In an era of accelerating digital commerce and shifting consumer financial behaviors, Buy Now, Pay Later (BNPL) has emerged as a pivotal financing mechanism. BNPL allows consumers to acquire goods or services immediately while deferring payments into interest-free installments, typically over four to six weeks. This model, often facilitated through partnerships between fintech platforms and merchants, addresses liquidity constraints without traditional credit’s immediate burden.

As businesses navigate global economic volatility, understanding BNPL’s dynamics is essential for optimizing revenue streams, managing risks, and aligning with regulatory evolutions.

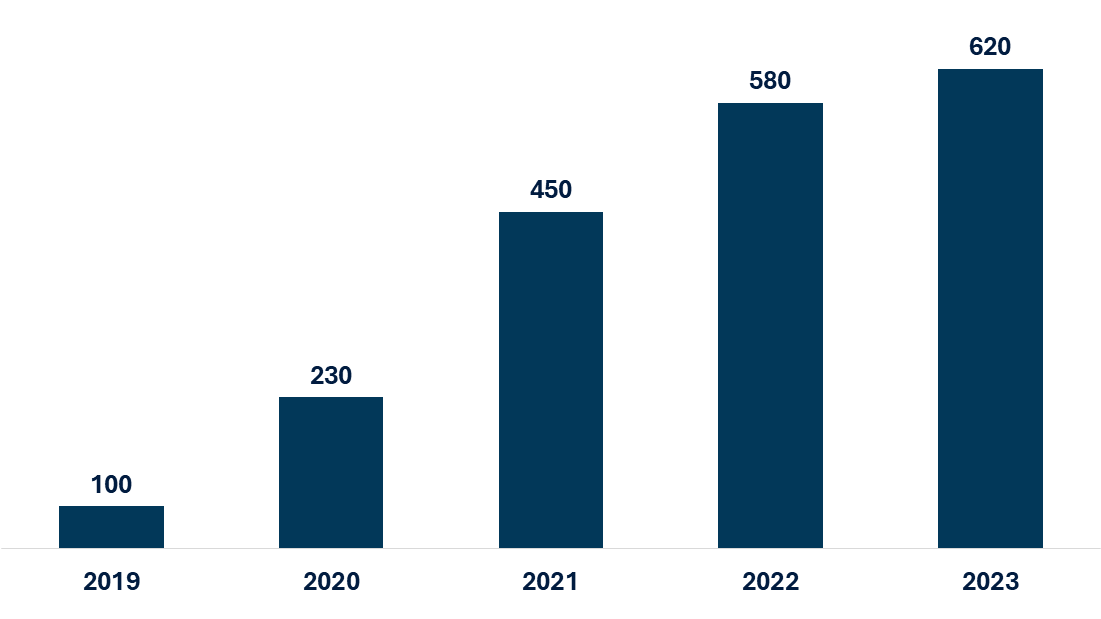

Global BNPL GMV Growth Index (2019 = 100)

Global BNPL Market Overview and Growth Trajectory

BNPL’s expansion reflects broader trends in digital payments and e-commerce penetration. Globally, the gross merchandise value (GMV) processed through BNPL platforms surged more than sixfold between 2019 and 2023, driven by platforms like Affirm, Klarna, and Afterpay. This growth accelerated during the COVID-19 pandemic, with app downloads and daily active users spiking as consumers shifted to online shopping.

In United States, BNPL loan originations by major providers leaped 970% from 16.8 million in 2019 to 180 million in 2021, with GMV rising from $2 billion to $24.2 billion. Daily applications in U.S. escalated from over 100,000 in 2019 to more than 1 million in 2022, underscoring robust demand.

Regionally, adoption varies but shows consistent upward momentum. In Australia, BNPL accounted for 0.7% of consumer payments by number in 2022, up from 0.5% in 2019. Europe exhibits strong uptake in countries like Sweden and Germany, where e-commerce efficiency and regulatory leniency facilitate integration.

Emerging markets in Asia, such as China and Singapore, also report significant growth, though data granularity is limited. BNPL thrives in environments with high inflation, inefficient banking systems, and elevated household debt levels, correlating positively with e-commerce maturity.

Consumer Adoption and Behavioral Shifts

1. Demographic Drivers

BNPL adoption displays distinct demographic patterns, with younger generations leading utilization rates. Recent data indicate that 41% of consumers aged 16-24 and 39% of those aged 25-34 have used BNPL services, compared to just 11% of those aged 65 or older. Millennials show the highest adoption rates, with 48% having used BNPL at least once, compared to 40% of Gen Z, 28% of Gen X, and 13% of Baby Boomers.

Contrary to expectations, BNPL usage is most prevalent among higher-income households. Data reveals that over 35% of households earning between $100,000 and $150,000 annually are active BNPL users, compared to 27% of those earning between $25,000 and $50,000. This pattern suggests that BNPL is being used as a cash flow management tool across income segments rather than solely as a credit access mechanism for lower-income consumers. Also, the adoption of BNPL is found higher particularly in regions with high household debt-to-GDP ratios.

2. Purchasing Behavior and Basket Economics

BNPL has expanded beyond its initial focus on big-ticket items to encompass everyday purchasing categories. The three most common categories for BNPL purchases now include clothing and footwear, electronics, and groceries. This diversification signals BNPL’s evolution from a specialized financing option to a general payment method integrated into routine consumer spending.

The behavioral economics of BNPL demonstrate clear benefits for merchants. BNPL can increase average order values by 20% to 40% and significantly boost conversion rates. Furthermore, omnichannel BNPL users spend on average 70% more per transaction than other online shoppers, highlighting the model’s strong impact on basket size. Approximately 40% of BNPL sales come from new customers to the retailer, indicating its effectiveness in customer acquisition.

For consumers, BNPL offers interest-free flexibility, enabling purchases without immediate full payment. Merchants benefit from increased conversion rates, higher average order values, and risk transfer to platforms, which handle credit and fraud. Businesses integrating BNPL report sales uplifts, as it broadens access to credit-constrained segments.

Future Outlook and Strategic Recommendations

1. Sector Expansion and Ecosystem Development

The BNPL ecosystem continues to evolve beyond traditional retail, expanding into new industry verticals and payment contexts. Significant growth opportunities exist in:

-

-

- B2B BNPL: B2B BNPL solutions typically feature larger transaction values, often ranging from USD 10,000 to USD 500,000, compared to an average B2C BNPL loan of about USD 135.

- Healthcare, Education, and Professional Services: BNPL is increasingly being deployed for medical treatments, educational courses, and home improvement services, expanding its reach into traditionally credit-resistant sectors.

- Embedded Finance Integration: BNPL is becoming increasingly embedded within broader financial ecosystems, integrated with digital wallets, neobanks, and e-commerce platforms to create seamless user experiences.

-

2. Strategic Recommendations for Stakeholders

-

-

- For Financial Institutions:

-

Develop hybrid BNPL offerings that combine the convenience of fintech solutions with the robust risk management capabilities of traditional lenders. Explore partnerships with established BNPL platforms to accelerate market entry while mitigating development risks.

-

-

- For Merchants:

-

Implement carefully calibrated BNPL strategies that balance the conversion and average order value benefits against the higher transaction costs. Consider segment-specific approaches, focusing on product categories and customer segments where BNPL provides the greatest impact.

-

-

- For Policymakers:

-

Develop proportionate regulatory frameworks that protect consumers without stifling innovation. Prioritize transparency requirements, standardized disclosure formats, and mechanisms to prevent over indebtedness while preserving BNPL’s financial inclusion benefits.

-

-

- For Investors:

-

Focus on BNPL platforms with sustainable unit economics, diversified revenue streams, and robust risk management capabilities. The era of growth-at-all-costs is ending, with sustainable profitability becoming increasingly important.

Conclusion

The BNPL sector stands at a critical inflection point, transitioning from hyper-growth to sustainable scaling. The global market expansion continues, with user adoption projected to surpass 900 million globally by 2027. However, future success will require balancing growth with profitability, regulatory compliance, and responsible lending practices.

The most successful players will be those that can navigate the evolving regulatory landscape, adapt their business models to address emerging risk concerns, and continue innovating to meet evolving consumer and merchant needs. As BNPL becomes an increasingly embedded component of the global financial ecosystem, stakeholders who take a strategic, measured approach to this dynamic market will be best positioned to capture long-term value.