For most of the generative-AI era, banks have been buying assistants. Tools that summarize a document, draft a memo, or suggest a line of code which are useful but fundamentally passive. The frontier has shifted to agentic AI where systems that don’t merely answer, but plan, decide, call other systems, and execute multi-step work across the core of the bank with a human supervising rather than driving.

A copilot makes an existing employee marginally faster. An agent takes the workflow itself. Firms are being “fundamentally rewired” into a fully AI-connected enterprise where every employee is paired with an agent, every back-office process is automated, and every client journey is curated by AI. According to the bank’s own investor disclosures, more than 200,000 staff now use its internal LLM Suite, around 100 generative-AI solutions are in production, and the firm has begun deploying agents for genuinely multi-step tasks.

This separates the institutions that treat AI as IT procurement from those that treat it as strategy.

The Inflection Point: From Answering to Acting

The maturity curve is now well understood inside the sector starting from passive content generation (generative AI), then task-specific execution (single agents), and then to autonomous multi-agent orchestration (true agentic systems). Each step removes more human keystrokes from the loop and pushes the AI deeper into the bank’s systems of record i.e. loan book, payments rail, fraud engine, CRM.

What makes banking unusually fertile ground is structural. The sector carries decades of accumulated technical debt and large, expensive customer-facing workforces such as call centers, onboarding teams, and compliance analysts performing exactly the kind of repeatable, rules-bound, knowledge-heavy work that agents are built to absorb. The constraint has never been the opportunity. It has been trust, integration, and control. In 2025 and 2026, the vendors and the regulators began, simultaneously, to remove those constraints.

The Value is Already Banked: This is not the metaverse

The industry has been burned before by robotic process automation and the metaverse, and a steady drumbeat of commentary insists that AI investment has yet to pay for itself. The most useful corrective to that view is not a forecast but it is a disclosed profit and loss line.

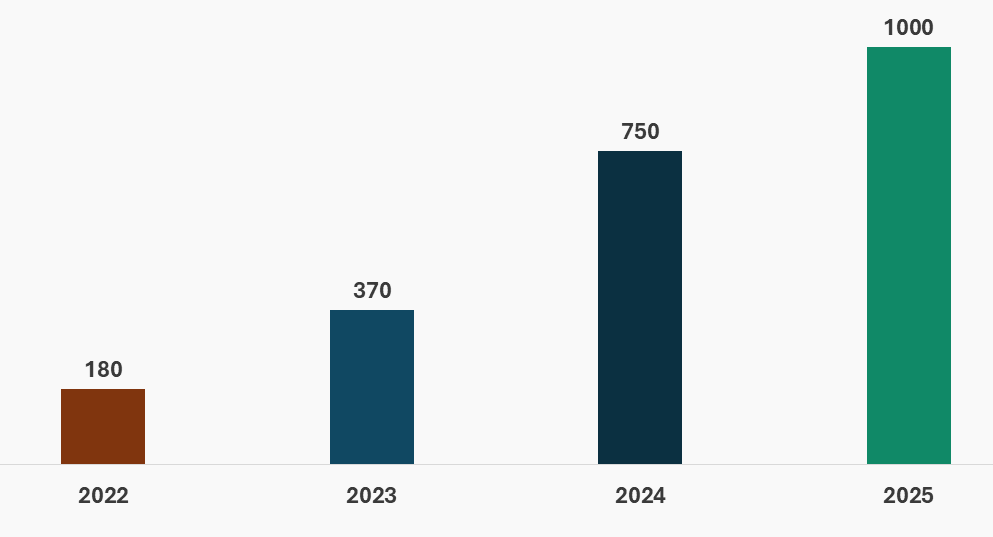

DBS, Southeast Asia’s largest bank by assets, reported that its data-analytics and AI initiatives generated approximately nearly USD 770 million in economic value in 2025, drawn from more than 430 use cases running on over 2,000 models. This result did not appear overnight. It is the top of a curve the bank has published for four consecutive years and the trajectory is the story.

DBS Group: Annual Economic Value from AI & ML (in S$)

The compounding is the point. Value roughly doubled each year from S$180m in 2022 to S$370m, then S$750m, then to the billion-dollar mark as the portfolio of use cases widened and the institution’s data foundations matured. Crucially, the bank frames this as redeployment of people toward higher-value relationship work, not headcount reduction, a narrative choice with real consequences for adoption.

The same signal appears across the largest balance sheets, in different currencies of measurement. Bank of America’s virtual assistant, Erica, has handled close to three billion interactions since 2018 and served roughly 20 million users in a single recent quarter. Its internal sibling, Erica for Employees, is used by more than 90% of staff and has cut calls to the service desk by around half. Citi’s generative coding assistant has completed hundreds of thousands of automated reviews, saving on the order of 100,000 engineering hours a week. They are production systems with measurable operating leverage.

The First Frontiers of AI Adoption in Banking

Agentic deployment in banking is not uniform. It concentrates first where the work is high-volume, evidence-based, and painfully manual and where a clean audit trail can be maintained. Four beachheads dominate.

-

- Financial-Crime Compliance: Anti-money-laundering investigation and KYC review are slow, costly, and plagued by false positives. In May 2026, FIS, a core processor that touches a meaningful share of the global economy, announced a partnership with Anthropic to build a Financial Crimes AI Agent that compresses AML investigations from days to minutes by assembling evidence across a bank’s core systems and surfacing the highest-risk cases for human review, with BMO and Amalgamated Bank among the first adopters.

- Lending and Credit Decisioning is the second front, where agents accelerate origination and underwriting.

- Customer Servicing is the third where DBS extended a generative-AI assistant to all corporate clients in late 2025.

- Software and Operations Engineering is the fourth, where coding agents are already at industrial scale.

The strategic implication is that early movers don’t just save cost on one process but they build a reusable capability that compounds across the next ten. The laggard, by contrast, rebuilds from zero each time.

The Strategic Paradox: Efficiency that can Erode the Franchise

AI that makes a bank radically more efficient can also make its customers radically more mobile and that cuts the other way on the income statement. Consider the deposit base. Enormous sums sit in low- or zero-interest checking accounts, profitable precisely because customers don’t move them.

Roughly USD 23 trillion of consumer deposits globally sit in near-zero-interest accounts. Now give every one of those customers an agent of their own. One that autonomously sweeps idle cash toward the best available rate, optimizes card balances, and exploits balance-transfer offers without being asked. The friction that protects net interest margins evaporates.

If banks do not adapt their business models, the most likely scenario shows global banking profit pools, on the order of USD 1.2 trillion, contracting by as much as USD 170 billion, or roughly 9%, as agentic intermediation redistributes deposits and compresses margins. The gains from efficiency, the firm warns, will largely be competed away over time, just as they were with digital banking.

Agentic AI is not a procurement decision to be delegated to the technology function. It is a question about the bank’s revenue model, its pricing, its distribution, and where it intends to sit when customers stop comparing products and start delegating decisions to machines. Treated as a cost program, agentic AI funds its own commoditization. Treated as a strategy, it is a chance to re-anchor the customer relationship before someone else’s agent does.

Capital In Motion: M&A, Joint Ventures and the Platform Land-Grab

The agentic-banking stack is being assembled through acquisition and partnership at speed, as incumbents race to own the orchestration layer rather than rent it. The pattern reveals a clear “build vs. buy vs. partner” choice that every institution now faces.

-

- M&A (UiPath acquires WorkFusion – 2026): The automation leader absorbed a specialist in AI agents for financial-crime compliance, a pre-built library automating AML and KYC, folding domain-specific banking agents directly into its platform. Consolidation is moving up the value chain, from generic automation to regulated, vertical-specific agents.

- M&A (ServiceNow acquires Moveworks): A multi-billion-dollar move to bring a front-end AI agent and enterprise search, already serving millions of employee users, into ServiceNow’s workflow orchestration engine, a system of action many banks already run.

- Platform (Fiserv launches agentOS; FIS partners with Anthropic): Two of the largest core processors are building governed, “agent-first” operating environments that sit natively across core, payments and servicing turning the rails thousands of mid-sized banks already depend on into agent-ready infrastructure.

- JV (UOB × Accenture): Singapore’s UOB chose the partner route to accelerate generative and agentic AI, a deliberate contrast to DBS’s in-house “build” philosophy, trading proprietary capability for speed to market.

- Talent (Citi’s leadership signal): Citi appointed a dedicated head of AI reporting into the COO function, a structural statement that agentic transformation is being run from the operating core, not the innovation lab.

The strategic read for any institution is that the platform layer is consolidating now. Banks that delay a clear sourcing decision risk being forced into whatever orchestration standard their core processor adopts on their behalf, a far weaker negotiating position than choosing deliberately today.

The Governance Imperative: Trust is the Gating Constraint

None of this scales without governance, and in financial services governance is not a brake but it is the license to operate. The autonomy and speed that make agents valuable are precisely what magnify their risk: an error, a bias, or a runaway action propagates at machine pace.

The regulatory perimeter is hardening accordingly. Under the EU AI Act, high-stakes banking use cases such as credit scoring fall into the high-risk category, carrying obligations around risk management, data governance and human oversight. The European Banking Authority’s late-2025 mapping confirmed broad compatibility with existing banking law while flagging that obligations like human oversight and cybersecurity are not waived by prudential compliance. The Digital Operational Resilience Act (DORA) places ultimate accountability for ICT systems with management. In the UK, the Financial Conduct Authority has opened an AI sandbox and live-testing route, with senior-manager accountability and consumer-duty rules applied directly to agentic deployments.

This reframes governance from cost to moat. The banks moving fastest i.e. DBS built in close partnership with its regulator; FIS and Fiserv are embedding traceability and human oversight into their platforms by design are treating control architecture as the enabler of speed, not its enemy.