From 2026, the EU Carbon Border Adjustment Mechanism (CBAM) mechanism entered its definitive phase where every ton of covered goods released into the EU now carries a financial liability, settled through CBAM certificates priced to the EU carbon market. The first certificates will be surrendered in September 2027, covering imports made throughout 2026.

CBAM is the operational edge of a deliberate repricing of carbon-intensive trade with the world’s largest single market, and its design contains a feature that most cost models miss. The charge is trivial in 2026 and structurally engineered to multiply year after year until 2034. Decisions taken against today’s near-zero number will look very different against the 2030 curve.

The Mechanics: How the EU CBAM Prices Carbon at the Border

CBAM currently covers six carbon-intensive sectors selected for their emissions intensity and their exposure to carbon leakage: iron and steel, aluminum, cement, fertilizers, electricity and hydrogen. For each shipment, an authorized importer must hold certificates equal to the embedded emissions of the goods, multiplied by the prevailing CBAM factor, and priced to the EU Emissions Trading System (EU ETS). The reference price for the first quarter of 2026 was set at €75.36 per ton of CO₂, calculated quarterly through 2026 and shifting to a weekly average from 2027.

The decisive design choice is the coupling between CBAM and the EU’s own industry. For years, European producers received free ETS allowances to shield them from carbon leakage. Those free allowances are now being withdrawn on a fixed schedule, and CBAM phases in at the same pace. CBAM factor is rising from just 2.5% of embedded emissions in 2026 to 100% by 2034. In other words, the border charge grows precisely as the domestic shield disappears, keeping imported and EU-made goods on the same footing.

A ton of carbon-heavy imported steel attracts only a few euros of CBAM cost in 2026 but by 2030 that same ton carries an order of magnitude more, and the full charge by 2034 is some forty times larger. The mechanism is back-loaded by design. Treating the 2026 number as representative and many procurement models quietly do build a cliff into the forecast.

The Exposure Map: CBAM Cost Exposure by Sector and Country

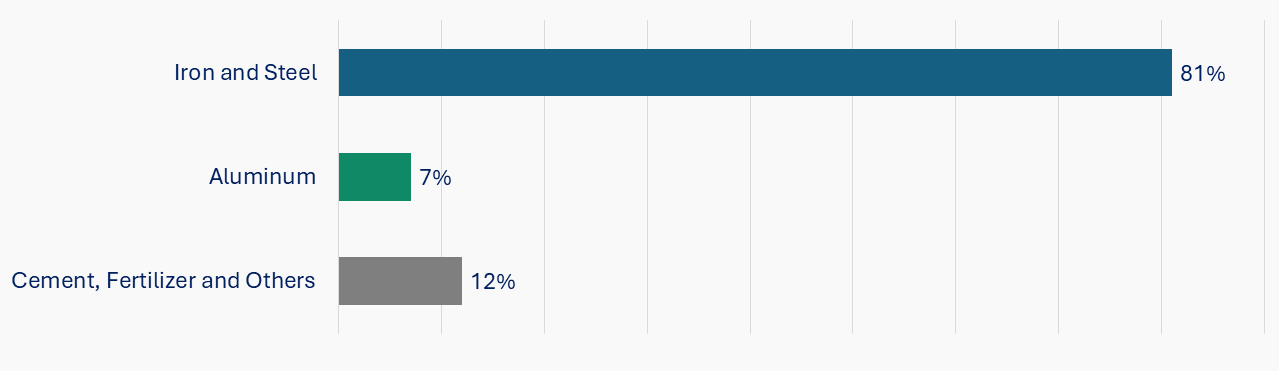

CBAM’s reach is broad, but its weight is not evenly spread. The metals complex dominates where iron and steel alone account for well over two-thirds of CBAM-exposed trade value and the large majority of projected certificate liabilities through 2035. Aluminum is a distant second; cement and fertilizers are smaller in absolute terms but acutely exposed relative to the value of what they ship. For most boards, managing CBAM is, first and overwhelmingly, a steel question.

Approximate Share of Projected CBAM Certificate Liabilities, 2026–2035

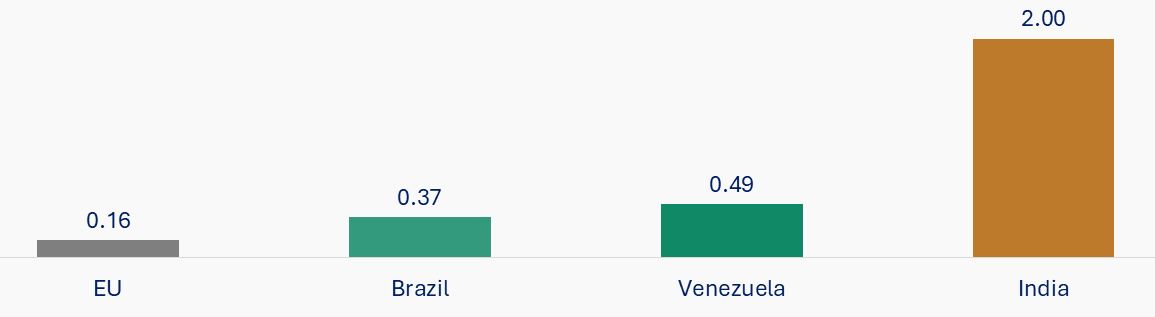

Geography concentrates the burden further. A handful of origins (China, Türkiye, India, Russia and Ukraine) are projected to generate most of the certificate demand. What sets the bill is the effective CBAM rate i.e. the cost as a share of the import’s value and that is driven by the carbon intensity of how a good is made, not how much of it crosses the border.

Two suppliers shipping the identical product can face wildly different border costs decided by the grid and the furnace behind them.

European steel is among the world’s least carbon-intensive per dollar of output whereas coal-reliant production elsewhere can embed many times more. Under the EU’s conservative default values, the implied effective CBAM rate reaches roughly 154% of import value for the most carbon-intensive Indonesian goods and around 86% for Egypt, while low-carbon origins such as Canada sit near the bottom. Carbon intensity has, in effect, become a procurement variable as concrete as unit price and lead time.

Carbon Intensity of Iron & Steel Exports (Kg CO₂ Per USD)

Inside the EU CBAM Simplification: Smaller Scope, Same Climate Ambition

In October 2025, the EU amended CBAM as part of its broader “Omnibus” simplification drive, and the change was widely read as a retreat. The headline measure replaced a fiddly per consignment value rule with a single de minimis threshold of 50 tons per importer per year. The threshold removes roughly 90% of importers covering SMEs and occasional shippers from the obligation entirely while still capturing about 99% of embedded emissions.

Electricity and hydrogen are excluded from the exemption and remain fully in scope at any volume. The threshold is reviewed every year to ensure the 99% coverage holds, and an importer who crosses it at any point becomes liable for the entire year’s imports retroactively, with punitive penalties for shipping without authorization. For the large, carbon-exposed corporates, the mechanism has been made leaner, more durable and considerably harder to circumvent.

The Strategic Response: Green Steel, Joint Ventures and the Industry’s CBAM Reckoning

Paired with the withdrawal of free ETS allowances, CBAM is forcing a capital-allocation reckoning across European heavy industry and the response so far is sharply bifurcated, separating the companies with an integrated energy-and-funding strategy from those waiting for the economics to arrive.

The green-steel playbook i.e. direct reduced iron paired with an electric arc furnace, ultimately run on green hydrogen is mature and deployable. The real constraints are the cost of green hydrogen at industrial scale and a green premium that buyers have proven unwilling to reliably pay.

Sweden’s Stegra (formerly H2 Green Steel) is the clearest test case. Its Boden plant pairs more than 700 MW of electrolyzers with DRI-EAF steelmaking, backed by some €6.5 billion raised but it required a financing lifeline through 2025 and early 2026, with the French hydrogen investor Hy24 and then a Wallenberg-led consortium stepping in to carry construction over the line. Capital, not engineering, is the gating factor.

Stegra’s €2.3 billion joint venture with Iberdrola to develop green-hydrogen and green-iron capacity in Iberia is the strategic template of the moment i.e. vertically integrating cheap renewable power with low-carbon production, so that the energy input is owned rather than bought at the mercy of the market. Such more partnerships, equity tie-ups and offtake structures are expected to built around the same logic to secure clean power and lock in green demand at the same time.

On the other side, ArcelorMittal paused its German DRI-EAF projects in Bremen and Eisenhüttenstadt in mid-2025, citing explicitly weaknesses in CBAM, Chinese overcapacity, and the absence of customers willing to pay for low-carbon steel. Salzgitter pushed back later phases of its SALCOS program. Meanwhile, state-backed Chinese capacity advanced on schedule. The lesson is that CBAM is necessary but not sufficient. It equalizes the cost of imports at the border, yet leaves EU producers exposed on export markets, which is why industry is pressing for export rebates and why Brussels has had to wrap CBAM inside a wider Steel and Metals Action Plan.

For exporters outside the EU, the strategic response is more straightforward and more urgent. The rational moves are twofold: invest in verified, audited emissions data to escape the deliberately punitive default values, and push to capture the carbon revenue at home rather than ceding it to the EU budget. The winners of this transition will be producers who can pair genuinely low-carbon output with secured, low-cost clean energy and committed buyers. The losers are stranded assets, squeezed between a rising carbon cost on one side and cheap high-carbon competition on the other.

CBAM Scope Expansion: Downstream Goods From 2028

In December 2025, the Commission proposed extending CBAM from 2028 to roughly 180 downstream steel- and aluminum-intensive products such as fabricated metals, machinery, vehicle components, industrial equipment and appliances, averaging around 79% metal content drawing an estimated 7,500 additional importers into scope. The proposal also makes pre-consumer scrap a CBAM precursor and tightens anti-circumvention rules, closing the obvious loophole of relocating the final manufacturing stage to dodge the charge on the metal inside.

The signal to any company that touches steel or aluminum even indirectly, as a manufacturer, OEM, builder or buyer of capital equipment is to assume in-scope status on a multi-year horizon rather than presume exemption. The default emissions values applied where verified data is absent are intentionally conservative and costly, precisely to push the market toward transparency. Emissions data is becoming a tradable asset, and the companies building that capability now will avoid paying the penalty for not having it later.

The Domino Effect: How the EU CBAM Is Spreading Carbon Pricing Worldwide

Perhaps CBAM’s most consequential effect is the one that happens beyond the EU’s borders. By attaching a price to the carbon in imports, it gives every trading partner a sharp incentive to price that carbon domestically and keep the revenue at home rather than handing it to Brussels. The result is a wave of policy momentum. United Kingdom launches its own CBAM on 1 January 2027; China is extending its emissions trading system to cover steel, aluminum and cement; and India, Türkiye, Brazil and Indonesia are each building or expanding carbon markets.

A linkage between the UK and EU emissions trading systems is under negotiation, which would remove the border charge between them altogether, a reminder that matching a carbon price can be worth more than absorbing one. For any board, the question is shifting from “are we exposed to the EU CBAM?” to “how do we position for a world of proliferating, interconnected carbon borders?” The patchwork is hardening into a system, and first movers on emissions transparency and low-carbon sourcing will carry a structural advantage into it.

Conclusion

The shape of CBAM is now clear. It is small today and large tomorrow by deliberate design. Its weight falls heavily on steel and on carbon-intensive origins, but unevenly enough that carbon intensity is now a competitive variable. The simplification made it more durable rather than less; the corporate response is already dividing the prepared from the exposed; and the perimeter is expanding both downstream into finished goods and outward across the globe.

CBAM is best treated not as a compliance line item but as a lens on the carbon-competitiveness of an entire supply chain and acted on while the cost is still low enough to make repositioning affordable. This is the kind of structural shift where early, well-modelled decisions compound, and where waiting for certainty is itself the most expensive option.