Executive summary

Unmanned aerial systems (UAS) have permeated global operations, from precision logistics in Brazil’s vast ports to surveillance in Africa’s conflict zones, yet their dual-use nature amplifies vulnerabilities across sectors. Rapid global proliferation of commercially available UAS, their operational use in multiple conflict zones and escalating disruptive incidents near civilian infrastructure are accelerating demand for counter-UAS (C-UAS) capabilities.

Public authorities across regions are converging on a “layered assurance” model (i.e. detection, identification, attribution, and graduated mitigation) which creates clear opportunities for systems integrators, managed-service providers and compliance-focused vendors.

Europe’s €1.065 billion European Defense Fund infusion for 2025 underscores radar and sensor advancements against drone incursions, while Asia-Pacific’s innovations, including India’s laser-based neutralizers, signal a 20-25% annual investment cadence through 2030. Executives navigating this terrain must recalibrate risk paradigms, prioritizing interoperable detection-mitigation hybrids that transcend borders. By 2030, as global UAS registrations surpass 10 million, entities embedding these capabilities will command resilient ecosystems amid inexorable aerial contestation.

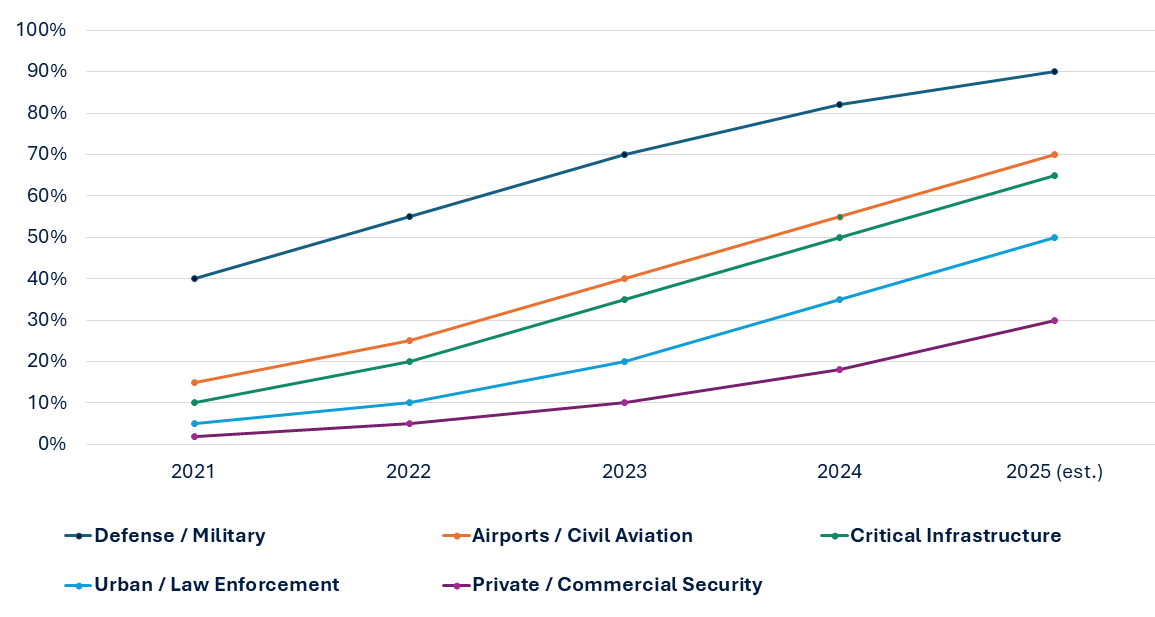

Global Anti-Drone Market Adoption Curve by Sector (2021–2025)

The Global Threat Landscape: A Borderless Challenge

The drone threat is a global phenomenon, manifesting uniquely across different geopolitical contexts. The 2018 disruption at London’s Gatwick Airport, which grounded hundreds of aircraft, was a watershed moment for European aviation security. In the Middle East, non-state actors have systematically weaponized commercial drones, a tactic starkly evidenced by the 2019 attacks on Saudi Aramco facilities, which temporarily halved the kingdom’s oil production. Meanwhile, in conflict zones like Ukraine, the proliferation of first-person view (FPV) drones has created a continuous, tactical-level threat, demanding agile and decentralized C-UAS solutions from frontline units.

The data confirms a universal surge in incidents. From a civilian perspective, air safety authorities globally are reporting a sharp increase in sightings. For instance, Australian agencies have reported a 400% increase in drone sightings near manned aircraft in controlled airspace between 2020 and 2023, a trend mirrored in Europe and Asia. This is not a regional issue; it is a systemic vulnerability in the global commons.

Deconstructing the Global C-UAS Ecosystem: A Technology and Application Analysis

Sophisticated C-UAS architecture is not a single product but an integrated system of systems, with technology preferences often dictated by regional regulations, operational environments, and budgetary constraints.

Pillar 1: Detection, Identification, and Tracking (DIT)

This foundational layer is seeing rapid innovation driven by global demand. The strategic trend is sensor fusion, combining:

-

-

- Radio Frequency (RF) Analyzers: Effective in populated areas but challenged by pre-programmed, autonomous drones.

- Radar: Critical for long-range perimeter defense of critical infrastructure like airports and energy facilities.

- Electro-Optical/Infrared (EO/IR): Essential for visual confirmation and forensic analysis, widely used in border surveillance.

- Acoustic Sensors: Gaining traction for low-cost, passive detection in urban canyons and for protecting forward military bases.

-

The integration of these data streams into a single Common Operational Picture (COP) using Artificial Intelligence (AI) is now a global standard for credible C-UAS command and control.

Your Action: Develop and aggressively market your C2 system’s API-driven interoperability. Your platform’s ability to integrate third-party sensors is a powerful competitive wedge against closed, proprietary systems.

Pillar 2: Mitigation and Neutralization

Mitigation strategies reveal significant global variation, reflecting differing legal and operational doctrines.

-

-

- Kinetic/Physical: Often employed in active conflict zones or for endpoint defense on military vessels. The risk of collateral damage from falling debris makes them less suitable for dense urban environments in peacetime.

- Electronic/Non-Kinetic: The dominant growth segment globally. Techniques include:

-

- Jamming: Widely deployed but strictly regulated. European nations, for example, operate under stringent European Conference of Postal and Telecommunications Administrations (CEPT) regulations governing signal interference, which shapes procurement decisions.

- Spoofing: A more sophisticated technique for covertly taking control of a drone, of high interest to intelligence and special forces units.

- Directed Energy (DE): High-Power Microwave (HPM) and Laser systems represent the strategic high ground. While U.S., and China are leading development, several NATO allies and Gulf states are actively testing and procuring these systems for fixed-site defense.

-

-

Your Action: Position your electronic warfare suite as the “lawful and precise” alternative to kinetic options. For DE, pursue strategic partnerships with leading R&D firms to fast-track a market-ready product, targeting the lucrative fixed-site defense segment (airports, nuclear facilities, military HQs).

Global Market Dynamics: A Multi-Polar Investment Landscape

The global C-UAS market is being propelled by diverse, concurrent drivers across all continents. Reliable data from international sources confirms this decentralized growth.

-

-

- NATO has established a Counter-UAS Reference Architecture, creating a multi-billion-euro, standardized market for interoperable technologies among its 32 member states.

- The European Defense Fund has allocated significant funding to C-UAS projects under its “Air Defense” priorities, fostering a collaborative European industrial base.

- In the Middle East, the Gulf Cooperation Council (GCC) states are among the world’s most active procurers, driven by the direct threat to their energy and infrastructure assets.

- Asia-Pacific nations, including Japan, South Korea, and Australia, are rapidly expanding their C-UAS capabilities in response to regional security dynamics and the protection of critical national infrastructure.

-

The following table, based on an analysis of global defense white papers and public tender data, illustrates the primary application segments from a worldwide perspective.

|

Application Segment |

Global Hotspots | Dominant Technology Focus |

Strategic Consideration |

|

Military & Defense |

Eastern Europe, Middle East, South Asia |

Electronic Attack, Directed Energy, Drone-on-Drone |

Electronic warfare resilience, interoperability with allies, mobility. |

|

Critical Infrastructure |

GCC, Europe, Asia-Pacific |

RF Sensors, Jamming, Geofencing |

Balancing efficacy with continuity of essential services (e.g., no GPS denial). |

|

Airport & Aviation Security |

Global (All Major Hubs) |

Long-Range Radar, Integrated C2 |

Integration with Civil Aviation Authorities, minimal passenger disruption. |

|

Border & Maritime Security |

Southern Europe, Southeast Asia, Americas |

Coastal Radar, EO/IR, Portable Jammers |

Coverage of vast, remote areas, distinction between drones and wildlife. |

Strategic Recommendations for a Global Framework

For sovereign nations and multinational corporations, a siloed or nationally biased approach to C-UAS is insufficient. We advise a globally informed strategic posture:

-

-

- Conduct a Geographically Tailored Risk Assessment: The threat profile in the Middle East (weaponized drones) differs from Europe (smuggling, espionage) or Southeast Asia (border incursions). Defense postures must be calibrated to the specific, local threat.

- Build a Layered, Technologically Agnostic Architecture: No single technology is a panacea. A resilient defense integrates diverse detection and mitigation layers to create overlapping fields of protection.

- Navigate the International Regulatory Maze: Proactively engage with national telecommunications, aviation, and spectrum management authorities. A legal system in one jurisdiction may be prohibited in another, complicating deployment for multinationals.

- Forge Alliances and Promote Interoperability: For nations, this means adhering to common standards like NATO’s. For enterprises, it means selecting systems that can share threat data with local law enforcement and national authorities.

-

Conclusion: The Future is Networked and Collaborative

The global C-UAS market is evolving from a collection of national programs into an interconnected, intelligent ecosystem. The future will be defined by international data-sharing agreements, AI-driven threat classification, and collaborative engagement protocols. The strategic differentiation will lie not merely in procuring advanced hardware, but in building the command-and-control networks and international partnerships that allow for a unified defense. For global entities, interoperable C-UAS capability is no longer a tactical upgrade – it is a fundamental pillar of national and economic resilience in the 21st century.

Deploy a definitive counter-drone strategy – connect with our experts for a tailored capability demonstration.