Executive Summary

As global leaders grapple with escalating climate targets and supply chain volatilities, the rolling stock market, encompassing locomotives, passenger coaches, and freight wagons, emerge as a cornerstone for resilient, low-carbon mobility. Rail currently handles 8% of global passenger-kilometers and 7% of freight ton-kilometers while consuming just 2% of transport energy, underscoring its efficiency edge. Yet, with passenger volumes rebounding 7% year-over-year in 2024 across UIC members and freight shares holding at 43% of inland transport, strategic investments in electrified fleets could unlock $550 billion in EU high-speed rail benefits alone by 2050.

The Macroeconomic Landscape: A Market in Motion

The rolling stock sector is not immune to the broader currents of global economics and geopolitics. Contrary to narratives of stagnation, the market is demonstrating robust growth, fundamentally underpinned by state-level fiscal policies and international climate commitments.

The global rail fleet is expanding. The worldwide railway network spans over 1.3 million route-kilometers, with Asia accounting for a dominant and growing share. This physical expansion necessitates a parallel expansion of rolling stock assets. Rail infrastructure is a key component of national stimulus packages, particularly in the wake of global economic shocks, positioning it as a non-cyclical investment in long-term economic resilience.

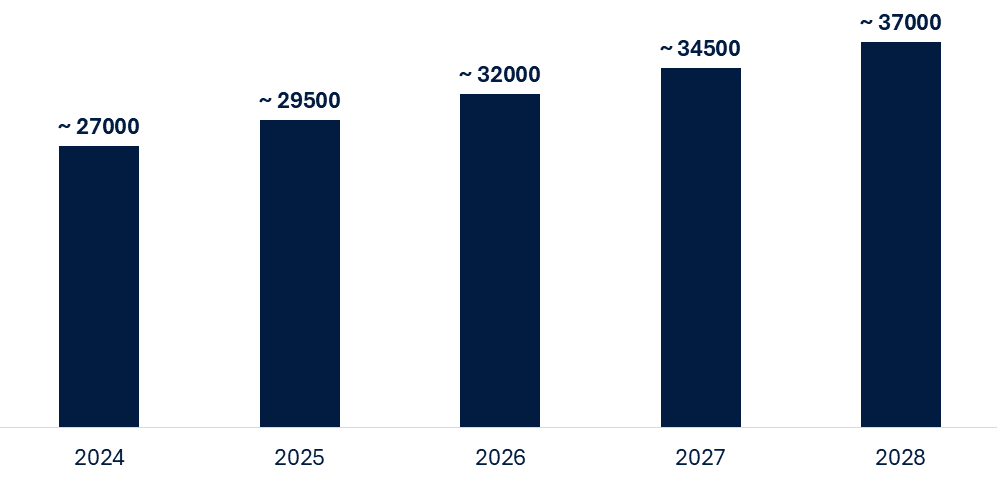

Projected Annual Demand for New Rolling Stock Units (Global)

Primary Demand Drivers: Beyond Simple Replacement

The demand for new rolling stock is multifaceted. Our analysis identifies three primary, interconnected drivers:

Urbanization and Mass Transit Expansion

The United Nations Department of Economic and Social Affairs (UN DESA) projects that 68% of the world’s population will reside in urban areas by 2050. This relentless urban concentration is creating immense pressure on public transit systems. Cities from Cairo to Jakarta are investing billions in new metro and light rail lines, creating a sustained, high-volume demand for EMUs (Electric Multiple Units) and trams. This segment represents the most consistent and predictable pipeline for rolling stock manufacturers.

The Decarbonization Imperative

The global shift towards a low-carbon economy is the most powerful structural driver. Rail transport is inherently more energy-efficient than road or air freight. Rail accounts for less than 1% of the EU’s transport-related greenhouse gas emissions while handling over 12% of freight and 8% of passenger traffic. Consequently, national governments are using rail as a lever to meet their Paris Agreement commitments. This is manifesting in two ways: the electrification of existing diesel lines and the strategic modal shift of freight from road to rail.

Geopolitical Re-shoring and Supply Chain Resilience:

Recent global disruptions have underscored the vulnerability of elongated supply chains. In response, nations are prioritizing domestic and regional manufacturing and logistics. Rail freight, with its ability to move large volumes efficiently over land, is a direct beneficiary. This is particularly evident in corridors like the EU’s Trans-European Transport Network and China’s Belt and Road Initiative, where investments in heavy-haul freight locomotives and intermodal wagons are accelerating.

The Strategic Shift: From Asset Procurement to Lifecycle Management

Leading players are no longer merely purchasing trains; they are investing in integrated mobility solutions. The focus is shifting from the Capital Expenditure of acquisition to the Total Cost of Ownership over the asset’s lifecycle. This paradigm shift is creating new value pools and competitive differentiators.

The Evolving Value Proposition in Rolling Stock

|

Traditional Model (Cost-Centric) |

Future Model (Value-Centric) |

| Focus on upfront purchase price |

Focus on lifecycle cost (maintenance, energy, availability) |

|

Reactive, scheduled maintenance |

Predictive maintenance powered by IoT and data analytics |

| Isolated asset procurement |

Integrated service contracts (e.g., Maintenance-as-a-Service) |

|

Standardized, one-size-fits-all fleets |

Modular, customizable platforms for regional needs |

| Mechanical reliability as key KPI |

Digital services (passenger Wi-Fi, real-time data) as key KPI |

This transition necessitates a deeper collaboration between operators and manufacturers and demands new capabilities in data analytics and service engineering.

Technological Disruption: The Digital and Green Rail Nexus

The rolling stock of the future will be defined by its software and energy source as much as its hardware.

-

-

- Digitalization and IoT: Sensors embedded in wheels, brakes, and engines generate terabytes of data. This enables predictive maintenance, moving from fixed schedules to condition-based interventions. This reduces downtime, extends asset life, and improves operational safety. For instance, the German national railway company, Deutsche Bahn, has publicly reported a target of reducing train failures by 25% through its predictive maintenance initiatives.

- Alternative Traction Systems: While electrification is the priority, the high cost of installing catenary wires on non-core routes is a barrier. This has catalyzed innovation in battery-electric and hydrogen fuel cell trains. Countries like Germany and the UK have already deployed hydrogen trains in regional service, with the technology offering a zero-emission solution for non-electrified lines.

- Automation and ATO: Automated Train Operation (ATO) over existing lines (GoA 2/3) is becoming standard in new metro systems and is being piloted for mainline services. The primary benefits are not driverless operation but enhanced capacity, punctuality, and energy efficiency through optimized driving profiles.

-

Strategic Recommendations for Stakeholders

In this complex environment, a passive approach is a recipe for obsolescence. We advise our clients to consider the following imperatives:

For Operators and Transport Authorities:

-

-

- Future-Proof Procurement: Embed digital and sustainability requirements into tender documents. Prioritize vendors offering open-data architectures and energy-efficient technologies.

- Forge Strategic Partnerships: Move from transactional buyer-supplier relationships to long-term partnerships for fleet availability and modernization.

- Develop Data Competency: Invest in the internal capability to manage, analyze, and leverage asset data for operational and commercial advantage.

-

For Manufacturers and Investors:

-

-

- Pivot to Service-Based Models: Develop competitive, high-margin service offerings around maintenance, modernization, and digital upgrades.

- Invest in R&D for Modularity: Create flexible rolling stock platforms that can be easily adapted for different regional requirements and future technological upgrades.

- Conduct Granular Market Analysis: Focus on specific, high-growth corridors and urban clusters rather than treating regions as monolithic markets.

-

Conclusion

The global rolling stock market is at an inflection point. Success will be determined not by the volume of units produced, but by the strategic foresight to align with macro trends in sustainability, digitalization, and shifting economic geography. The winners in this new era will be those who view rolling stock not as a static asset, but as a dynamic, data-generating node within an intelligent, integrated, and green transportation ecosystem. The time for strategic repositioning is now.

Accelerate your strategic positioning in the evolving rolling stock market—let’s build your actionable roadmap.