Global electricity demand is growing at over 3.5% annually through 2030, driven by data centers, electric mobility, industrial electrification, and cooling loads. At the same time, grid infrastructure built for a centralized, unidirectional model is being asked to absorb bidirectional flows from millions of distributed energy resources, manage AI-driven demand spikes concentrated in narrow geographies, and maintain reliability against increasingly volatile weather patterns.

In this environment, the bottleneck is no longer generation capacity. It is intelligence i.e. the ability to observe, predict, and act on what is happening at every node of the distribution network in real time. Grid edge analytics software, platforms that ingest data from smart meters, sensors, inverters, and grid devices and convert it into operational and strategic intelligence, is rapidly emerging as the technology layer that determines whether utilities can bridge the gap between physical infrastructure constraints and surging system complexity.

The Structural Imperative: Why Analytics Has Moved from Back Office to Grid Edge

For most of the last century, electricity grids operated within a model that was data-poor by design. Power flowed in one direction, from centralized generation through transmission and distribution to passive consumers. Analytics, where it existed, was retrospective i.e. monthly billing cycles, periodic asset inspections, post-event outage analysis. The grid did not need to think at the edge because there was nothing intelligent happening there.

Three forces are dismantling this paradigm simultaneously:

-

-

- The demand acceleration

-

Global electricity demand is now growing at approximately 2.5 times the rate of overall energy demand. The average annual demand growth exceeding 3.5% through 2030, driven in significant part by data centers, whose electricity consumption is expected to triple by 2035. AI alone could account for up to 50% of US electricity demand growth between 2025 and 2030, with high-end scenarios projecting 157 GW of additional demand by 2029. This load is not uniformly distributed but it is concentrated in specific geographies, often near existing clusters, placing extraordinary pressure on local distribution networks.

-

-

- The DER inflection

-

Distributed energy resources such as rooftop solar, behind-the-meter batteries, EVs acting as mobile storage, smart thermostats, and flexible industrial loads are converting the distribution grid from a delivery network into a two-way market. Every DER is simultaneously a source of supply, a flexible demand asset, and a potential source of grid instability. Managing this complexity requires analytics that operate not at the control center but at the transformer, the feeder, and the meter itself.

-

-

- The infrastructure-intelligence gap

-

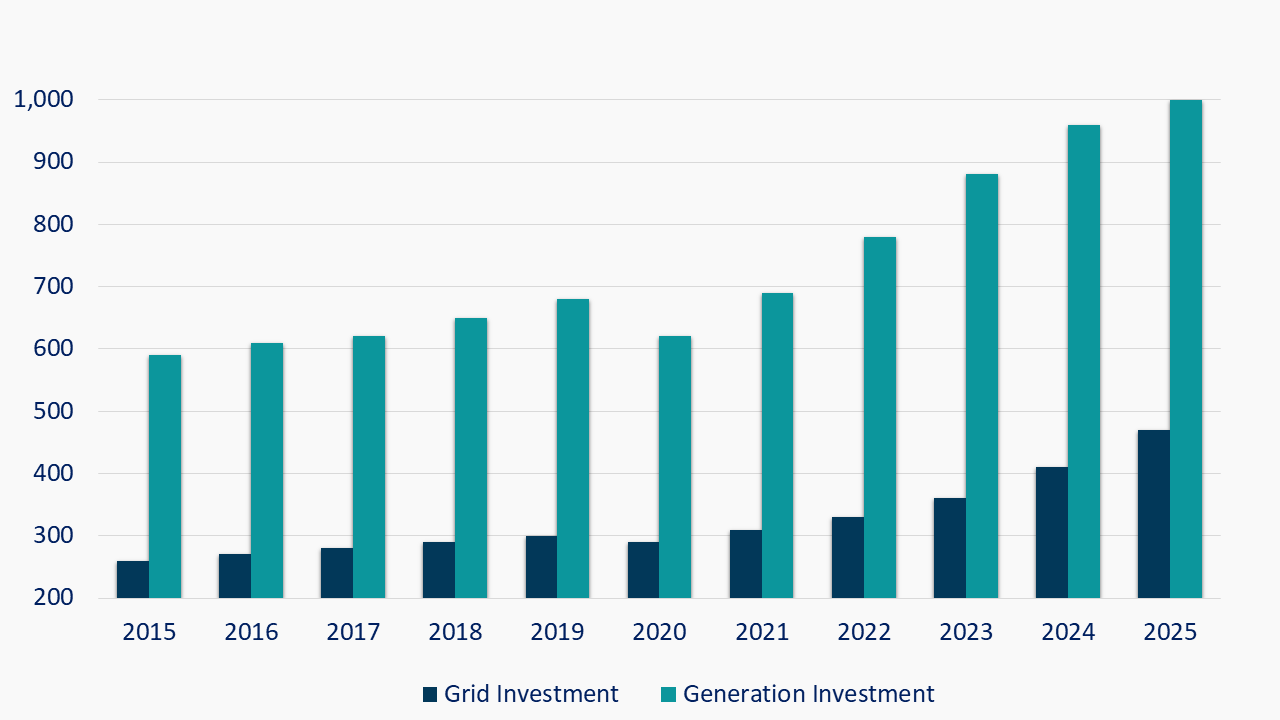

Annual global grid investment now exceeds $470 billion. To keep pace with demand, this figure needs to increase by approximately 50% to roughly $600 billion annually by 2030. Yet grid construction timelines routinely exceed those for generation and demand projects. Over 2,500 GW of renewable, large-load, and storage projects currently sit in grid connection queues worldwide. The grid-enhancing technologies and regulatory reforms could free enough capacity to connect 1,200 to 1,600 GW of these advanced-stage projects without building a single new line. This is fundamentally an analytics problem i.e. identifying where latent capacity exists, when it can be utilized, and how to dispatch flexible resources to relieve constraints in real time.

The Analytics Paradox: More Data, Less Visibility

The global smart meter installed base surpassed 1.8 billion units by the end of 2024, with projections pointing to 3 billion by 2030. North America has achieved approximately 81% smart meter penetration. China has deployed the largest absolute fleet globally. India has installed over 52.8 million meters under the Revamped Distribution Sector Scheme (RDSS) as of December 2025, with 203 million sanctioned creating one of the world’s most significant data infrastructure buildouts in progress.

Only around 100 GW of demand response is utilized globally, a fraction of the technical potential. Consider that residential air conditioning alone contributes approximately 600 GW of peak electricity demand worldwide, yet flexible demand response from these loads remains marginal. In India, where smart meter deployment is accelerating at roughly 80,000–100,000 installations per day, the prepaid activation rate, a basic indicator of whether meter data is being used for anything beyond billing, sits below 2%.

In Europe, the gap takes a different form. Approximately 50% of European distribution system operators still lack an accurate network model, the foundational data layer required before any advanced analytics can function. Also, only 3–5% of available grid flexibility is being activated across European networks. Grid congestion management costs tripled in Germany, United Kingdom, and United States between 2019 and 2022.

What Grid Edge Analytics Actually Does: A Functional Architecture

Grid edge analytics software encompasses a set of capabilities that operate across the distribution value chain, from the smart meter through the distribution transformer and feeder to the control center and customer-facing applications. The technology stack typically includes four functional layers.

Data Ingestion and Normalization: Aggregating high-frequency data streams from smart meters (interval reads, voltage and current waveforms, event logs), grid sensors (temperature, loading, fault indicators), DER systems (inverter output, battery state-of-charge, EV charging profiles), and SCADA/OMS platforms. The challenge at scale is not volume alone but heterogeneity where utilities operate equipment from dozens of vendors, across multiple communication protocols, with varying data quality.

Edge Processing and Inference: Increasingly, analytics are being executed not in the cloud but at the meter or gateway device itself. This is the “distributed intelligence” model pioneered by Itron and now adopted across the industry. Processing data at the edge reduces latency for time-critical decisions (autonomous load shedding, fault isolation, voltage regulation), reduces communication bandwidth requirements, and enables operation even when cloud connectivity is interrupted, a critical consideration for resilience.

Predictive and Prescriptive Analytics: Machine learning models that forecast load at the individual meter, transformer, and feeder level; predict asset failure before it occurs; detect non-technical losses and energy theft patterns; optimize DER dispatch across portfolios; and generate actionable alerts for field crews. This layer is where AI/ML delivers the highest-value use cases and where competitive differentiation among vendors is sharpest.

Decision Orchestration: The integration layer that connects analytics outputs to operational systems dispatching demand response events, adjusting voltage set points, scheduling maintenance, coordinating DER charging and discharging, and feeding optimized scenarios back to planning tools. This is the layer most utilities are still building.

Global Grid Investment vs. Generation Investment (2015–2025)

Regional Landscape: Divergent Paths, Converging Needs

1. North America: Scale deployment meets AI integration

United States represents the single largest grid investment market globally, with $115 billion in grid capital expenditure in 2025, approximately a quarter of the worldwide total. North America has achieved approximately 81% smart meter penetration, with 152.4 million electricity meters installed, creating a mature data infrastructure upon which advanced analytics can be layered.

The strategic frontier in North America is the integration of AI at the grid edge. Itron’s collaboration with NVIDIA, announced in March 2025, combines Itron’s distributed intelligence platform with NVIDIA’s Jetson edge computing platform to enable real-time waveform data processing, using AI to identify systemic risks such as faults and wildfire precursors directly at the meter. Similarly, Itron’s partnership with Microsoft integrates Gen AI Copilot capabilities into its edge operating system, allowing utility operators to query complex grid data using natural language, a step-change in operational accessibility. Landis+Gyr’s Revelo platform, deployed with utilities like Southwestern Electric Cooperative, delivers grid-edge sensing and real-time load disaggregation capabilities directly from the meter.

The demand-side catalyst is also uniquely intense in North America: AI data center interconnection queues now rival and in some cases exceed renewable energy queues in transmission bottleneck severity.

2. Europe: Bridging the model gap under regulatory reform

Europe’s grid edge analytics challenge is fundamentally one of network model accuracy and flexibility activation. With approximately 50% of DSOs operating without accurate digital network models and grid OPEX rising 25–30% due to ageing assets, the foundational prerequisites for advanced analytics are still being established across much of the continent.

Schneider Electric’s One Digital Grid Platform, launched at Enlit Europe, addresses this directly by collapsing planning, operations, and asset management into a single AI-enabled data layer. The platform’s design philosophy reflects a European reality, most utilities cannot afford to rip and replace existing systems. Interoperability and modular adoption are structural requirements.

The regulatory environment is accelerating adoption. Grid congestion management costs tripled across Germany, UK, and US from 2019 to 2022, and European regulators are increasingly mandating real-time visibility and DER coordination capabilities as conditions of network operation. The synchronization of the Baltic power system in February 2025 demonstrated both the technical achievement and the analytical complexity of managing increasingly interconnected regional networks.

3. Asia-Pacific: The volume deployment with an analytics deficit

Asia-Pacific presents the most dramatic contrast between smart meter deployment scale and analytics maturity. China dominates global smart meter shipments and has the largest installed base. India’s RDSS programme has sanctioned over 203 million meters across 45 distribution utilities in 28 states, with installation rates accelerating to 80,000–100,000 meters per day. Yet India’s analytics gap is pronounced: as of early 2026, only approximately 13.4 million of the 250 million targeted meters are communicating, and fewer than 4.8 million are operating in prepaid mode.

The structural challenge in India and similar emerging markets is sequencing. Unlike mature markets where analytics capabilities were developed alongside or even ahead of metering infrastructure, India’s RDSS deployed hardware first and is now building the analytics layer retrospectively. This creates a window of significant opportunity for analytics software providers who can deliver value from existing meter data while the infrastructure buildout continues.

In Australia, Itron’s IntelliFLEX DERMS solution manages PV solar across the three largest territories and coordinates tens of thousands of EVs, representing one of the most advanced grid edge DER management deployments globally. Norgesnett’s deployment in the Nordics represents the first large-scale grid edge intelligence installation in Northern Europe, directly addressing EV growth and rising solar generation.

4. Middle East & Africa: Nascent infrastructure, leapfrog potential

The Middle East and Africa represent early-stage markets where grid edge analytics adoption is nascent but accelerating. Jordan Electric Power Company’s partnership with Itron to deploy meter data management across 1.5 million smart meters, with capacity to add 100,000 meters annually, illustrates the trajectory. Saudi Arabia’s Vision 2030 and the UAE’s energy diversification programs are creating institutional demand for grid intelligence platforms. Sub-Saharan Africa’s distributed energy systems, often operating as microgrids or mini-grids, present a distinct use case where edge analytics can enable grid management at dramatically lower cost points than traditional centralized approaches.

Competitive Landscape: From Metering Companies to Intelligence Platforms

The competitive dynamics of grid edge analytics are being reshaped by a fundamental strategic shift i.e. the transition from hardware-led business models (selling meters and sensors) to software-and-outcome-led models (selling intelligence, optimization, and managed services). This shift mirrors the broader industrial trend toward “software-defined” infrastructure, but it carries specific implications for the energy sector.

Major Vendor Moves in Grid Edge Analytics (2025–2026)

|

Vendor |

Strategic Move | Capability Signal |

Scale Indicators |

|

Itron |

NVIDIA Jetson integration for edge AI; Microsoft Copilot for natural language grid queries; AWS, Snowflake partnerships | Full-stack edge-to-cloud intelligence with AI inference at the meter | 16M+ DI-enabled meters; 100M+ endpoints; 70 GWh dispatched in 2025 |

|

Schneider Electric |

One Digital Grid Platform launch; AutoGrid acquisition for DER orchestration; $1.9B Switch supply deal | Converged planning-operations-asset management on single AI platform | Present in 1 in 4 buildings globally; 240,000+ sites on Resource Advisor; 11% organic revenue growth Q1 2026 |

|

Landis+Gyr |

Revelo grid sensing platform; open App Ecosystem for third-party grid applications | Grid-edge sensing with waveform data for real-time load disaggregation and voltage management | 530,000-meter Rhode Island Energy deployment; cooperative utility wins |

|

Grid4C |

AI-powered predictive analytics platform; Data Science as a Service (DSaaS) model | Individual meter-level behavioural modelling; appliance-level disaggregation | Billions of daily meter reads processed; embedded analytics in third-party hardware |

|

Siemens |

Grid Software portfolio integration; digital twin capabilities for distribution networks | Enterprise-scale grid simulation and scenario planning | Broad installed base across European and global utility operations |

The partnership structures are equally revealing. Itron’s ecosystem now spans NVIDIA (edge AI compute), Microsoft (generative AI interface), AWS (cloud analytics), Snowflake (data management), Bidgely (consumer disaggregation), and NET2GRID (energy insights) creating a platform architecture rather than a point product.

Schneider Electric’s acquisition of AutoGrid added DER orchestration capabilities to its EcoStruxure stack, enabling coordination of thousands of distributed resources simultaneously, a capability directly targeted at the flexibility activation gap. Schneider’s broader strategic thesis, articulated by CEO Olivier Blum as “the Fifth Revolution” focused on intelligence, positions the company at the intersection of buildings, grid, and industrial infrastructure on a single AI platform.

Strategic Implications and the Path Forward

For stakeholders across the energy value chain, the emergence of grid edge analytics as a critical infrastructure layer creates distinct strategic imperatives.

1. For utility executives

The sequencing decision when to deploy analytics relative to metering and DER infrastructure is proving to be one of the most consequential strategic choices in grid modernization. The evidence from mature deployments in the Netherlands, Finland, and US utilities demonstrates that analytics capabilities developed 18–24 months ahead of full meter rollout generate significantly faster returns. Utilities that have deployed meters first and analytics later face multi-year delays in value realization, as India’s RDSS experience illustrates.

The platform versus point-product decision is equally material. As vendor ecosystems consolidate around Itron, Schneider Electric, and Landis+Gyr, utilities that select point products risk integration complexity and stranded investment. Conversely, early commitment to a platform ecosystem carries concentration risk. The optimal approach for most utilities will be a standards-based, interoperable core platform with selective best-of-breed applications.

2. For regulators and policymakers

The treatment of analytics software as a regulated asset, eligible for rate-based recovery and subject to performance benchmarks, is an emerging regulatory frontier. If analytics deployments can demonstrably defer infrastructure investment and improve reliability metrics, the regulatory case for rate-basing these expenditures strengthens materially. European regulators are already moving in this direction by mandating real-time DER visibility as a condition of network operation.

3. For infrastructure investors

The shift from hardware to software-and-outcomes revenue models within the grid edge sector creates different investment return profiles. Hardware businesses are inherently cyclical, tied to deployment waves. Software and managed-service businesses, once deployed at scale, generate recurring revenue with high gross margins and low marginal cost of delivery. The edge AI segment in smart grids, valued at $15.5 billion in 2025 and projected at $19.5 billion in 2026, represents one of the highest-growth segments in energy technology.

Conclusion: The Grid That Thinks at the Edge Will Win

The grid of 2030 will bear little resemblance to the grid of 2020. It will absorb power from millions of distributed sources, serve load profiles reshaped by AI workloads and electric mobility, manage billions of connected endpoints, and operate under reliability expectations that grow more demanding with every heatwave, wildfire, and policy mandate.

Meeting these demands with infrastructure alone is financially impractical and temporally impossible as grid investment needs to rise by 50% just to keep pace underscores the inadequacy of a build-only strategy. Grid edge analytics software is not a technology category. It is a strategic capability. The organizations that recognize this distinction early and invest accordingly will define the energy infrastructure of the next decade.