For most of the modern era, military advantage was bought in platforms: a more capable fighter, a quieter submarine, a longer-ranged missile. That logic is breaking down. In a contested fight against a peer adversary, the decisive variable is no longer any single platform but the speed and integrity of the network that connects them. The side that can sense, decide and act faster than its opponent wins, even with comparable hardware. This is the strategic premise behind Joint All-Domain Command and Control (JADC2), the United States’ effort to fuse data from sensors across every warfighting domain into a single, resilient decision network.

For defense companies, JADC2 is not a niche communications programme. It is a structural shift in where money, margin and power sit in the industry. It rewards software, data and integration over discrete hardware, and it is already redrawing the competitive map between century-old primes and a new class of software-first entrants.

The Concept: What JADC2 Actually Is and Why “Combined” Matters

JADC2 is best understood not as a product but as an outcome: connect any sensor to the best-placed shooter, regardless of which service owns either, and compress the decision cycle from days to minutes. The Pentagon frames it as the connective tissue of multi-domain operations, the layer that lets activity in one domain reinforce activity in another rather than merely deconflict with it.

The widely used label has since evolved to CJADC2 (Combined Joint All-Domain Command and Control) with the “Combined” signaling that allies and coalition partners are designed into the architecture from the outset, not bolted on afterwards. That distinction is strategically deliberate. A credible deterrent in the Indo-Pacific depends on operating seamlessly with partners such as Australia, Japan, United Kingdom and others, which is why the mission-partner environment sits at the core of the construct.

In February 2024 the Department of Defense (since restyled the Department of War) announced it had delivered a minimum viable capability for CJADC2 which is an initial, fielded version combining software applications, live data integration and cross-domain operational concepts, described by then-Deputy Secretary Kathleen Hicks as “real and ready now… low latency and extremely reliable.” Underneath that headline sit the individual service efforts that feed it: the Army’s Project Convergence, the Navy’s Project Overmatch, and the Department of the Air Force’s Advanced Battle Management System (ABMS), now folded into a broader portfolio the service calls the DAF Battle Network. A recurring 90-day experimentation series, the Global Information Dominance Experiments, is used to iterate and field capability quickly rather than waiting on a decade-long acquisition cycle.

JADC2 converts the unit of competition from the platform to the network. Advantage now accrues to whoever owns the integration layer, the data standards, and the software that turns sensor feeds into decisions.

Demand Signal: Budgets and the Pivot to Software

U.S. DOD’s FY2024 budget request earmarked roughly USD 1.4 billion specifically for CJADC2, and the funding lines beneath it tell a consistent story such as spending is rising, and it is tilting decisively toward software, data infrastructure and integration rather than new metal.

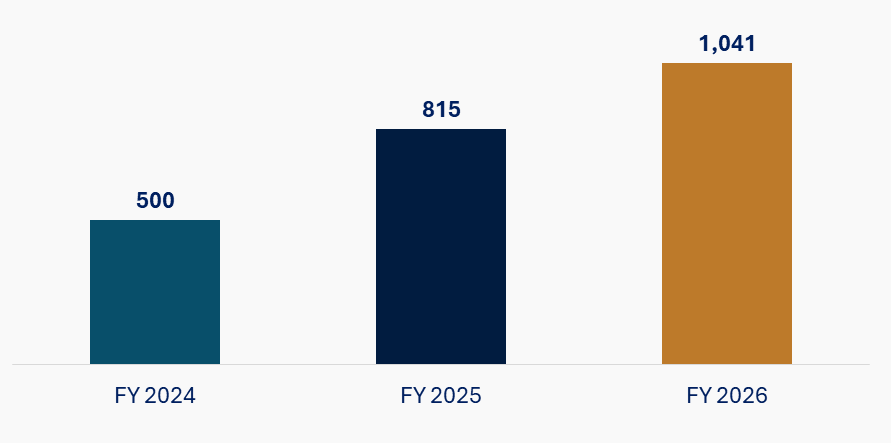

The clearest single barometer is ABMS, the Air Force’s contribution to JADC2. Its dedicated budget line has roughly doubled in two years, from about half a billion dollars requested in FY2024 to more than a billion in the FY2026 request and that figure captures only the slice owned directly by the integrating programme office, not the dozens of related programmes across the DAF Battle Network.

U.S. Air Force ABMS Funding (The Service’s Core JADC2 Line), USD Millions

Two further demand amplifiers matter for anyone modelling this market. First, the Pentagon has been deliberately re-engineering how it buys this capability. Through the Open Data and Applications Government-owned Interoperable Repositories (Open DAGIR) construct, launched in 2024, it is moving away from single-vendor “stovepipes” toward a government-owned, multi-vendor data architecture lowering the barrier for new entrants and reshaping incumbency. Second, the planned Golden Dome homeland missile-defense architecture which by design links sensors, command-and-control and interceptors into a single integrated network, and secured an initial tranche of roughly USD 25 billion is effectively a large, well-funded JADC2 use case. The command-and-control and sensor-fusion layer is where much of that value will be contested.

The Competitive Reordering: A Market in Motion: Disruptors, Primes and New Rules

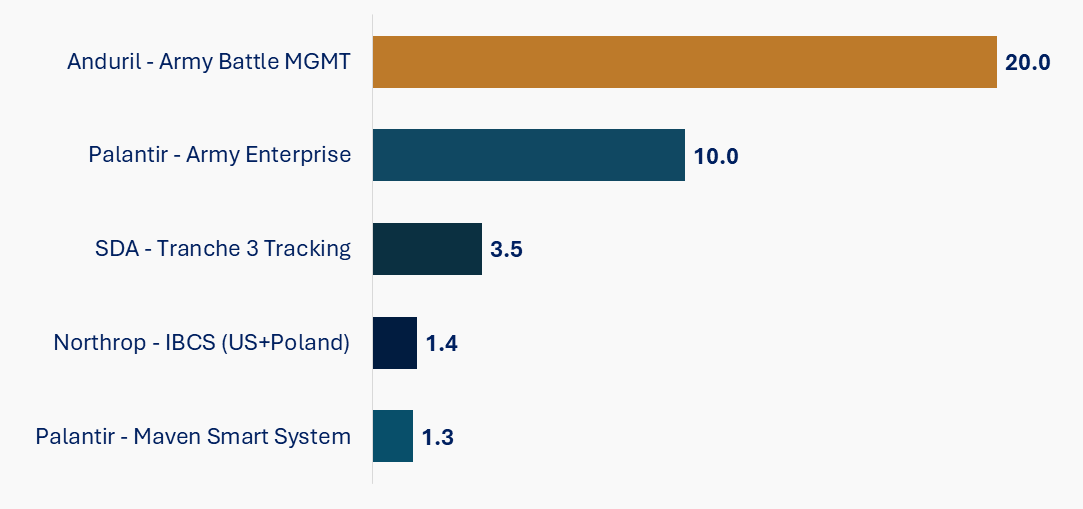

Nowhere is the JADC2 effect on industry structure clearer than in the contest now underway between software-first challengers and the established primes. On the challenger side, Palantir has built a commanding position through the Maven Smart System (MSS), the AI-enabled targeting and situational-awareness software that traces back to Project Maven. The trajectory is instructive: an initial five-year contract worth $480 million in May 2024 saw its ceiling raised to nearly $1.3 billion through 2029 just a year later, as the Pentagon moved to pre-position capacity for surging demand from combatant commands. By 2025 the system reportedly counted more than 20,000 users across dozens of tools, and the Department moved to transition it from prototype into a formal programme of record. In a separate and even larger signal, the Army awarded Palantir an enterprise software agreement in 2025 with a ceiling of up to $10 billion over a decade to consolidate data and software across the service. Palantir’s U.S. government revenue reached roughly $1.57 billion in 2024, up about 45% year on year.

Anduril has pursued a parallel path through Lattice, its AI command-and-control platform that fuses sensor data into a single operating picture and lets one operator orchestrate many autonomous assets. In early 2026 the Army selected Lattice as the backbone of a counter-drone interoperability effort under a ten-year indefinite-delivery vehicle with a ceiling reported at up to $20 billion explicitly to deliver common air-domain awareness across the force through a single proven C2 platform. Anduril’s rise has been underwritten by an extraordinary flow of private capital, which is itself a data point about how investors are repricing software-defined defense.

The established primes, far from being displaced, are defending and extending the high-assurance, hardware-integrated core of command and control. Northrop Grumman’s Integrated Battle Command System (IBCS), the Army’s programme of record for integrated air and missile defense, secured contracts totaling USD 1.4 billion in early 2025 spanning U.S. Army and Poland, and by mid-2025 the company had completed delivery of all major end items under low-rate production and moved to full-rate manufacturing. In space, the sensing backbone that JADC2 and Golden Dome depend upon is being built by a consortium of primes and new-space players: the Space Development Agency’s USD 3.5 billion award in December 2025 for 72 missile-tracking satellites split across Lockheed Martin, L3Harris, Northrop Grumman and Rocket Lab.

Deals, Alliances and Expansion: How the Field Is Consolidating

For corporate strategists, the most revealing signals are not the headline contracts but the maneuvering around them. Four categories of activity are reshaping the competitive landscape.

1. Mergers and Acquisitions

The software-first entrants are integrating vertically through acquisition to control the full stack beneath their C2 platforms. Anduril has acquired infrared-sensor maker American Infrared Solutions and Dublin-based ruggedized edge-computing firm Klas, folding both into the Lattice ecosystem, a deliberate move to own the sensing and tactical-edge processing that feed the network. In a striking sign of the shift in who leads major programmes, Anduril also assumed control of the Army’s multi-billion-dollar augmented-reality soldier programme previously run by Microsoft in early 2025.

2. Joint Ventures and Partnerships

Because no single firm owns the whole kill chain, alliances have become the defining structural feature of the market. In December 2024 Anduril and Palantir, nominal competitors, announced a consortium linking Lattice with the Maven Smart System and Palantir’s AI platform to move tactical sensor data into AI-assisted workflows. Both have separately partnered with frontier AI providers to embed large-language-model capability into defense software under appropriate accreditation. The Army’s TITAN ground-station targeting node, a Palantir-led award worth roughly $178 million, is delivered by a deliberately mixed industry team spanning Anduril, Northrop Grumman, L3Harris and others, a template for how disruptors and primes now combine rather than simply compete.

3. Market and Geographic Expansion

The “Combined” in CJADC2 is creating a substantial allied market. Northrop’s IBCS work now embeds Polish sensors and a UK missile system into a shared air-defense picture. Anduril’s Lattice-integrated programmes span Australia’s autonomous-undersea effort, a contract with the Dutch Ministry of Defense, and expanding positions across the Indo-Pacific and the Middle East. For suppliers, allied modernization accelerated by NATO members moving toward higher defense-spending targets is now as important a growth vector as the U.S. budget itself.

4. Technology Development

Underpinning all of the above is a sustained push to develop the enabling technologies: AI-driven sensor fusion, mesh networking, government-owned open data standards, zero-trust and data-centric security for coalition information sharing, and tactical-edge compute that functions in degraded, contested environments. The competitive question is shifting from “who has the best platform” to “whose software, data architecture and integration scale fastest and most securely.”

The Contracting Landscape: Selected JADC2-Enabling Awards and Contract Ceilings, 2024–2026 (USD Billion)

Value Migration: Five Shifts for Defense Leader

Taken together, the budget, contract and corporate signals point to five durable shifts in where value is created and captured across the defense industrial base.

From hardware margins to software economics

The fastest-growing pools sit in software, data and integration. These carry different cost structures, update cycles and margin profiles than platform manufacturing and reward firms that can iterate at the speed of code rather than the cadence of hardware.

Open architecture turns data into the strategic asset

The shift to government-owned, multi-vendor data standards erodes traditional incumbency. Lock-in moves from proprietary hardware to whoever sets and operates the data and interface layer. Owning the standard is now worth more than owning the box.

Programs of record convert pilots into recurring revenue

As capabilities like Maven transition from experiment to programme of record, the prize becomes durable, multi-year, license-and-sustainment revenue. The commercial winners are those who can cross the “valley” from demonstration to enduring acquisition.

Commercial capital is rewriting the supplier base

Venture-scale funding is creating credible new primes on a software-first model and compressing the build-to-field timeline. Incumbents must decide where to compete head-on, where to partner, and where to acquire capability they cannot build fast enough.

Allied demand is a growth engine, not an afterthought

The “Combined” mandate and rising allied budgets make coalition interoperability a primary commercial vector. Firms that design for partner integration and exportability from the outset will capture demand that single-market competitors cannot reach.