Introduction: Data Centers as the Backbone of the Digital and AI Economy

Data centers are purpose-built facilities that concentrate compute, storage, and networking to run the digital economy with high availability, physical security, and engineered power-and-cooling redundancy. In practical terms, a data center is the industrial backbone behind cloud services, enterprise applications, streaming, payments, logistics, and increasingly AI training and inference where workloads are both compute-dense and energy-intensive. As per estimates, global data-center electricity consumption will reach ~950 TWh by 2030, making data centers a board-level topic spanning strategy, capex, risk, and energy procurement.

From an ecosystem standpoint, the industry is structurally consolidating around hyperscalers and professional colocation platforms driven by scale economics, speed-to-market, and the need to secure land, power, and fiber in constrained metros. Over 1,100 hyperscale data centers were present globally at end-2024 which indicates hyperscalers major share in worldwide capacity and shows how enterprises think about “build vs. lease vs. cloud.”

Common Applications:

-

-

- Cloud & Saas Foundations: Iaas/Paas, Enterprise Saas, Developer Platforms, CDNS.

- Enterprise Core Systems: ERP, CRM, Databases, VDI, Collaboration, Business Continuity / Disaster Recovery.

- Data & AI: Data Lakes/Warehouses, Real-Time Analytics, AI Training Clusters, Inference at Scale and at The Edge.

- Digital Infrastructure Services: Payments, E-Commerce, Gaming, Telecom Core/Edge Functions, Media Streaming, Cybersecurity Services.

-

Primary Types of Data Centers:

-

-

- Hyperscale (owned/operated by cloud giants): Very large campuses optimized for cost per MW, automation, and standardization.

- Colocation / Retail & Wholesale: Shared facilities where enterprises lease space/power; ranges from cabinet-level to multi-MW suites.

- Enterprise / On-premises: Dedicated facilities for regulatory, latency, or legacy reasons; increasingly modernized as “private cloud” nodes.

- Edge / Distributed Micro Data Centers: Smaller footprints close to users/devices for low-latency workloads (content, IoT, industrial, telco).

-

Technological Trends Shaping the Next Generation of Data Centers

The data center landscape is undergoing a profound transformation driven by rapid advances in computing workloads particularly artificial intelligence as well as increasing demands for efficiency, sustainability, and resilience. A recent core trend is the integration of AI-enabled infrastructure management and optimization systems, where machine learning is not only a workload but also a tool for operational efficiency.

For example, reinforcement learning models are being developed to dynamically optimize cooling and energy use in high-performance facilities, balancing thermal performance with energy consumption in real time. At the same time, research into next-generation interconnects, such as terahertz wireless communication architectures, is underway to overcome the limitations of traditional wired data center fabrics, promising ultra-low latency and high throughput for distributed AI clusters. These technological innovations reflect a shift toward holistic design approaches that combine hardware evolution, advanced control systems, and real-time analytics to meet demanding compute and energy efficiency targets.

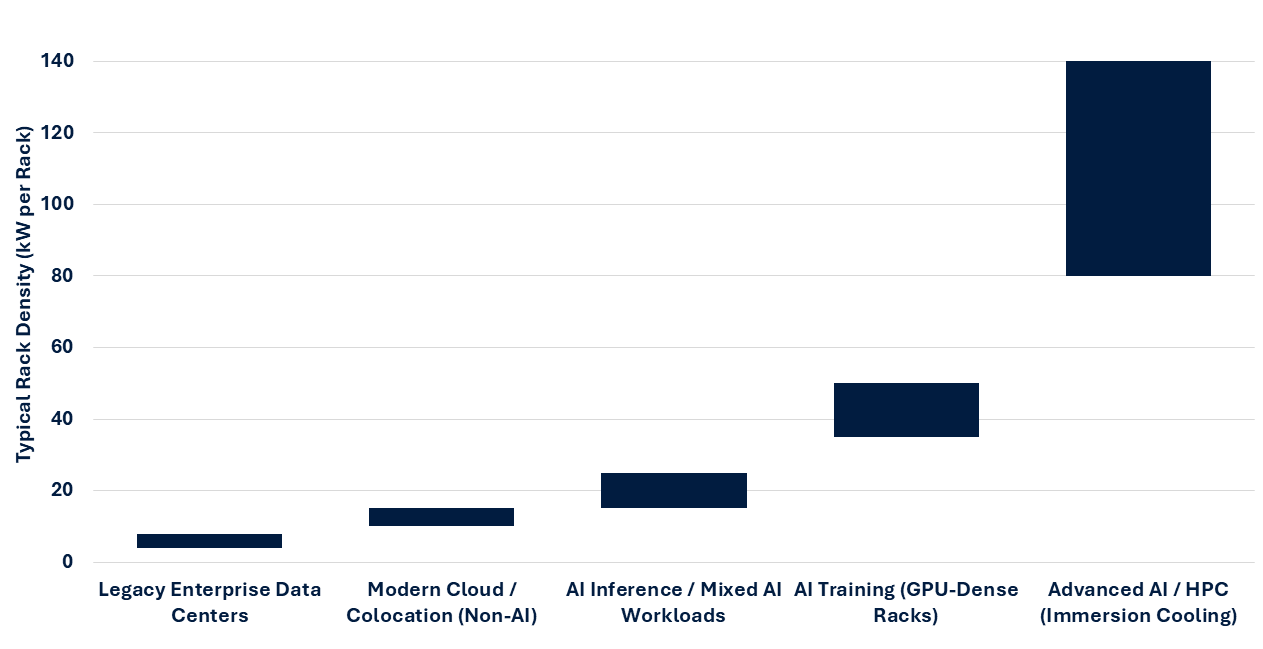

Across 2025–2026, liquid cooling solutions, both direct-to-chip and full immersion, have risen sharply as standard practice for AI-intensive workloads, substantially reducing cooling energy while maintaining high density compute environments. In practical deployments, companies like Microsoft are pioneering “zero-water” cooling systems and community-focused energy strategies, while partnerships for geothermal and hybrid renewable power supply agreements are emerging between data center developers and clean energy producers.

Recently, Southco announced a new “blind mate floating mechanism” designed to improve cooling efficiency in high-density data centers, underscoring broader industry shifts toward advanced thermal management beyond traditional air cooling. Additionally, industry efforts around heat reuse and green financing frameworks signal an ecosystem trend toward measurable carbon and resource footprint reductions. Together, these trends point to a data center ecosystem that is increasingly intelligent, sustainable, and strategically aligned with broader digital and energy infrastructure imperatives.

M&A, Joint Ventures, and Financing: How Capital is Reshaping the Data Center Ecosystem

Data centers have become a prime destination for large-scale infrastructure capital, and 2025–2026 activity increasingly reflects a “platform + power + cooling” thesis where investors and strategics are acquiring capabilities that remove the main bottlenecks to AI-era growth (energy availability, thermal management, speed of deployment).

Two patterns stand out. First, strategic M&A is moving upstream into enabling technologies i.e. not just buying data centers but buying the power-and-cooling stack required to run high-density AI workloads. Second, mega-JVs are emerging as the preferred model to aggregate land, grid access, and development pipelines while keeping balance sheets flexible.

These transactions are not financial engineering instead they are capability upgrades. When Eaton agreed to acquire Boyd’s thermal business for $9.5 Billion, the stated logic was to strengthen Eaton’s end-to-end offering into data centers, especially liquid cooling, positioning it to capture a larger share of the capex wave tied to AI infrastructure.

On the development side, ACS and BlackRock’s GIP launched a €2 Billion JV targeting a large portfolio pipeline, effectively industrializing development and accelerating time-to-market by combining construction/development execution with institutional capital.

Overall, this wave of M&A, joint ventures, and large-scale financing underscores a structural shift in the data center market from a real-estate led asset class to a capital-intensive, infrastructure grade industry where control over power, cooling, and execution capability determines competitive advantage.

Power, Energy, and Grid Constraints: The New Strategic Battleground for Data Centers

AI Workloads Are Driving a Step-Change in Rack Density and Cooling Architecture

Power has become the binding constraint for data center growth often more critical than land, fiber, or capital. With AI-optimized facilities a major driver of incremental load, grid interconnection and transmission expansion are not keeping pace. Proximity to deliverable energy capacity trumps real estate fundamentals across many region.

This constraint is now influencing market rules and operating models. PJM (the largest U.S. grid operator) has proposed a connect and manage approach that would require large new loads to bring supply-side solutions and/or accept curtailment to protect reliability, an explicit signal that data centers are being treated as grid-scale actors rather than passive customers. In Europe, the system-level impact is already visible. For example, Ireland’s data centers accounted for roughly ~22% of national electricity consumption in 2024, sharpening regulatory scrutiny and reinforcing the need for credible power + sustainability strategies.

What this means in practice:

-

-

- Power-first Site Strategy: Prioritize locations with bankable capacity (firm interconnection timelines), not just cheap land or tax incentives.

- Hybrid Energy Procurement: Long-term PPAs plus dispatchable capacity (e.g., firm contracts, onsite generation, or structured load curtailment) to satisfy reliability requirements.

- Grid Collaboration becomes a Competency: Engaging TSOs/ISOs early, supporting transmission upgrades, and adopting faster-approval approaches and forecasting rigor.

- Regulatory and Community License to Operate: Demonstrate transparent impacts on power/water and credible mitigation plans especially in constrained metros.

-

Conclusion: From Real Estate Asset to Strategic Infrastructure Platform

Data centers have decisively transitioned from being a niche real-estate category to mission-critical digital infrastructure, on par with energy, transport, and telecom networks. The convergence of AI-driven compute demand, power and grid constraints, sustainability pressures, and capital inflows is reshaping competitive dynamics across the ecosystem. Winners in this market will not be defined by scale alone, but by their ability to integrate power strategy, technology choices, capital structuring, and stakeholder alignment into a coherent operating model.

Looking ahead, the market is likely to reward players that move early from reactive expansion to intentional platform-building. This requires treating data centers as long-lived infrastructure with multi-decade implications for energy systems, regional development, and digital sovereignty.

Strategic takeaways for stakeholders:

-

-

- Adopt a power-led growth strategy: secure firm, scalable power before committing capital; treat energy as a core input, not an afterthought.

- Design for AI-first economics: future-proof facilities for high-density compute, liquid cooling, and rapid technology refresh cycles.

- Use partnerships as force multipliers: leverage JVs, utility alliances, and ecosystem partnerships to accelerate scale and de-risk execution.

- Embed sustainability and community alignment early: regulatory and social license will increasingly dictate speed-to-market and valuation.

-

In this context, data centers are best understood not merely as buildings with servers, but as strategic convergence points of capital, energy, technology, and policy and those who recognize this shift early will shape the next decade of the digital economy.