type |

Operating Temperature |

Key Characteristics |

|

Plasma Pyrolysis |

1,000°C – 2,000°C |

Highest TRL; High electricity input (25-30 kWh/kg H2); Produces carbon black |

|

Catalytic Pyrolysis |

600°C – 900°C |

Lower temperature; Catalyst deactivation challenges; Produces graphite/CNTs |

|

Thermal Pyrolysis |

>1,200°C |

No catalysts; Various heating methods; Balance of H2 volume vs. carbon quality |

Methane Pyrolysis Market Drivers, Challenges, and Risk Mitigation Strategies

Market drivers include escalating hydrogen demand in decarbonizing sectors and supportive policies. Hydrogen could meet 10% of global energy needs by 2050 in net-zero pathways, with pyrolysis benefiting from incentives like U.S. Inflation Reduction Act’s $3/kg clean hydrogen tax credit. Opportunities abound in carbon markets, where sequestered solid carbon could generate credits, enhancing project economics.

The dual-revenue model combining hydrogen sales with carbon co-product monetization creates a more compelling business case than single-product alternatives. Depending on the carbon allotrope produced (carbon black, graphite, or carbon nanotubes), potential revenue streams can significantly offset hydrogen production costs

Yet, challenges persist high capital costs for pilot-to-commercial transitions, energy sourcing for endothermic reactions, and carbon management to avoid environmental pitfalls like fugitive methane emissions. Life-cycle analyses indicate pyrolysis’s greenhouse gas footprint is minimal if powered renewably, but upstream methane leaks could undermine benefits.

Strategically, we recommend phased investments, i.e. pilot collaborations for technology validation, followed by joint ventures to de-risk scale-up. Policymakers should prioritize R&D grants and carbon pricing mechanisms to accelerate adoption.

Regional Analysis: Global Deployment Hotspots

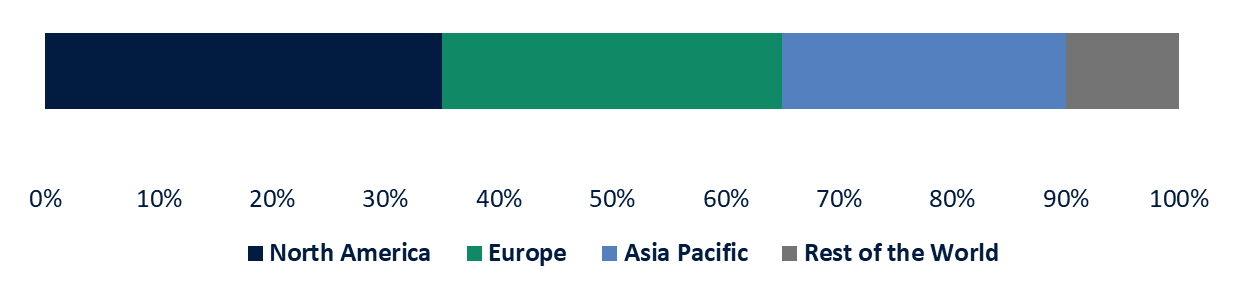

From a global vantage, United States leads with DOE-backed innovations, hosting 44% of pyrolysis developers and facilities like Monolith’s, supported by $1 billion in conditional loans. Europe follows, with BASF targeting large-scale pyrolysis by 2030 under the EU Hydrogen Strategy, which aims for 40 GW of electrolyzers but increasingly incorporates turquoise pathways for diversified supply.

In Asia, Australia and Japan drive progress; Hazer Group’s technology leverages abundant natural gas, while Asia-Pacific’s rapid industrialization could see pyrolysis capturing significant shares in ammonia and steel sectors.

Projected Regional Contributions to Low-Carbon Hydrogen Production by 2030

This distribution underscores the need for cross-border partnerships to standardize technologies and supply chains.

Strategic Recommendations and Future Outlook

For stakeholders navigating the evolving methane pyrolysis landscape, several strategic imperatives emerge:

1. For Technology Developers

-

-

- Focus on Carbon Product Marketability: Beyond hydrogen production efficiency, prioritize the quality and marketability of carbon co-products. The economic viability of methane pyrolysis hinges on creating high-value carbon allotropes with established market demand or developing innovative applications for lower-grade carbon materials.

- Pursue Strategic Partnerships: Form alliances with industrial offtakers for both hydrogen and carbon products. Technology developers should establish supply agreements with tire manufacturers (for carbon black), battery producers (for graphite), or advanced materials companies (for carbon nanotubes) to de-risk scale-up investments.

- Embrace Modular Deployment: Develop scalable, modular reactor designs that allow for incremental capacity expansion and testing in diverse operational environments. This approach reduces initial capital requirements and enables market-responsive growth based on proven performance.

-

2. For Investors and Policymakers

-

-

- Target Technology Scaling Gaps: Direct capital toward addressing critical scale-up challenges, particularly in catalyst longevity, reactor design, and carbon separation systems. Support should prioritize technologies that demonstrate clear paths to cost reduction through operational efficiency rather than merely theoretical advantages.

- Develop Carbon Market Infrastructure: Foster development of transparent markets and standards for carbon co-products, including quality specifications, valuation methodologies, and trading mechanisms to facilitate market liquidity for these materials.

- Balance Support Across Technology Pathways: Maintain a diversified portfolio of support across plasma, catalytic, and thermal pyrolysis approaches rather than concentrating on a single technology, as different methods may prove optimal for specific regional contexts and applications.

-

Conclusion

Looking ahead, methane pyrolysis could contribute to a $2.5 trillion global hydrogen economy by 2050, supporting 30 million jobs. Turquoise hydrogen pathways like pyrolysis may secure up to 25% market share in select regions by 2030. For clients, we advise scenario planning: assess feedstock availability, model cost curves under varying carbon prices, and pursue public-private pilots.

The coming decade will be decisive, with successful players being those who strategically navigate the complex landscape of technology options, market applications, and policy frameworks. For organizations prepared to make strategic investments and forge innovative partnerships, methane pyrolysis offers not merely compliance with decarbonization mandates but genuine competitive advantage in the emerging low-carbon economy.

Partner with us today to unlock methane pyrolysis opportunities and secure your leadership in sustainable hydrogen production.