Executive Summary

Europe is in the early stages of the most consequential defense build-up since the Cold War. Triggered by Russia’s full-scale invasion of Ukraine in February 2022 and intensified by evolving transatlantic dynamics under the second Trump administration, the continent’s security architecture is undergoing a structural overhaul. At the NATO Summit in The Hague in June 2025, allied leaders agreed to a new investment framework committing member states to 5% of GDP in combined defense and security-related spending by 2035 with a core floor of 3.5% allocated to military capabilities.

In 2025, all 32 NATO allies met or exceeded the prior 2% of GDP target for the first time, with the alliance-wide average reaching 2.76%. European allies and Canada collectively increased defense spending by 20% year-on-year. EU member states’ defense expenditure reached an estimated €381 billion, a 63% increase from 2020. Defense investment approached €130 billion, with equipment procurement exceeding €88 billion and R&D spending projected at €17 billion. Order backlogs at major European defense contractors are at record levels. Rheinmetall closed 2025 with a backlog of €63.8 billion; BAE Systems holds over £75 billion; Saab’s stood at SEK 274.5 billion.

Germany’s domestic defense orders have more than doubled since 2019, while industrial production has risen by roughly a quarter. Ammunition production capacity across the EU expanded from 300,000 rounds per year in 2022 to an estimated 2 million by end-2025, but this remains insufficient against the attrition rates observed in Ukraine. The gap between political commitment and industrial delivery is the defining strategic risk of the rearmament cycle.

From the Wales Pledge to The Hague: The Spending Trajectory

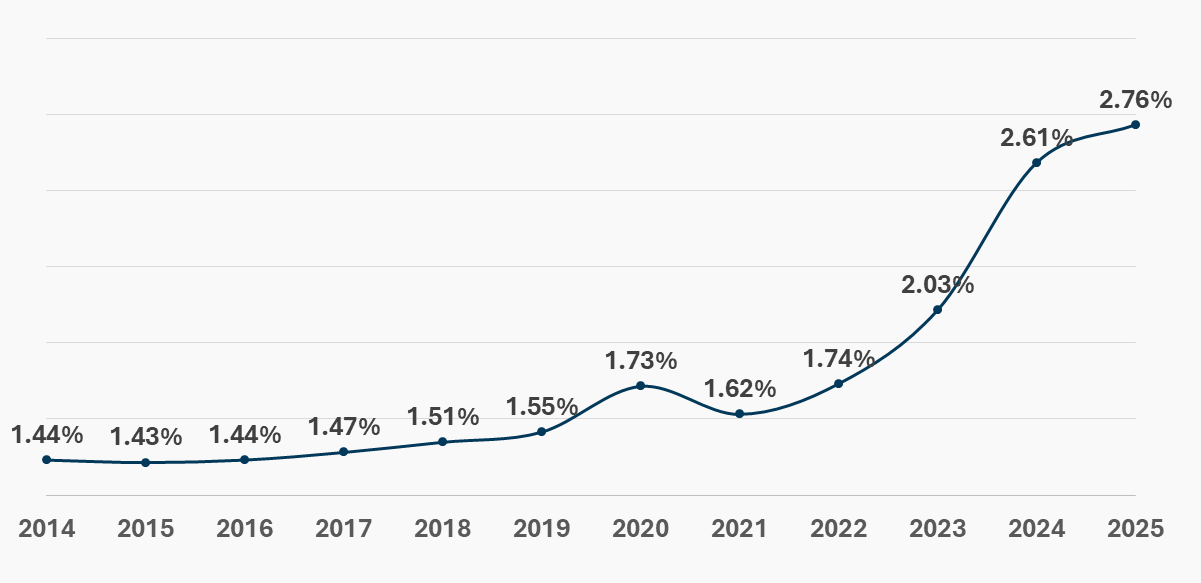

The evolution of NATO’s defense spending norms over the past decade reflects both the alliance’s belated recognition of the Russian threat and the political dynamics that shape burden-sharing negotiations. At the 2014 Wales Summit, convened in the aftermath of Russia’s annexation of Crimea, allies pledged to “aim to move towards” spending at least 2% of GDP on defense by 2024. At the time, only three member states met the benchmark. The pledge was widely treated as aspirational rather than binding.

Progress was incremental for most of the following decade. The alliance-wide average hovered between 1.43% and 1.56% of GDP from 2015 through 2019. It rose modestly in 2020 and 2021, partly due to pandemic-era GDP contractions that inflated the ratio. The genuine inflection point came in 2022, following Russia’s full-scale invasion of Ukraine. By 2023, the average had reached 2.03%. In 2024, it accelerated to 2.61%, and in 2025 it hit 2.76%.

NATO average defense spending as a share of GDP since 2014

The Hague Summit in June 2025 marked a qualitative shift. Under sustained pressure from the United States where President Trump had made allied spending a central demand, NATO leaders adopted a new investment framework structured around a 5% of GDP commitment by 2035. Critically, this breaks into two tiers: 3.5% for core military capabilities (force structure, equipment, operations) and 1.5% for broader security-related expenditure encompassing critical infrastructure protection, cyber defense, civil resilience, and defense industrial base strengthening. Allies agreed to submit annual plans demonstrating incremental progress toward these targets, with a review scheduled for 2029.

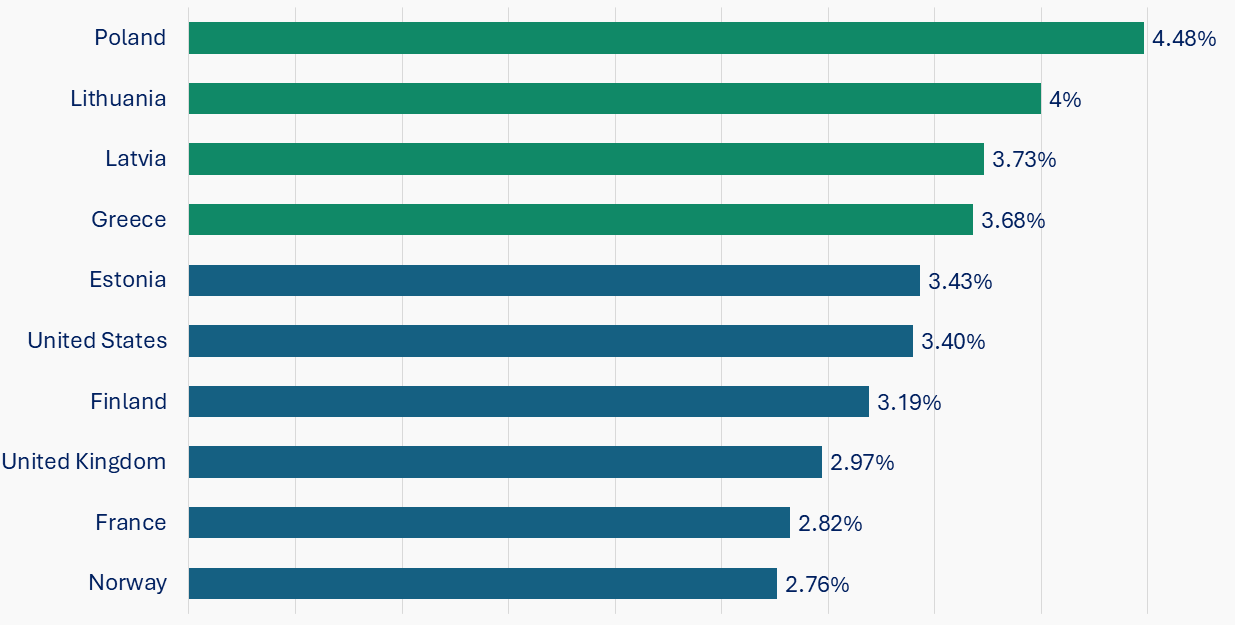

The political dynamics are not uniform. Poland leads among all NATO members at 4.48% of GDP, followed by Lithuania (4.00%) and Latvia (3.73%). Northern and Eastern European states have broadly committed to reaching 3.5% by 2029 or sooner. Conversely, Spain rejected the 5% framework entirely, capping its ambition at 2.1% of GDP, a position that drew pointed criticism from Washington and prompted discussion of alternative burden-sharing enforcement mechanisms. For industry stakeholders, it signals that demand will be geographically concentrated in Northern, Eastern, and core Western European markets for the near term.

Top 10 Allies by Defense Spending as Share of GDP in 2025

The Fiscal Architecture: EU Instruments and Collective Procurement

Alongside the NATO-level commitments, the European Union has constructed a parallel institutional architecture designed to incentivize joint procurement, reduce market fragmentation, and accelerate the scaling of the European Defense Technological and Industrial Base (EDTIB). The scale of ambition is reflected in the numbers: the EU’s next multiannual budget cycle is expected to include a Security, Defense & Space heading of approximately €131 billion, representing a tenfold increase over the current period.

Several instruments are already operational or in advanced stages of deployment. The Security Action for Europe (SAFE) facility provides €150 billion in preferential loans to member states for defense procurement, with 19 member states having fully subscribed. The European Defense Industry Program (EDIP), granted final Council approval in December 2025, mobilizes €1.5 billion in grants for 2025–2027 to boost defense industrial capacity, with €300 million earmarked for Ukraine’s defense industry. The European Defense Fund (EDF) provides €9.45 billion for 2021–2027 in R&D grants. Additional instruments include ASAP (€500 million for ammunition production), EDIRPA (€300 million for joint procurement), and the European Peace Facility, whose ceiling has been lifted to €17 billion.

The Roadmap further identifies four flagship programs: the European Drone Defense Initiative (initial capability by end-2026, full functionality by end-2027), the Eastern Flank Watch to fortify the EU’s eastern land and maritime borders, the European Air Shield for integrated multi-layered air and missile defense, and the European Space Shield for protection of EU space assets.

For non-European suppliers, the implications are stark. Germany’s procurement data illustrates the shift where its new military procurement plan shows 154 major defense purchases planned through 2026, with only 8% allocated to U.S. suppliers, a dramatic reversal from recent years when Berlin was one of Washington’s largest defense buyers. The SAFE loan conditions explicitly favour European manufacturers, and American firms are largely excluded unless Washington negotiates bilateral agreements with Brussels, which has not yet occurred.

Industrial Mobilization: The Supply-Side Response

EU member states’ defense expenditure trajectory captures the scale of the demand signal. Spending rose from approximately €234 billion in 2020 to an estimated €381 billion in 2025. Investment across equipment and R&D accounted for 31% of total expenditure in 2024, with equipment alone exceeding €88 billion. Defense R&D spending expanded from €13 billion in 2024 to a projected €17 billion in 2025.

The ammunition sector exemplifies both the progress and the constraints. EU production capacity for artillery ammunition rose from approximately 300,000 rounds per year in 2022 to an estimated 2 million by end-2025, a pace of expansion that exceeds peacetime industrial growth rates by a factor of three. Rheinmetall is building Europe’s largest ammunition plant in Unterlüß, Lower Saxony, targeting output of hundreds of thousands of shells annually by 2027. In February 2026, NSPA awarded Rheinmetall a contract valued at approximately €200 million for 120mm tank ammunition.

Across the broader defense industrial base, major European contractors reported exceptional financial performance in 2025. Rheinmetall posted annual sales of €9.9 billion (up 29% year-on-year), with an operating profit of €1.8 billion and a record order backlog of €63.8 billion. The company forecasts 2026 sales of €14.5 billion, representing growth of 40–45%. BAE Systems holds an order backlog exceeding £75 billion, is doubling Eurofighter Typhoon output, and secured a major £10 billion frigate contract with Norway. Saab reported 22% sales growth in H1 2025, raised its full-year growth forecast to 16–20%, and closed the year with an order backlog of approximately USD 30 billion. Thales saw 8.1% revenue growth in H1 2025 and raised its full-year forecast, while Leonardo reported 12.9% sales growth.

Selected Major European Defense Contracts, 2025–2026

|

Contractor |

Customer | Programme |

Value / Scope |

| BAE Systems | Norway | Type 26 Frigates | £10 billion |

| KNDS / Rheinmetall | Germany / Netherlands | Boxer IFVs (200+) | €3.4 billion |

| Rheinmetall | Netherlands | Skyranger 30 GBAD | High triple-digit € million |

| Saab | Poland | A26 Submarines (Orka) | Multi-billion € |

| Saab | France | GlobalEye AEW&C (x2) | Undisclosed |

| BAE Systems | Türkiye | Typhoon Aircraft (20) | Multi-billion £ |

| Rheinmetall / NSPA | Multiple NATO | 120mm Tank Ammunition | €200 million |

| CV90 Consortium | 6-nation coalition | CV90 Mk IV IFVs | Joint procurement (2026) |

The Production Paradox: Demand Outpacing Output

The most critical finding from the 2025–2026 data is the widening gap between the demand signal and industrial output. Germany provides the clearest illustration. Between 2025 and early 2026, the six-month moving average of domestic defense orders rose by approximately 100%, while domestic sales increased by about 25%. Industrial production, however, edged up only marginally. Since 2019, German defense demand has more than doubled, while production has risen by roughly a quarter. Demand is growing five to six times faster than output.

This is not primarily a capital problem. European governments are directing unprecedented volumes of funding into defense. It is, fundamentally, a structural incentive problem. Defense companies have spent two decades optimizing for stable margins, predictable returns, and low political risk. Expanding production capacity requires irreversible capital expenditure across new factories, tooling, and workforce training that boards are reluctant to undertake when contract durations are short, political commitments are potentially reversible with each electoral cycle, and order volumes remain uncertain beyond the near term.

The workforce constraint is equally significant. The EU’s Defense Readiness Roadmap projects a need for 600,000 skilled workers for the defense industry by 2030, with 200,000 required by 2026. This is not merely a hiring challenge but it requires cross-sector talent reallocation in economies already facing demographic headwinds and competition for technical skills from the technology and energy sectors.

Supply chain vulnerabilities add a further layer of complexity. China controls approximately 90% of the world’s rare-earth magnet production and supplies 98% of Europe’s imports of these materials, which are essential for drone motors, missile guidance systems, and a wide range of other defense applications. Beijing’s recent imposition of export restrictions requiring government approval for foreign use of rare-earth materials exposes a fundamental contradiction. Europe is seeking to reduce dependence on American defense suppliers while remaining critically dependent on Chinese-controlled inputs for the weapons it intends to build.

Strategic Implications for Industry Stakeholders

1. Demand Concentration and Market Geography

The rearmament spend will not be evenly distributed. Northern and Eastern European markets i.e. Poland, the Baltic states, the Nordics, Germany, and the Netherlands will absorb a disproportionate share of procurement budgets. Poland’s sustained spending above 4% of GDP, combined with its ambitious modernization programs (Orka submarines, Patriot-class air defense, K2 tanks), positions it as a leading demand center. The Baltic states, while small in absolute terms, are among the most committed spenders relative to GDP and are prioritizing air defense, maritime surveillance, and border fortification.

2. European Preference and Supplier Realignment

The EU’s 55% European procurement target by 2030 and the SAFE facility’s conditions favoring European manufacturers are creating a structural preference for EDTIB suppliers. This does not fully exclude non-European firms. Lockheed Martin’s pairing with Saab, Anduril’s drone venture with Rheinmetall, and RTX’s partnership with MBDA demonstrate that transatlantic firms can participate through joint ventures and technology partnerships. However, the default procurement pathway is shifting decisively toward European primes.

3. The Joint Procurement Imperative

The push toward 40% joint procurement by end-2027 creates both opportunities and constraints. The six-nation CV90 Mk IV infantry fighting vehicle program (Estonia, Lithuania, Netherlands, Norway, Finland, and Sweden) illustrates the model: standardized variants with common training, ammunition, and spare parts. For OEMs, multinational contracts offer scale and production certainty. For subcontractors and component suppliers, they require the ability to service multiple national requirements from integrated production lines. Firms that can navigate multi-jurisdictional offset requirements and interoperability standards will capture disproportionate share.

4. Priority Capability Areas

The convergence of NATO capability targets and EU flagship programs points to several priority domains that will command the largest capital allocation through the end of the decade. Air and missile defense sits at the apex, with the Hague Declaration calling for a fivefold increase in allied air defense capabilities. The European Air Shield, Rheinmetall’s Skyranger family, and continued Patriot and IRIS-T procurement represent a multi-billion-euro addressable market.

Counter-drone systems are emerging as a standalone capability category, with the European Drone Defense Initiative targeting initial operational capability by end-2026. Ammunition and munitions replenishment remains an urgent priority, with production capacity still below wartime consumption rates. Naval modernization, electronic warfare, satellite-based intelligence, and cyber defense round out the priority stack.

5. The Financing Layer

The SAFE facility’s €150 billion in loans, the EDIP’s €1.5 billion in grants, and the EDF’s €9.45 billion in R&D funding create a layered financing architecture that extends beyond traditional national defense budgets. For defense technology startups and mid-tier firms, the EDIP and EDF grant mechanisms, particularly the move toward open-topic competitions modelled on the U.S. SBIR program, represent new market entry pathways.

France’s AID innovation agency announced a joint program with Ukraine’s defense innovation cluster in February 2026, offering competitive grants for defense startups in both countries. As of January 2026, Europe hosted a growing but still modest cohort of defense startups compared to the United States, underscoring the scale of the opportunity for firms positioned to meet emerging capability requirements.

Conclusion: The Credibility Test

The scale of political commitment to European rearmament is no longer in question. The fiscal trajectory is clear: from 1.4% of combined GDP in 2014 to 2.3% in 2025, with a binding path toward 3.5% core defense spending by 2035. The institutional architecture i.e. NATO’s capability targets, the EU’s SAFE facility, EDIP, and the Defense Readiness Roadmap provides the framework. The demand signal to industry has never been stronger.

What remains in question is the conversion rate. The speed and efficiency with which political commitments and financial resources are translated into deployed military capability. The production paradox demand growing five to six times faster than output will not resolve itself through additional budget appropriations alone. It requires long-duration contracts that make industrial expansion rational, workforce development at a scale not seen in a generation, supply chain diversification away from Chinese-controlled critical minerals, and procurement reform that prioritizes speed and accepts greater risk.

For stakeholders in the defense industry whether major contractors, mid-sized suppliers, technology startups, or investors, the key strategic question is whether Europe can maintain its current sense of urgency beyond the next election cycle. Companies that act on the assumption that this momentum will continue, by investing in production capacity, skilled workforce, and advanced capabilities, are likely to benefit from long-term growth opportunities.