By-wire systems replace the mechanical and hydraulic linkages with sensors, redundant electronics and electric actuators and in the past eighteen months they have moved decisively from concept vehicles into series production programmes with named suppliers, certified safety cases and multi-million-unit contracts. Three developments define the inflection.

The strategic consequence is larger than a component substitution. By-wire is the physical enabling layer of the software-defined vehicle. It determines who writes the code that steers and stops the car, where chassis value migrates between OEMs and tier-one suppliers, and how quickly Chinese platforms convert engineering speed into global market position.

The End of the Mechanical Chassis: What By-Wire Actually Changes

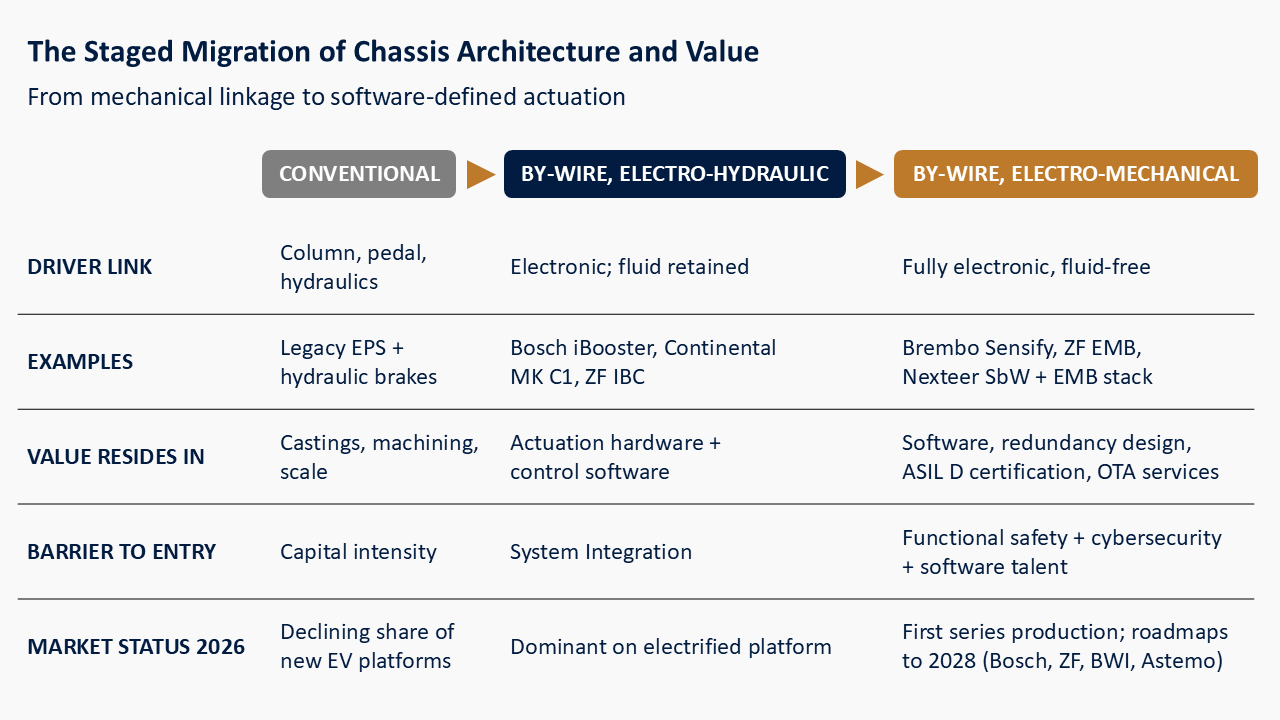

Steer-by-wire removes the steering column. The steering wheel becomes an input device with a force-feedback actuator; a separate road-wheel actuator turns the wheels based on electronic commands. Brake-by-wire follows the same logic in two stages: electro-hydraulic systems (EHB) sever the mechanical pedal link but retain fluid actuation, while electro-mechanical braking (EMB) eliminates hydraulics entirely, placing an electric motor at each caliper.

The commercial logic rests on five reinforcing drivers:

-

-

- Software-Defined Vehicle: SDV requires software-defined actuation where advanced driver assistance and automated driving functions need braking and steering that a computer can command with full authority, redundancy and millisecond latency.

- Packaging and Manufacturing: Deleting the column and hydraulic circuits frees cabin space, simplifies left-hand/right-hand-drive engineering and removes brake-fluid filling from the assembly line.

- Electric-Vehicle Synergy: By-wire braking blends friction and regenerative braking seamlessly, directly improving range.

- Variable Steering Ratio: Production systems from Tesla, Lexus and now Mercedes-Benz eliminate hand-over-hand steering at low speed while stabilizing response at highway speed.

- Lifecycle Economics: By-wire functions can be updated, tuned and monetized over the air across a vehicle’s life shifting chassis revenue from a one-time hardware sale toward recurring software value.

-

2025–2026: The Inflection from Prototype to Production

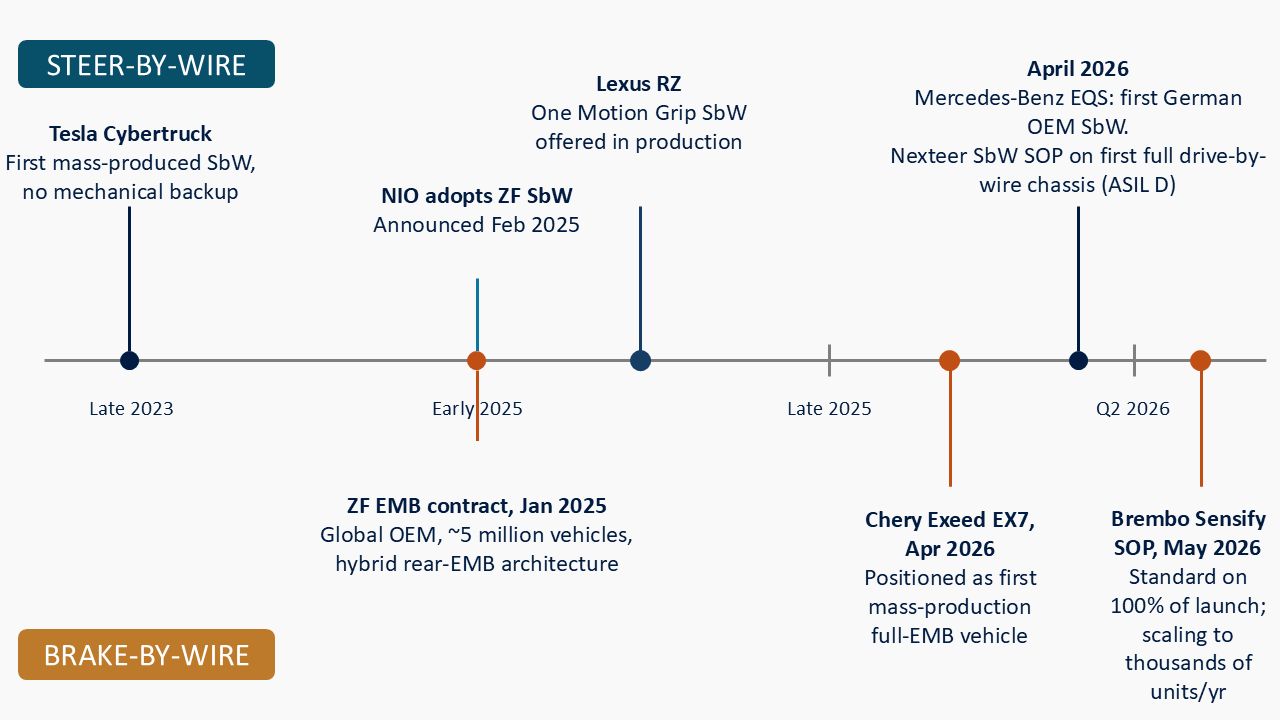

Tesla’s Cybertruck, launched in late 2023, was the first mass-produced vehicle to steer entirely by wire with no mechanical backup, and Lexus followed with its One Motion Grip system offered on the RZ. The past eighteen months converted isolated launches into an industrial wave and the geography of that wave is instructive.

In April 2026, Mercedes-Benz confirmed it will offer steer-by-wire on the updated EQS, becoming the first German manufacturer to bring the technology to production, paired with a flat-bottomed yoke enabled by the variable ratio. In the same month, Nexteer’s first series-production steer-by-wire system launched on a Chinese NEV platform, the vehicle Nexteer describes as the world’s first production passenger car with a full drive-by-wire chassis, built on multi-layered redundancy: dual controllers, dual power supplies, multiple communication links and dual actuation paths.

On the braking side, Chery has positioned its Exeed EX7, launched in April 2026, as the first mass-production vehicle with a fully electro-mechanical braking system, while Brembo’s Sensify entered series production weeks later. Suppliers including Bosch, ZF, BWI Group and Hitachi Astemo have publicly outlined competing dry brake-by-wire deployment roadmaps spanning 2025 to 2028.

Eighteen months separated the first multi-million-unit brake-by-wire contract from the first full drive-by-wire passenger car in series production. The cadence is accelerating, and its center of gravity is shifting toward China.

The Architecture Shift and Where the Value Migrates

The transition is not a single step but a staged migration, and each stage redistributes value. Electro-hydraulic by-wire systems (Bosch’s iBooster, Continental’s MK C1, ZF’s Integrated Brake Control) already dominate new electrified platforms. The frontier is the move to fully dry electro-mechanical systems, where the caliper itself becomes a mechatronic product combining an electric motor, a screw mechanism, force sensing and embedded software.

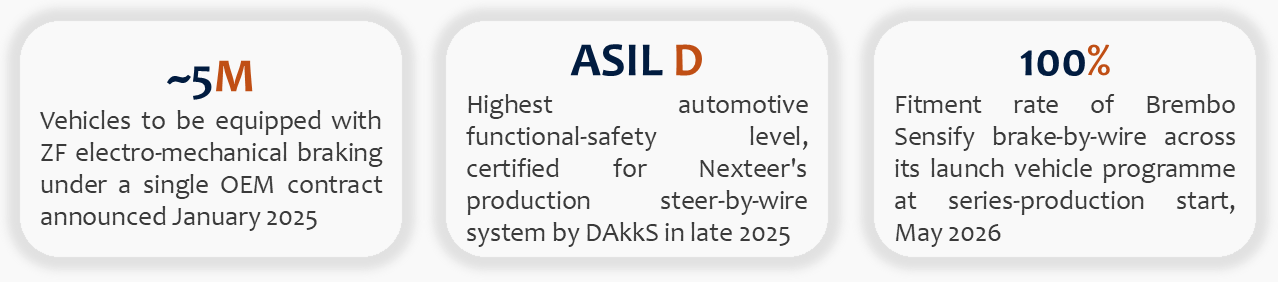

That redefinition changes who captures margin. A conventional brake corner is a commodity casting; an EMB corner is a safety-critical electronic control unit with an actuator attached. Functional-safety certification, redundant power & communication architectures, and cybersecurity compliance become the true barriers to entry as these capabilities are concentrated in a small set of tier-one suppliers and, increasingly, in vertically ambitious Chinese OEMs. ZF’s January 2025 contract illustrates the transitional economics where EMB and by-wire technology on the rear axle, combined with Integrated Brake Control and conventional hydraulic calipers at the front created a hybrid system that lets the OEM adopt the technology without betting the entire platform on it in one step.

China Sets the Pace, Europe Sets the Standard

Historically, safety-critical innovations debuted on German premium platforms and cascaded downward over a decade. By-wire is diffusing in the opposite direction i.e. the first full drive-by-wire production chassis is a Chinese new-energy vehicle; the first vehicle positioned as fully EMB-braked is a Chery; NIO committed publicly to ZF steer-by-wire in early 2025; and Brembo signed a co-development agreement for intelligent braking with JAC Group in February 2026.

Yet the certification backbone remains European. Nexteer’s production steer-by-wire achieved ASIL D approval through DAkkS, the German accreditation body, and UNECE steering regulations continue to define the type-approval pathway for most global markets. This creates a distinctive interdependence: Chinese platforms provide the volume, speed and consumer willingness to adopt; European suppliers and certification institutions provide the safety case that makes global export possible. Western OEMs that treat by-wire as a distant premium feature risk discovering as they did with battery cost curves that the learning curve has already been captured elsewhere. Mercedes-Benz’s decision to lead the German industry into production steer-by-wire on the EQS in 2026 should be read partly in this light as a defensive move to keep authorship of the driving experience in-house.

Deal Flow and Strategic Positioning: Contracts, Partnerships and Technology Bets

Because technology is consolidating around a small number of certifiable system suppliers, competitive positioning is being locked in through commercial instruments rather than open-market share battles. Four categories of activity stand out.

Platform-scale production contracts: ZF’s agreement to equip nearly five million vehicles with electro-mechanical braking, bundled with its Electric Recirculating Ball Steering Gear, is the template where multi-technology, and multi-year awards that make the supplier a chassis co-architect rather than a parts vendor. Brembo’s Sensify launch follows the same pattern, entering production fitted as standard across an entire programme, with additional customer contracts already signed.

Organizational consolidation as strategy: ZF merged its Active Safety Technology and Passenger Car Chassis Technology divisions in January 2024 to create a Chassis Solutions Division spanning steering, braking, dampers and software which is an explicit bet that OEMs will buy the by-wire chassis as an integrated system. Nexteer, historically a steering specialist, now markets a full “Motion-by-Wire” portfolio spanning steer-by-wire, rear-wheel steering and brake-by-wire, and used Auto China 2026 to declare its own EMB system market-ready, with more than twenty clients having completed driving evaluations.

Joint development and cross-border partnership: The Brembo–JAC agreement on intelligent braking, NIO’s adoption of ZF steer-by-wire, and the earlier Schaeffler–Paravan joint venture around the Space Drive drive-by-wire system all point to the same structural reality i.e. no single player holds the full stack of actuation hardware, redundancy engineering, vehicle-dynamics software and China market access. Expect partnership intensity and selective M&A around software, sensing and actuator specialists to increase as EMB roadmaps converge on 2027–2028 launch windows.

Market-entry expansion: Suppliers are using by-wire credentials to widen customer bases: Nexteer reports serving more than sixty automakers globally, including BYD, Xiaomi, Chery, Geely and Xpeng alongside BMW, Ford, GM, Stellantis, Toyota and Volkswagen, a customer map in which Chinese NEV makers are no longer a regional annex but a lead market for the most advanced systems.

Execution Risks

Redundancy Cost Versus Volume Economics: Eliminating the mechanical fallback means safety must be engineered in duplicate i.e. dual power supplies, dual controllers, and dual communication paths. Until volumes scale, by-wire systems carry a cost premium over mature hydraulic equivalents, which is why hybrid architectures such as ZF’s rear-EMB, front-hydraulic configuration will dominate the transition decade.

Regulatory Asymmetry: Type-approval frameworks are evolving at different speeds across UNECE markets, United States and China, and homologation strategy is now a genuine source of competitive advantage or delay. A system certified for one market cannot be assumed portable to another without material engineering and documentation effort.

Supply-Chain Concentration: EMB places a permanent-magnet electric motor at every wheel, deepening the industry’s exposure to rare-earth magnet supply chains at a moment when export controls have made that dependence a board-level geopolitical issue.

Consumer Trust and Liability: Early public reaction to yoke-style controls shows that human-machine-interface decisions can overshadow the underlying engineering. Product-liability frameworks for software-actuated braking and steering also remain untested at scale, a factor for OEM legal strategy and for insurers alike.

Implications for Stakeholders

For OEMs: Which layers of the by-wire stack are strategically essential to own (vehicle-dynamics software and tuning, most obviously) and which should be sourced from system suppliers? The answer determines platform architecture decisions being frozen in 2026–2027 for vehicles launching in 2029–2030.

For suppliers: The window to establish a certified, referenceable by-wire position is closing as platform awards concentrate. Component makers in the conventional brake and steering chain (castings, hoses, hydraulic components, columns) need explicit portfolio-transition plans, because the content they supply is being engineered out of the vehicle.

For investors and corporate development teams: The value migration mapped in above figure defines the M&A screen. Targets with functional-safety software capability, actuator mechatronics, force-sensing technology or China integration channels sit precisely where scarcity is forming. Conversely, portfolios concentrated in hydraulic-era content warrant a hard look at terminal-value assumptions.