Private credit has evolved from a niche post-GFC workaround into a $3.5 trillion pillar of global finance, rivalling traditional bank lending and public bond markets in scale. Simultaneously, the industry’s center of gravity is shifting away from institutional-only capital formation toward a systematic campaign to capture retail and mass-affluent wealth. With product innovation lowering minimums to $2,500, the DOL proposing a landmark safe harbour for alternatives in 401(k) plans, and the “Big Seven” alternative managers collectively overseeing $4.67 trillion, the convergence of these forces represents the most consequential structural shift in credit markets since the Global Financial Crisis.

From the Margins to the Mainstream: The Private Credit Boom

Fifteen years ago, private credit was a cottage industry where a handful of specialist managers lending to mid-market borrowers that banks had abandoned in the wreckage of 2008. Today, it is the fastest-growing segment of alternative assets and a structural feature of global capital markets.

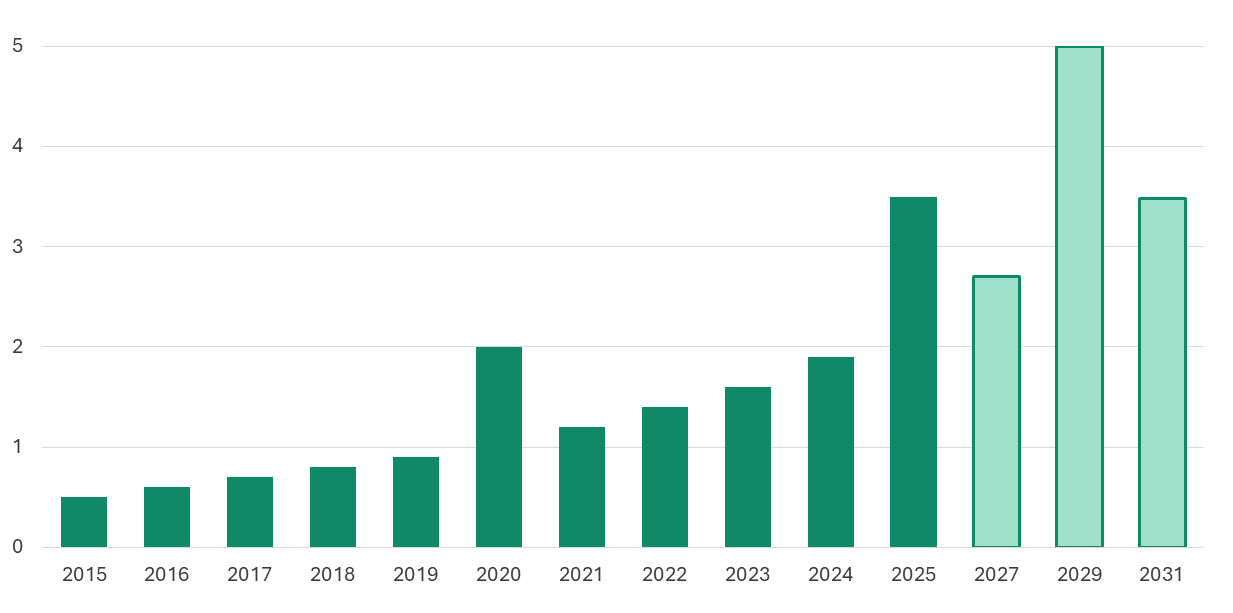

The numbers tell a story of exponential institutional adoption. Global private credit assets under management reached approximately $3.5 trillion by late 2025. This represents a near-doubling from roughly $2 trillion in 2020. U.S. market alone has grown from $500 billion to approximately $1.3 trillion over the past five years. As per estimates, the global market will reach $5 trillion by 2029.

Global Private Credit AUM Trajectory (in USD Trillion)

What makes this expansion structurally significant rather than merely cyclical is the breadth of the deployment base. Capital deployment surged to $592.8 billion in 2024, a 78% increase over 2023 volumes. The asset class has diversified well beyond its direct lending origins: corporate lending, asset-backed finance, real estate debt, infrastructure credit, and specialty finance all contributed to expanded activity in 2024. Direct lending remains the dominant strategy at approximately 66% of the market, but specialty finance is the fastest-growing segment, projected to compound at nearly 14% annually through 2031.

Geographically, North America continues to anchor the market with roughly 60% of global AUM. But Europe now accounts for close to 30%, a notable increase driven by Basel 3.1 implementation and a surge in significant risk transfer (SRT) transactions. The Asia-Pacific region, though still the smallest by absolute share, is projected to grow at 12.5% CAGR through 2031, driven by infrastructure demand and supply-chain reorientation.

Why Now? The Structural Drivers Behind the Boom

The growth of private credit is not an accident of timing. It is the product of at least four mutually reinforcing structural forces that show no signs of abating.

1. Regulatory-Driven Bank Retrenchment

The single most important catalyst remains regulatory capital reform. The finalization and phased implementation of Basel III (and its iterations — Basel 3.1 in Europe, the Basel III Endgame in the United States) have materially increased the capital intensity of select corporate lending, leveraged finance, and project-finance exposures on bank balance sheets. The effect is mechanical i.e. higher risk-weighted asset charges push certain lending activities below banks’ internal return hurdles, creating a structural supply gap that private credit managers have filled.

Many banks are actively partnering with private credit platforms. Credit lines extended by the largest U.S. banks to private credit vehicles grew approximately 145% between 2020 and 2024, reaching roughly $95 billion. ABN AMRO’s inaugural $2.35 billion significant risk transfer transaction with Blackstone-managed funds, announced in December 2025, exemplifies the emerging symbiosis: the bank reduced risk-weighted assets by $1.88 billion while retaining its client relationships.

2. The Maturity Wall and Refinancing Demand

A wave of leveraged loan and high-yield bond maturities is approaching in 2026 and 2027, creating substantial refinancing demand. Private credit managers with deployable funds are well-positioned to capture this flow, particularly for borrowers seeking certainty of execution and flexible terms that public markets may not provide under volatile conditions.

3. The AI and Energy Transition Capex Cycle

The buildout of AI infrastructure such as data centers, power generation, semiconductor facilities and the broader energy transition represent a multi-trillion-dollar capex supercycle. Private credit is increasingly financing these projects through bespoke structures that blend infrastructure debt with corporate credit characteristics. Blackstone alone manages a data-center portfolio valued at over $50 billion. Power Sustainable Infrastructure Credit announced a December 2025 final close with over $1 billion in committed capital targeting energy, transport, and digital infrastructure.

4. Insurance Capital Reallocation

Insurance companies are allocating aggressively to private credit as a yield-enhancing replacement for traditional fixed income. The integration of insurance balance sheets into alternative asset platforms exemplified by Apollo’s deep partnership with Athene creates a structural, long-duration source of capital that reduces dependence on fundraising cycles. Over 90% of institutional investors now hold private credit allocations.

For banks, the question is no longer whether to engage with private credit, but how. The emerging playbook combines originate-to-distribute models, SRT partnerships, and co-lending platforms. Banks that treat private credit managers solely as competitors risk losing both deal flow and the fee income that partnership structures can preserve.

The Retailization Thesis: The Most Consequential Shift in a Generation

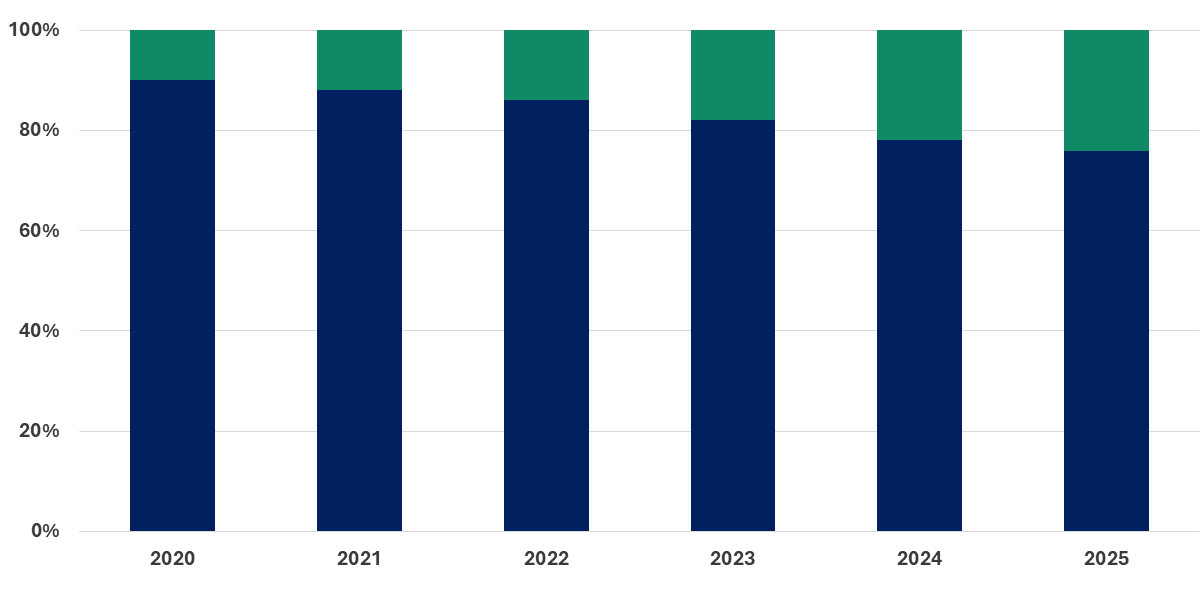

If the first act of private credit’s story was institutional adoption, the second act, now well underway, is the systematic campaign to capture retail and mass-affluent capital. The scale of the opportunity is enormous: global wealth management platforms oversee tens of trillions of dollars, yet retail allocations to private markets remain a fraction of the 30–50% allocations common among institutional portfolios.

The retail and mass-affluent investors now account for 24% of global private credit AUM, a share that is expected to grow materially in the coming years. Non-traded business development companies (BDCs) have raised $167 billion and interval funds $126 billion through Q3 2025. Total AUM in funds with private asset exposure and limited liquidity exceeded $534 billion by year-end 2025, adding roughly $100 billion in a single year.

Private Credit: Institutional vs. Retail Capital

1. The Product Innovation Engine

The traditional drawdown limited-partnership structure with 10-year lockups, capital calls, and multi-million-dollar minimums is fundamentally incompatible with retail distribution. The industry’s response has been a wave of product engineering designed to bridge the liquidity expectations of individual investors with the illiquidity premium that private markets offer.

Three product formats have emerged as the primary vehicles for Retailization:

-

-

- First, evergreen (perpetual) funds that eliminate fixed maturity dates and allow continuous subscriptions and periodic redemptions.

- Second, semi-liquid structures including interval funds and tender-offer funds that offer quarterly or monthly redemption windows.

- Third, exchange-traded products that provide daily liquidity through public-market wrappers around private credit exposure.

-

Minimum investment thresholds have dropped from $5 million to as low as $2,500 in some structures, dramatically expanding the addressable market.

In Europe, the regulatory catalyst has been ELTIF 2.0 (effective January 2024), which overhauled the European Long-Term Investment Fund framework. The structural shift has been immediate: quarterly-liquidity ELTIF launches surged from 9% of all launches pre-ELTIF 2.0 to 31% post-reform. Private debt now leads the ELTIF universe at 35% of strategy share, and 63% of new funds carry minimum subscriptions below €20,000.

The Private Wealth NAV Explosion

The velocity of capital formation in the wealth channel is striking. Data shows that private equity and infrastructure products aimed at private wealth investors now collectively represent a NAV of approximately $125 billion, an 80% year-over-year increase. Gross inflows across these diversified products show annualized growth rates of 60–70% as of Q3 2025. While private credit (primarily direct lending) currently accounts for roughly 50% of private wealth retail NAV, the market is actively diversifying into infrastructure, secondaries, and buyout strategies.

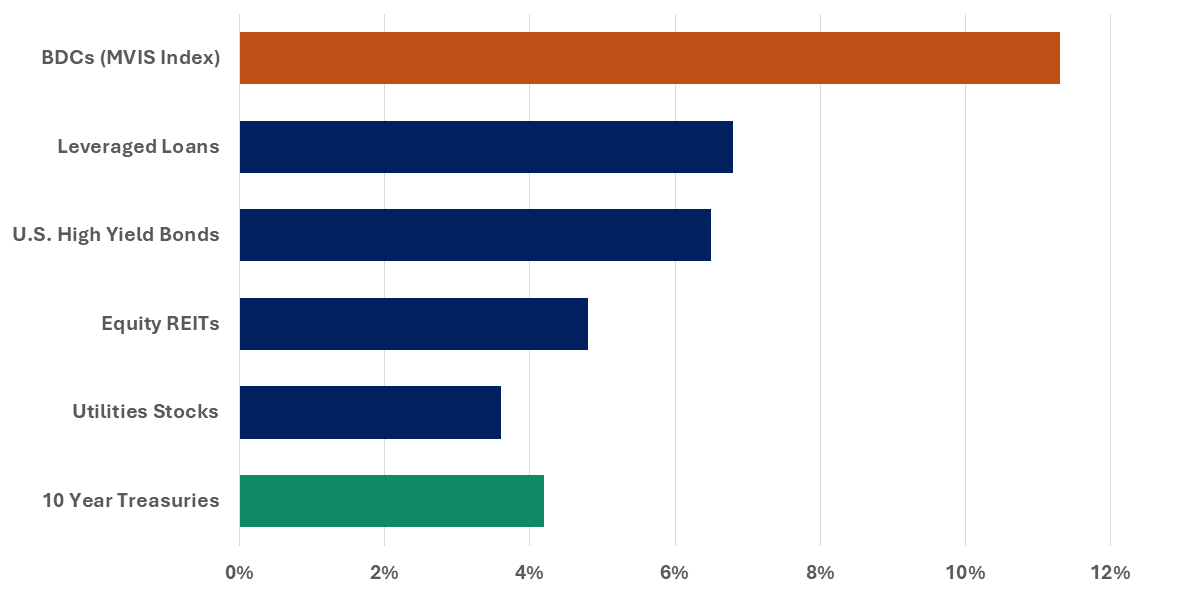

Yield Comparison Across Income Asset Classes

The 401(k) Frontier: A $12 Trillion Opportunity Takes Shape

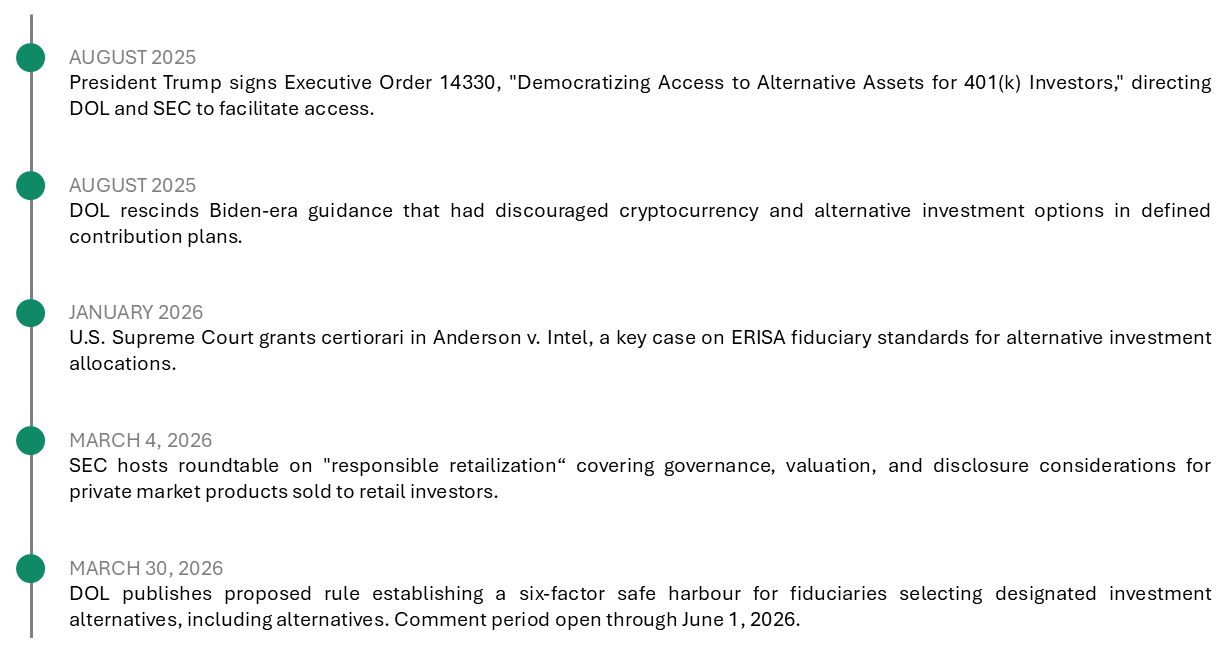

On March 30, 2026, U.S. Department of Labor unveiled a proposed rule that could represent the single largest structural catalyst for private credit growth in the next decade. The rule would create a process-based safe harbour under ERISA for plan fiduciaries selecting alternative investments including private equity, private credit, real estate, infrastructure, and digital assets as designated investment alternatives in 401(k) plans.

The context is critical. While defined benefit (pension) plans have allocated meaningfully to alternatives for decades, defined contribution plans which now hold over $12 trillion in assets have effectively been a walled garden of publicly traded mutual funds and index funds. Not because ERISA prohibited alternatives, but because the litigation risk was prohibitive. The DOL’s proposed rule noted that over 500 ERISA fee cases have been filed since 2016, producing more than $1 billion in settlements.

The Regulatory Timeline

The proposed safe harbour requires fiduciaries to evaluate six factors: performance, fees, liquidity, valuation, performance benchmarks, and complexity. Notably, the rule explicitly acknowledges that 401(k) plans are long-term savings vehicles and that there is no requirement to select only fully liquid products, a significant philosophical shift that could open the door to semi-liquid private credit structures within target-date funds and managed accounts.

It may take years before courts validate the safe harbour’s protections, and plan sponsors may wait for that judicial clarity before acting. The rule also does not address the SEC’s definitions of “accredited investor” and “qualified purchaser,” which could limit the universe of eligible products. Nevertheless, the directional signal is unmistakable i.e. the regulatory architecture for retail access to private markets is being built in real time.

The Arms Race: Who Is Winning the Retail Distribution Battle

The seven largest publicly traded alternative asset managers (Blackstone, Apollo, KKR, Carlyle, Ares, TPG, and Blue Owl) collectively oversaw $4.67 trillion in AUM at year-end 2025. Assets in perpetual (evergreen) strategies reached nearly $2 trillion across these firms, representing 42% of total AUM. The race for private wealth shelf space has become the primary strategic battleground.

In Europe, the distribution ecosystem is evolving rapidly. BlackRock and Partners Group are building a joint evergreen platform targeting high-net-worth individuals, with a $10 trillion private wealth opportunity in view. KKR’s investment in iCapital furthers its strategy of broadening individual investor access to private strategies across borders. Meanwhile, Golub Capital reported closing over $25 billion in financing commitments in 2025 and expanding its European footprint as the number-one middle market CLO issuer.

The competitive dynamics are reshaping industry economics. Private wealth channels are now the fastest-growing source of recurring fee revenue for alternative managers. Managers with strong brands, established distribution partnerships, and operationally scalable product infrastructure will consolidate share; smaller, institutionally focused managers without a credible retail strategy face structural headwinds.

Cracks Beneath the Surface: Risk Factors Demanding Attention

The private credit boom is not without material risks. As the market has scaled, pockets of stress have emerged and the retailization trend introduces a new category of vulnerability: the behaviour of non-institutional investors during periods of market dislocation.

The Redemption Pressure Test

The fourth quarter of 2025 delivered the first serious stress test for semi-liquid private credit structures. Redemptions as a share of beginning-of-quarter NAV in the non-listed BDC space nearly tripled to 4.71%. Among BDCs with over $1 billion in aggregate NAV, redemption volumes surged 217% quarter over quarter. In Q1 2026, Blackstone raised quarterly redemption limits on its flagship BCRED fund from the standard 5% to 7.9% to meet rising investor demand. Most significantly, Blue Owl halted quarterly redemptions entirely in favour of capital distributions, a decision that had major affect on its stock price.

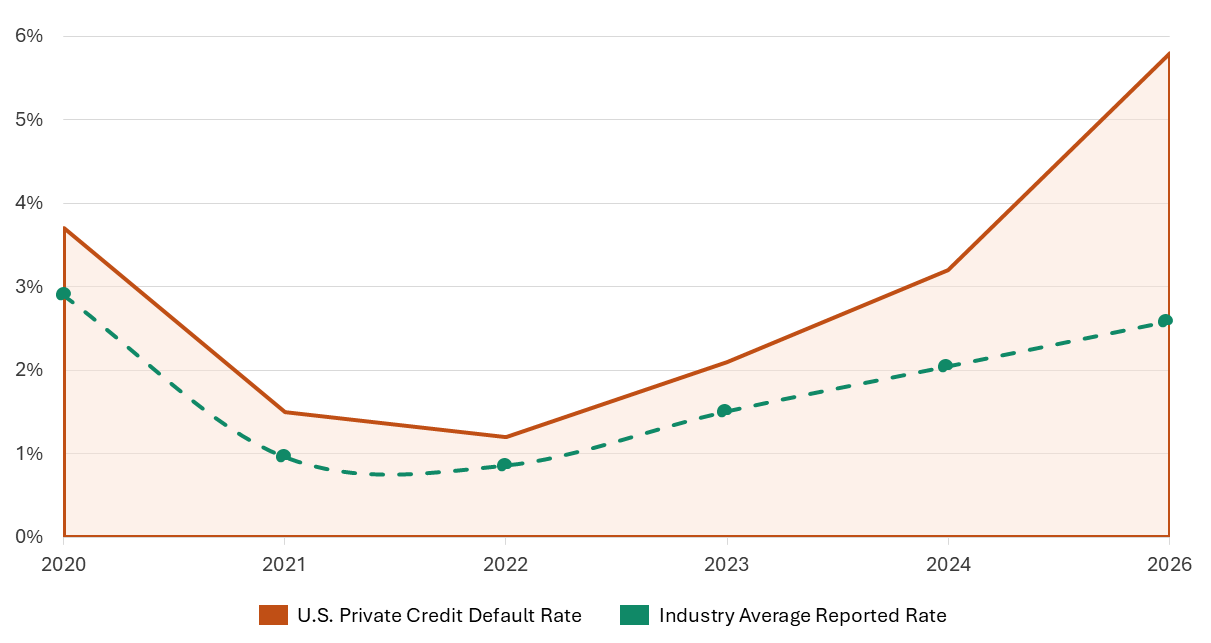

Default Rates: The Headline vs. Reality Gap

Commonly cited private credit default rates of 2–3% mask a more nuanced picture. U.S. private credit default rate reached 5.8% for the trailing twelve months through January 2026, the highest level since the rating agency began tracking the metric. The widespread use of payment-in-kind (PIK) interest where borrowers pay interest by issuing additional debt rather than cash is a clear signal of cash-flow stress. PIK structures preserve headline metrics but increase principal balances and defer risk recognition.

Private Credit Default Rate Trajectory

Strategic Implications for Banks and Financial Institutions

For banks and financial institutions, the convergence of the private credit boom and retailization creates both competitive pressure and strategic opportunity. The institutions that adapt will not only defend their existing franchise but capture new revenue streams.

1. Embrace Originate-to-Distribute and SRT Partnerships

The ABN AMRO–Blackstone model is instructive. Banks that develop programmatic SRT capabilities can optimize risk-weighted assets, generate fee income from distribution, and maintain client relationships, all while transferring first-loss risk to private capital. European banks are further ahead on this curve, but U.S. banks are catching up rapidly.

2. Build or Acquire Wealth-Channel Distribution

The wealth management arms of banks are uniquely positioned to distribute private credit products to high-net-worth and mass-affluent clients provided they develop the operational infrastructure for semi-liquid products (subscription processing, NAV reporting, redemption management). Joint ventures with established alternative managers, as Barclays did with AGL Credit Management and Wells Fargo with Centerbridge, can accelerate time to market.

3. Develop Proprietary Private Credit Capabilities

Several banks are moving beyond distribution to build proprietary direct lending and asset-backed finance platforms. This requires underwriting expertise, portfolio management capability, and a willingness to accept the lower liquidity and longer duration of private credit assets. For banks with strong mid-market franchises, the economics are compelling.

4. Prepare for Retirement-Channel Distribution

The DOL’s proposed rule, if finalized, will create demand for private credit products specifically structured for defined contribution plans. These products will need to satisfy the six-factor safe harbour (performance, fees, liquidity, valuation, benchmarks, complexity) while offering competitive returns. First movers who develop retirement-eligible private credit products will access a structural, long-duration capital pool that transforms their fundraising economics.

What Comes Next: Outlook for 2026–2028

1. Market Consolidation

Scale advantages in distribution, technology, and brand recognition will accelerate consolidation among alternative managers. Smaller managers without a credible retail strategy will face fundraising headwinds. 2025 was already the second-best year on record for GP-level deal value at $25.1 billion. It will further intensify as the cost of building retail-grade operational infrastructure rises.

2. Asset-Backed Finance

As direct lending spreads compress and competition intensifies, managers are pivoting toward asset-backed finance (ABF) i.e. lending against tangible collateral including auto loans, equipment, consumer credit, and trade receivables. ABF offers diversification away from corporate credit, self-amortizing structures, and multiple layers of credit enhancement.

3. Transparency and Technology as Competitive Differentiators

As retail capital scales, demand for real-time NAV reporting, standardized performance metrics, and transparent fee disclosure will intensify. Technology platforms that enable streamlined subscription, redemption, and reporting workflows such as iCapital, CAIS, and Percent will become critical infrastructure. Managers who resist transparency will lose distribution access.

4. The Default Cycle

Rising default rates, particularly among larger deals and covenant-lite structures, will create a differentiation event. Managers with genuine credit-selection expertise, conservative underwriting standards, and active portfolio management will outperform. The era of passive allocation to private credit as a homogeneous yield product is ending.