Introduction: The Imperative for Regulatory Technology (RegTech) in Global Finance

RegTech refers to the application of technology particularly artificial intelligence, machine learning, cloud computing, and blockchain to enhance regulatory processes, compliance management, and risk monitoring within financial institutions.

Since the global financial crisis, regulatory obligations have grown substantially in both volume and complexity. For example, in a 2017 study, it was noted that regulatory fines and settlements had increased “a staggering 45-fold” and many banking CEOs (~ 85 %) indicated the escalating cost of compliance as a major disruption.

For financial institutions this means increasing volumes of reporting, expanded anti-money-laundering (AML) / know-your-customer (KYC) requirements, more stringent data-driven supervision and higher expectations around transparency and speed. On the supervisory side, authorities are under pressure to use technology-enabled approaches such as real-time data collection, analytics and risk monitoring.

Hence, the financial sector operates in a web of evolving regulations, from Basel IV capital requirements to the EU’s Digital Operational Resilience Act (DORA) and Asia-Pacific’s cross-border data flows under ASEAN frameworks. Moreover, As of 2024, global public debt stands at 93% of GDP, projected to hit 100% by decade’s end, amplifying fiscal scrutiny and compliance demands.

Consequently, adopting RegTech is no longer optional, it is a strategic imperative for institutions seeking to maintain competitiveness, manage regulatory cost and respond to rapidly evolving regulatory models.

The Core Driver: Quantifying the Regulatory Onslaught

The primary driver for RegTech adoption is the undeniable and quantifiable increase in regulatory pressure.

-

-

- Regulatory Volume: Globally, the number of regulatory updates consistently exceeds 200 revisions per day across more than 1,000 regulatory bodies. This volume makes manual tracking and implementation impossible.

- Enforcement Actions: Financial penalties are a tangible metric. Global banks have paid over $400 billion in fines since the 2008 crisis. In the year 2022 alone, global financial crime enforcement actions resulted in nearly USD 6 billion in fines, with Anti-Money Laundering (AML) failures being a primary contributor.

- Cost of Compliance: Compliance costs for banks can range from 2% to 10% of total operating costs, with smaller institutions disproportionately affected. This creates direct pressure on profitability.

-

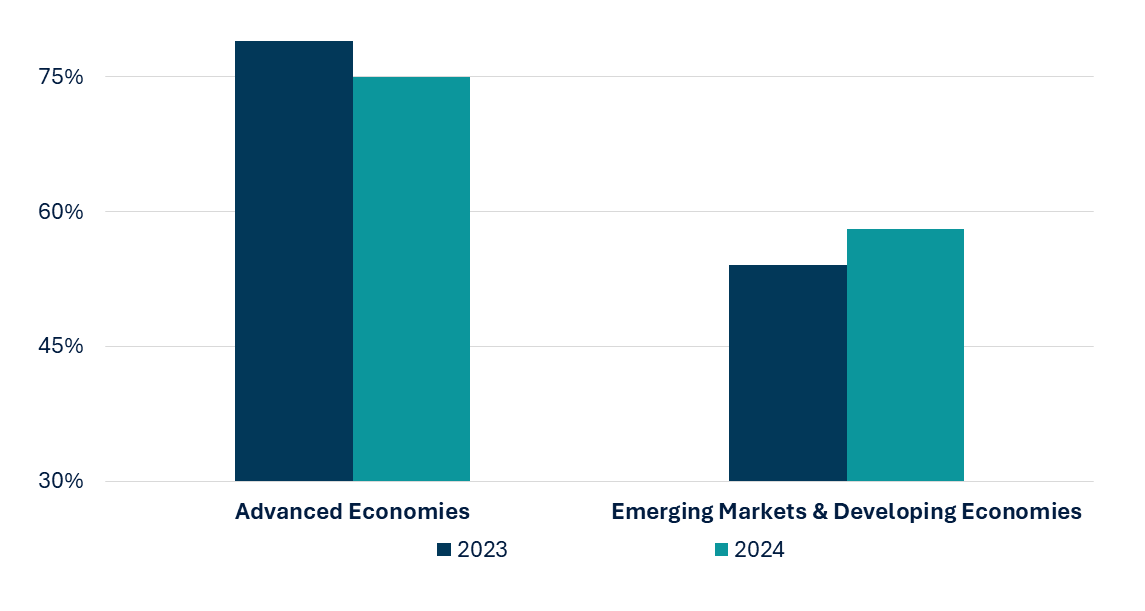

SupTech Adoption by Financial Supervisory Authorities

The RegTech Solution Set: A Focus on Core Applications

Strategic investment in RegTech is concentrating on several high-impact domains:

1. Anti-Money Laundering (AML) and Fraud Detection:

AI-powered transaction monitoring systems significantly reduce false positives which can constitute over 95% of alerts in legacy systems. Machine learning models can identify complex, and non-obvious patterns of illicit activity that rule-based systems miss.

2. Know Your Customer (KYC) and Onboarding

Digital identity verification and automated client lifecycle management can reduce onboarding time from weeks to hours, particularly through biometric-based eKYC systems that enable remote processes for unbanked populations, a critical enabler given that 850 million people globally lack official identification, including 35% of women in low-income countries. This enhances the client experience while simultaneously improving the accuracy and depth of due diligence.

3. Regulatory Change Management (RCM)

AI-driven platforms automatically monitor, interpret, and map regulatory updates from hundreds of global sources to an institution’s internal control framework, providing real-time impact analysis. Generative AI (GenAI) accelerates this by automating document summarization, information retrieval, and content generation, enabling faster deployment of compliance updates and reallocation of resources from manual tasks to strategic priorities, potentially boosting worker productivity, especially for lower-skilled roles, amid a projected USD 400 billion in AI investments for financial services by 2027.

4. Risk Management and Reporting

RegTech solutions automate the aggregation of data required for critical regulatory reports (e.g., Basel III, MiFID II, SFDR), reducing errors, operational risk, and the resource burden associated with manual reporting.

The Global Landscape and Strategic Considerations

Adoption and maturity vary significantly across regions, influenced by local regulatory stances:

Europe & UK

A leader in principle-based regulation, with regulators like the UK’s Financial Conduct Authority (FCA) operating a “Tech Sprint” and sandbox approach to foster innovation. GDPR and PSD2 have propelled RegTech maturation, particularly in data privacy and open banking, aligning with the European Commission’s 2018 FinTech Action Plan. AI integration, a RegTech cornerstone, shows 72% adoption among UK financial services firms as of 2022.

North America

Characterized by a more rules-based, enforcement-heavy environment. In U.S., agencies like the SEC and OCC are increasingly emphasizing the use of technology for effective compliance, viewing its absence as a potential indicator of weakness.

North American banks are prioritizing fraud detection and AML under Basel III. Strategically, firms here benefit from SupTech pilots, yet interoperability gaps with EU standards amplify cross-border costs by 15-20%

Asia-Pacific

A heterogeneous but rapidly growing market. Jurisdictions like Singapore and Hong Kong are proactively developing RegTech frameworks, while others are driven by the need to combat financial crime and manage massive, unbanked populations.

In Hong Kong, HKMA-driven strategies have achieved near-universal RegTech penetration, with 97% overall adoption across the banking sector in 2025, up from 83% in 2022, and 100% among retail banks, spanning AML, KYC, and reporting. For emerging markets within the Asia-Pacific region, RegTech plays a critical role in meeting FATF-aligned counter-terrorist financing (CFT) requirements. The region’s more than 6,000 FinTech firms serve as a powerful indicator of the scalable financial inclusion potential that RegTech solutions can unlock when deployed effectively.

RegTech Implementation Challenges

Common hurdles that undermine RegTech ROI:

-

-

- Legacy System Integration: The greatest technical challenge is integrating agile RegTech solutions with monolithic, decades-old core banking systems. To mitigate, executives should prioritize API-led modernization pilots, potentially reducing integration timelines by 40% while preserving data integrity.

- Data Fragmentation: RegTech’s efficacy hinges on high-quality, unified data streams, yet most financial entities grapple with siloed repositories and inconsistent formats that must be harmonized pre-implementation. Strategic remediation via enterprise data lakes and governance frameworks can enhance model reliability, unlocking 50% improvements in anomaly detection accuracy while bolstering ROI through reduced false positives.

- Talent Gap: A persistent scarcity of hybrid experts i.e. those blending profound regulatory acumen with advanced technical proficiency in AI and machine learning, constitutes a pivotal bottleneck, stifling effective RegTech orchestration.

- Vendor Proliferation: The market is fragmented, making it difficult to select viable, long-term partners versus point-solution providers. To counter, due diligence frameworks and multi-vendor strategies can mitigate lock-in, preserving ROI by averting 15-20% escalation in operational costs from single-point failures.

-

A Strategic Roadmap for RegTech Adoption

To successfully leverage RegTech, financial institutions must adopt a strategic, phased approach:

-

-

- Diagnose & Prioritize: Conduct a current-state assessment to identify the highest-cost, highest-risk compliance processes (e.g., AML false positives, manual reporting) that offer the greatest ROI for automation.

- Build the Data Foundation: Prioritize data governance and architecture. A unified data layer is a prerequisite for effective RegTech deployment.

- Foster a Collaborative Culture: Break down silos between Compliance, IT, and Business units. RegTech implementation is a cross-functional program, not an IT project.

- Engage Proactively with Regulators: Present a well-considered RegTech strategy to regulators, demonstrating a commitment to enhancing control effectiveness. Utilize regulatory sandboxes where available.

- Pilot and Scale: Begin with a controlled proof-of-concept for a specific use case. Demonstrate value, learn, and then scale across the organization.

-

Conclusion

RegTech represents a fundamental evolution in how financial institutions manage regulatory risk and opportunity. The regulatory burden is not abating, and traditional methods are unsustainable. The question for leadership is no longer if to invest, but how to build a coherent strategy that aligns technology, data, and talent to transform compliance into a source of resilience, insight, and competitive edge. The institutions that master this transition will be the ones to define the future of finance.