The Inflection Point: Why Mining Automation Is No Longer Optional

The global mining industry has entered a structural transformation that moves autonomous equipment from a competitive advantage to an operational necessity. Three converging forces are driving this shift, and none of them are cyclical.

First, the labor equation has fundamentally changed. Mining regions worldwide from Western Australia’s Pilbara to Canada’s oil sands and Chile’s Atacama face chronic shortages of skilled equipment operators. In remote Australian mining districts, fly-in/fly-out logistics and accommodation costs can add upward of A$150,000 per year per employee to operational overhead. Autonomous equipment transforms this cost structure by enabling operations to be managed from remote centers in cities like Perth, where Fortescue, BHP, and Rio Tinto already control drilling rigs and haul trucks from over 1,000 kilometers away.

Second, ESG mandates have moved from reporting exercises to capital allocation decisions. Fortescue’s commitment to eliminate Scope 1 and 2 emissions from its Australian iron ore operations by 2030 backed by a USD 2.8 billion investment in autonomous battery-electric equipment with Liebherr exemplifies how decarbonization targets are now directly driving fleet procurement strategies. Investors and lenders increasingly evaluate mining companies on their technology adoption roadmaps as proxy indicators for long-term operational resilience.

Third, the critical mineral supercycle demands unprecedented extraction efficiency. The global energy transition requires massive increases in copper, lithium, nickel, and rare earth production. Meeting this demand with conventional mining methods is neither economically viable nor operationally feasible at the required scale. Autonomous equipment enables continuous 24/7 operations, eliminates shift-change downtime, and delivers the throughput consistency that conventional manned operations cannot sustain. Mining companies that delay automation risk falling behind not only on cost competitiveness but on their ability to supply the minerals the world urgently needs.

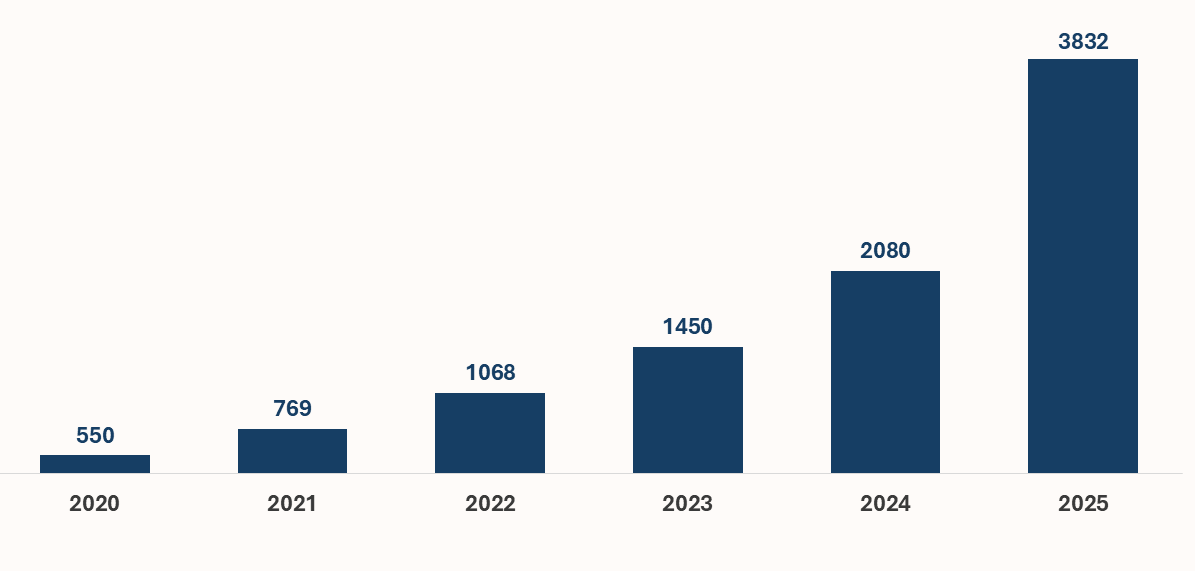

Fleet Deployment by the Numbers: What Mine-Level Data Reveals

Over 3,830 autonomous haul trucks are on surface mines globally as of July 2025. This represents an 84% increase from the 2,080 units tracked in July 2024, and a nearly sevenfold expansion from approximately 550 trucks operating in 2020.

Global Autonomous Haul Truck Fleet

At the operator level, the deployment landscape is concentrated among a handful of large miners. CHN ENERGY Investment Group now operates the world’s largest autonomous fleet with 509 trucks, followed by Guanghui Energy (whose Baishihu Coal Mine alone hosts 420 autonomous units), BHP, and Rio Tinto. Suncor Energy runs 140 autonomous trucks across its Millennium and North Steepbank oil sands mines in Canada, with an additional 47 at Fort Hills. Fortescue currently operates over 200 autonomous trucks across its Pilbara iron ore sites.

The scope of autonomous equipment is broadening beyond haulage. Autonomous blast-hole drilling is the second major equipment category undergoing rapid automation. These systems achieve positioning accuracy within ±5 centimeters of planned locations (compared to approximately ±30 centimeters for conventional manned drilling) and deliver utilization rates of 85–90%, versus 55–65% for manned rigs. BHP signed a deal with Epiroc in early 2025 to deploy Pit Viper autonomous surface drills across its Pilbara operations, remotely controlled from a facility over 1,100 kilometers away in Perth. Fortescue followed with a AUD 350 million order for approximately 50 cable and battery-electric autonomous drill rigs from Epiroc, also remotely operated from Perth, over 1,500 kilometers from the mine face.

Autonomous and autonomous-ready equipment now represents approximately 4.2% of the total global operating population of surface and underground trucks, surface drills, and load-haul-dump machines. Out of nearly 300 mines tracked with autonomous or tele-remote equipment, ten mines account for 30% of the total equipment count, of which seven are in China and three in Australia. In Australia, nearly 10% of haul trucks are already autonomous or autonomous-ready representing the highest penetration rate of any country.

OEM Competitive Landscape: Caterpillar, Komatsu, and the Emerging Challengers

Caterpillar, Komatsu, and Chinese manufacturers Tonly and LGMG collectively account for over 80% of all autonomous truck brands. However, the competitive dynamics are shifting as interoperability, electrification, and vendor-agnostic retrofit solutions redefine the basis of competition.

|

OEM |

AHS Platform | Fleet Size | Material Hauled |

Key Milestone (2024–2025) |

|

Caterpillar |

MineStar Command | ~700 trucks |

12B+ short tons |

Targets 2,000+ by 2030; quarry-class autonomy at Luck Stone (2M tons hauled, zero injuries in Year 1) |

|

Komatsu |

FrontRunner AHS | 900+ trucks |

10B+ metric tons |

First autonomous trolley-electric truck (May 2025); zero system-related injuries across entire fleet |

|

Liebherr |

Co-developed AHS | 360 on order |

In commissioning |

US$2.8B Fortescue deal: 475 battery-electric autonomous machines; largest deal in Liebherr’s 75-year history |

|

Sandvik |

AutoMine | Underground leader |

N/A |

AutoMine Surface Fleet launched (May 2025); acquired Universal Field Robots (Aug 2024) |

|

Epiroc |

6th Sense / ASI | Growing |

N/A |

Largest-ever autonomous + electric contract (Apr 2025); completed full acquisition of ASI Mining (Jul 2024) |

Caterpillar: Scaling From Mines to Quarries

Caterpillar reported approximately 690 autonomous trucks operating under its Cat MineStar Command for hauling platform by end-2024. Company has also announced the ambition to triple that figure to over 2,000 by 2030. The company’s fleet has collectively moved more than 12 billion short tons of material and traveled over 236 million miles. Critically, Caterpillar is expanding autonomy beyond large-scale mines into the quarry and aggregates sector, a substantially larger addressable market by site count. Its deployment at Luck Stone’s Bull Run quarry in Virginia achieved productivity levels matching staffed machines within weeks of go-live in November 2024 and hauled over 2 million tons of material with zero safety injuries in its first year of operation. The economic viability threshold for AHS has dropped from fleets of 70+ trucks to operations with fewer than 15 trucks, dramatically expanding the addressable market.

Komatsu: The Pioneer With the Safety Record

Komatsu’s FrontRunner, launched in 2008, was the world’s first commercially deployed autonomous haulage system. The platform now encompasses more than 900 commissioned trucks globally, having hauled over 10 billion metric tons of material with zero system-related injuries. In May 2025, Komatsu achieved an industry first: the autonomous operation of a power-agnostic electric drive truck connected to a dynamic trolley line, demonstrating the technical convergence of autonomous operation with electrified power delivery. Komatsu’s trucks deliver an average 40% improvement in tire and brake life and a 13% reduction in overall maintenance costs.

The Challenger Field: Liebherr, Sandvik, and Epiroc

Liebherr’s partnership with Fortescue has elevated it from a niche surface equipment manufacturer to a frontline contender in autonomous mining. The USD 2.8 billion deal for 475 autonomous battery-electric machines includes a co-developed AHS with an integrated Energy Management System for coordinating autonomous truck charging cycles. Sandvik, the established leader in underground automation through its AutoMine platform, launched AutoMine Surface Fleet in May 2025, extending its franchise into drill-and-blast surface operations. Epiroc, having completed the full acquisition of ASI Mining in July 2024, now controls one of the industry’s leading OEM-agnostic autonomous mining solutions and secured its largest-ever autonomous and electric equipment contract in April 2025.

Interoperability: The Decisive Battleground

Interoperability has become the critical competitive differentiator as mining operators reject proprietary lock-in. Companies such as SafeAI and Oxbotica are winning contracts by offering vendor-agnostic retrofit solutions for existing fleets, compelling OEM incumbents to publish APIs and participate in cross-OEM working groups. Wenco International’s adoption of open-standards protocols enables mixed-fleet plug-and-play deployment. Heidelberg Materials, one of the world’s largest building materials producers, signed a deal with Silicon Valley-based Pronto AI to deploy autonomous haulage across 100+ trucks at its quarry sites worldwide over three years demonstrating that AHS demand extends well beyond traditional mining into adjacent extractive industries.

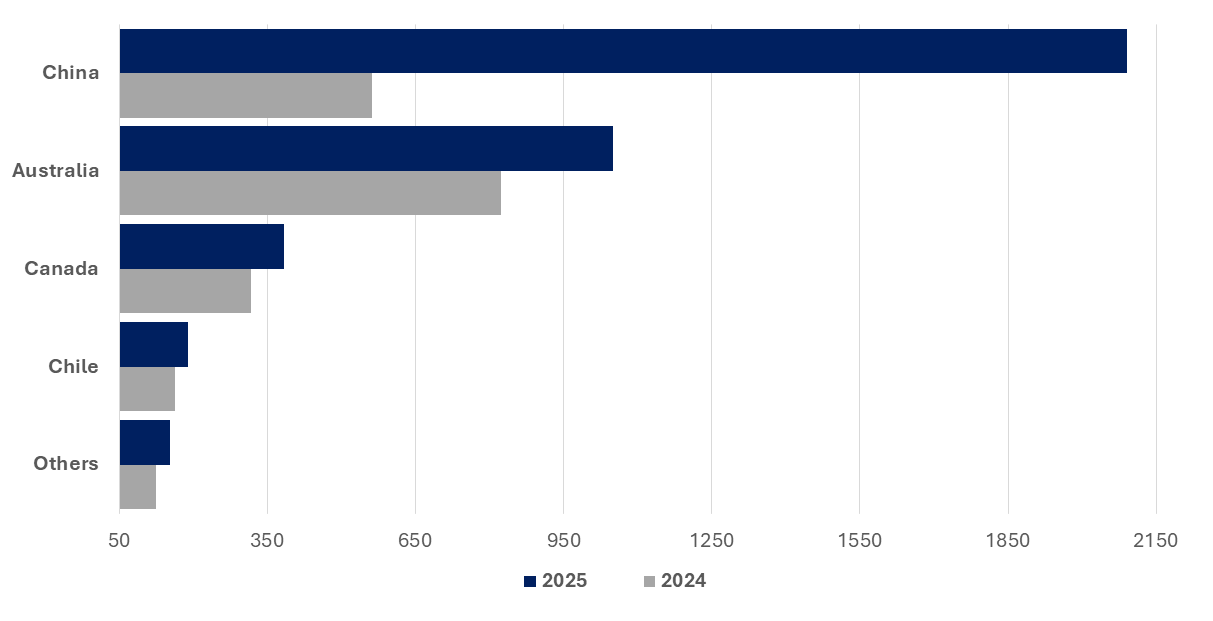

Regional Deployment: China’s Surge, Australia’s Maturity, and the Next Frontiers

The geographic center of gravity for autonomous mining has shifted dramatically. China has emerged as the world’s largest market for autonomous haul trucks, hosting 2,090 units as of July 2025, up from 562 a year earlier and just 69 in May 2022. Chinese coal miners are driving the expansion: the Baishihu Coal Mine (Guanghui Energy) operates 420 autonomous trucks, while the Yimin Coal Mine plans to add another 200 over three years. CHN ENERGY Investment Group leads globally with 509 autonomous trucks in service. Between July 2024 and July 2025, autonomous truck deployments in the global mining sector increased from 2,080 to 3,832 with Chinese operations accounting for the majority of that growth.

Autonomous Truck in Mining by Country

Australia

Australia maintains the second-largest fleet with 1,024 autonomous trucks (up from 927 in 2024) and remains the world’s proving ground for autonomous mining innovation. Rio Tinto pioneered AHS deployment at its Yandicoogina and Nammuldi mines in 2016, and its autonomous fleet has since transported just under five billion tonnes of material across ten Pilbara sites. Rio Tinto is targeting a 10% operational efficiency boost across Pilbara by 2026 through integrated autonomous trucks, autonomous trains, and AI-driven analytics. Fortescue’s USD 2.8 billion Liebherr partnership will replace approximately two-thirds of its current mining fleet with autonomous battery-electric equipment by 2030. Australia’s penetration rate, over 10% of haul trucks autonomous or autonomous-ready, is the highest of any country globally.

North America, Latin America, and Emerging Markets

Canada follows with 344 autonomous trucks, driven by oil sands operators Suncor Energy and Canadian Natural Resources. Nevada Gold Mines’ August 2025 partnership with Komatsu marks the first deployment of FrontRunner AHS in United States, with Sedna and Nokia deploying custom 5G communications infrastructure to support the autonomous fleet. Chile, with 208 trucks, reflects copper-driven adoption at operations like Anglo American’s Quellaveco and BHP’s Escondida. Barrick’s USD 440 million equipment deal with Komatsu for the Reko Diq copper-gold project in Pakistan marks Komatsu’s first major placement in its Middle East territory, signaling the expansion of autonomous mining into new geographic frontiers.

M&A, Joint Ventures, and Strategic Partnerships: The Consolidation Playbook

Mining automation has become a primary arena for strategic M&A, joint ventures, and technology partnerships. The period from 2024 through early 2026 has witnessed an acceleration of deal activity as OEMs, mining operators, technology specialists, and telecommunications providers move to secure positioning in what is increasingly viewed as a winner-take-most market for autonomous ecosystems.

|

Acquirer / Partner |

Target / Partner | Deal Type | Value |

Strategic Rationale |

|

Fortescue |

Liebherr | Partnership |

USD 2.8 Billion |

475 autonomous battery-electric machines (trucks, excavators, dozers) for Pilbara iron ore operations; largest deal in Liebherr’s history |

|

Epiroc |

ASI Mining | Acquisition |

Undisclosed |

Full ownership of OEM-agnostic autonomous mining systems provider; extends surface autonomy capabilities |

|

Sandvik |

Universal Field Robots | Acquisition |

Undisclosed |

Autonomous interoperable solutions for surface and underground mining; strengthens AutoMine platform |

|

Weir Group |

Micromine | Acquisition |

USD 840 Million |

Mining software across exploration, mine design, fleet management; creates end-to-end digital platform |

|

Caterpillar |

Luminar | Partnership |

Undisclosed |

LiDAR integration into Cat Command autonomy platform for next-gen quarry and mining trucks |

|

Barrick / Komatsu |

Reko Diq JV | Equipment Deal |

USD 440 Million |

Primary mining equipment for copper-gold project in Pakistan; Komatsu’s first major Middle East placement |

|

Nevada Gold Mines |

Komatsu + Nokia + Sedna | Multi-Party JV |

Undisclosed |

First U.S. deployment of FrontRunner AHS with custom Nokia 5G communications infrastructure |

|

Hitachi CME |

Rio Tinto | 5-Year R&D Pact |

Undisclosed |

Develop partial autonomy for ultra-large hydraulic excavators; interoperable multi-unit platform by 2030 |

|

BHP |

Epiroc | Fleet Deal |

Undisclosed |

Pit Viper autonomous surface drills across Pilbara iron ore; remotely operated from Perth (1,100+ km) |

|

Fortescue |

Epiroc | Fleet Deal |

AUD 350 Million |

~50 cable and battery-electric autonomous drill rigs for Pilbara; controlled remotely from Perth (1,500+ km) |

|

Heidelberg Materials |

Pronto AI | Partnership |

Undisclosed |

AHS deployment across 100+ trucks at Heidelberg Materials quarry sites worldwide over three years |

The Acquisition Logic: Building End-to-End Autonomy Stacks

OEMs are acquiring technology companies to build vertically integrated autonomy platforms. Epiroc’s completion of the full acquisition of ASI Mining in July 2024 was driven by a clear strategic logic: ASI’s OEM-agnostic autonomous systems enable Epiroc to serve mixed-fleet environments where mines operate equipment from multiple manufacturers. This capability is critical as the industry moves away from single-OEM standardization toward interoperable, multi-brand fleets. Similarly, Sandvik’s August 2024 acquisition of Universal Field Robots widened AutoMine’s ability to integrate with third-party equipment on both surface and underground operations, reinforcing Sandvik’s strategy of positioning AutoMine as an open platform rather than a proprietary system.

The Weir Group’s USD 840 million all-cash acquisition of Australian mining software company Micromine, completed in April 2025, represents a different but equally strategic play. Weir is assembling an end-to-end digital mining platform by combining Micromine’s exploration, mine planning, and fleet management software with its existing MOTION METRICS and NEXT intelligent solutions. The acquisition is projected to enhance Weir’s operating margins by approximately 25 basis points in 2025 and is expected to be EPS-accretive in its first full year of ownership.

The Partnership Model: Co-Development and Risk Sharing

The Fortescue–Liebherr partnership exemplifies a co-development model in which a mining operator and an OEM jointly build proprietary technology that neither could develop alone. Fortescue Zero (the company’s technology arm, rebranded from Williams Advanced Engineering, which Fortescue acquired in 2022) developed the battery power systems, while Liebherr contributed the vehicle platform and manufacturing capability. The jointly developed AHS includes an Energy Management System that coordinates autonomous truck charging, solving a critical operational challenge for battery-electric fleets. Both companies have committed to making their zero-emission mining ecosystem available to the broader industry, signaling an intent to establish a de facto industry standard.

The Nevada Gold Mines deployment represents a different partnership archetype: a multi-party consortium model. The initiative brings together Barrick/Newmont (the mine operators), Komatsu (AHS technology), and Sedna/Nokia (5G communications infrastructure) into a coordinated deployment that marks the first implementation of FrontRunner AHS in United States. This model recognizes that autonomous mining is not a single-vendor solution but requires integrated capabilities spanning equipment, software, and telecommunications.

Strategic Equipment Deals: Locking In Supply Chains

Barrick’s USD 440 million equipment agreement with Komatsu for the Reko Diq copper-gold project in Pakistan (signed June 2025) illustrates how mining companies are using large-scale equipment deals to lock in strategic supply relationships while simultaneously expanding autonomous capabilities into new geographies. Komatsu is establishing Komatsu Pakistan Mining Limited, a dedicated subsidiary for the project shows a level of commitment that goes well beyond a conventional equipment sale. Caterpillar’s partnership with Luminar to integrate LiDAR into its next-generation Cat Command autonomy platform reflects a different supply chain strategy securing access to best-in-class sensor technology from the automotive autonomy sector to accelerate mining-specific autonomous capabilities.

Hitachi Construction Machinery’s five-year R&D partnership with Rio Tinto targets the development of partial autonomy for ultra-large hydraulic excavators, a category that has proven more technically challenging to automate than haulage. The pact envisions an interoperable platform capable of operating multiple excavators with partial autonomy across mine sites by 2030, potentially opening the last major category of surface mining equipment to autonomous operation.

The Convergence Thesis: Electrification, Autonomy, and Data

The most consequential strategic development in mining automation is the convergence of three previously distinct technology trajectories: autonomous operation, fleet electrification, and data-driven mine optimization.

Electrification + Autonomy: The Integrated Value Proposition

Komatsu’s May 2025 milestone, the first-ever autonomous operation of an electric drive truck connected to a dynamic trolley line, demonstrated the technical convergence of driverless operation with on-the-move electric power transfer. Fortescue’s partnership with Liebherr takes this further: all 360 autonomous T 264 trucks will be equipped with Fortescue Zero’s 3.2MWh battery system, with 30-minute fast charging via 6MW robotic chargers and an optional Power Rail (side-mounted trolley) system. Fortescue’s mining fleet consumed approximately 450 million liters of diesel in FY2024, representing 51% of its Scope 1 emissions. The transition to autonomous battery-electric equipment is therefore simultaneously a cost play, a decarbonization strategy, and a productivity lever.

5G and Communications: The Invisible Enabler

Telecommunications infrastructure has emerged as a critical enabler of scaled autonomous operations. Nokia’s custom 5G deployment at Nevada Gold Mines provides the ultra-low-latency, and high-reliability connectivity required for real-time autonomous fleet coordination across large open-pit operations. The partnership model in which telcos, OEMs, and mining operators collaborate on purpose-built communications networks is becoming the template for new autonomous deployments. Without adequate connectivity, autonomous systems cannot scale beyond isolated, geo-fenced circuits to full-site fleet management.

Data as a Compounding Asset

Every autonomous truck, drill, and loader generates continuous data streams that feed AI and analytics platforms for route optimization, predictive maintenance, geological modelling, and production scheduling. This data creates a compounding feedback loop: more autonomous hours generate more data, which generates better models, which generate higher productivity and lower costs. Mining companies that treat their autonomous fleet data as a strategic asset (investing in analytics platforms, data governance, and AI/ML capabilities) will capture disproportionate value from their automation investments. Those that treat data as an incidental byproduct of equipment procurement will leave substantial value on the table.

Strategic Imperatives: What Mining Leaders Should Do Now

For C-suite executives and board-level decision-makers in the mining sector, the transition to autonomous operations demands action across three strategic dimensions.

Assess Autonomous Readiness Beyond Haulage

Most mining companies have evaluated autonomous haulage. Far fewer have systematically assessed readiness across drilling, loading, dozing, ventilation, and processing. The technology frontier is broadening rapidly: Hitachi and Rio Tinto are pursuing autonomous excavation; Sandvik has extended AutoMine to surface drilling; Fortescue is deploying autonomous dozers. Leaders should conduct a mine-lifecycle automation audit that identifies which operational domains offer the highest ROI for the next wave of autonomous deployment, and which require further technology maturation.

Align Technology Partners with Interoperability and Electrification Roadmaps

The autonomous mining OEM landscape is consolidating, and technology partner decisions made in 2026 will shape fleet capabilities through 2035 and beyond. Mining companies should prioritize partners that offer open, interoperable platforms capable of integrating equipment from multiple manufacturers. Simultaneously, electrification roadmaps should be aligned with autonomy deployment. The Fortescue–Liebherr model, in which autonomous operation and battery-electric power are developed as a single integrated system, represents the emerging standard. Companies that procure autonomous-only or electric-only solutions risk costly retrofitting when integrated packages become the market norm.

Invest in Workforce Transformation and Data Governance

Autonomous mining transforms the workforce; it does not eliminate it. Operators become fleet supervisors; drillers become technology managers overseeing multiple autonomous rigs from remote operations centers hundreds or thousands of kilometers away. This transformation requires significant investment in retraining, digital literacy, and change management. Equally, mining companies must build data governance frameworks that treat autonomous fleet data as a core strategic asset, establishing clear policies for data ownership, integration, quality assurance, and AI/ML model governance. Companies that underinvest in people and data will find their autonomous equipment delivers hardware-level returns but fail to capture the compounding analytical value that distinguishes leaders from laggards.

Conclusion: The Window for Strategic Action

Mining automation has passed the point of debate. With nearly 4,000 autonomous haul trucks operating globally, fleet deployments growing at 84% year-over-year, and technology converging across autonomy, electrification, and data analytics, the question for mining leaders is no longer whether to automate. It is how quickly they can build the technical capabilities, workforce competencies, data infrastructure, and strategic partnerships required to compete at the autonomous frontier.

The competitive window is narrowing. Caterpillar intends to triple its autonomous fleet to over 2,000 trucks by 2030. Komatsu has crossed 900 commissioned units with an unblemished safety record. Fortescue is deploying the world’s first large-scale autonomous battery-electric fleet. China’s coal miners have added over 1,500 autonomous trucks in a single year. The miners and OEMs establishing autonomous capabilities today are not merely improving operations — they are defining the operational model for the next generation of resource extraction.

For mining executives, three actions are non-negotiable: audit autonomous readiness across the full mine lifecycle, align technology partner selection with interoperability and electrification roadmaps, and invest in workforce transformation and data governance with the same strategic intensity applied to equipment procurement. The autonomous mine of 2030 will be defined not by the machines it operates, but by the organizational intelligence deployed to orchestrate them.