The Big Picture: Offshore Oil and Gas Equipment Is Back in Demand

For most of the last decade, offshore oil and gas equipment was treated as a structurally challenged business. The 2014 price collapse, the rise of short-cycle North American shale and the early momentum of the energy transition all pushed capital away from long-dated, capital-intensive offshore projects. That narrative has reversed. Offshore and deepwater in particular is once again the segment that operators, contractors and investors are betting on to deliver the next leg of global supply growth.

Conventional fields are declining faster than they once did, and a larger share of remaining barrels now sits offshore, where production decline is steeper and harder to sustain. Sustaining today’s output therefore requires continuous, heavy reinvestment in wells, subsea systems and floating production. If upstream capital spending stopped entirely, the world would lose roughly 5.5 million barrels per day of supply each year broadly equivalent to the combined output of Brazil and Norway. In that context, offshore equipment is not a discretionary purchase but it is the cost of keeping the lights on.

The Capital Cycle Behind the Recovery

The clearest way to understand the equipment market is to follow the capital cycle of its customers. Global upstream investment has run at roughly US$570 billion in 2025 still about a third below its 2015 level in nominal terms, reflecting a decade of capital discipline. Within that envelope, however, the offshore share has staged a marked recovery.

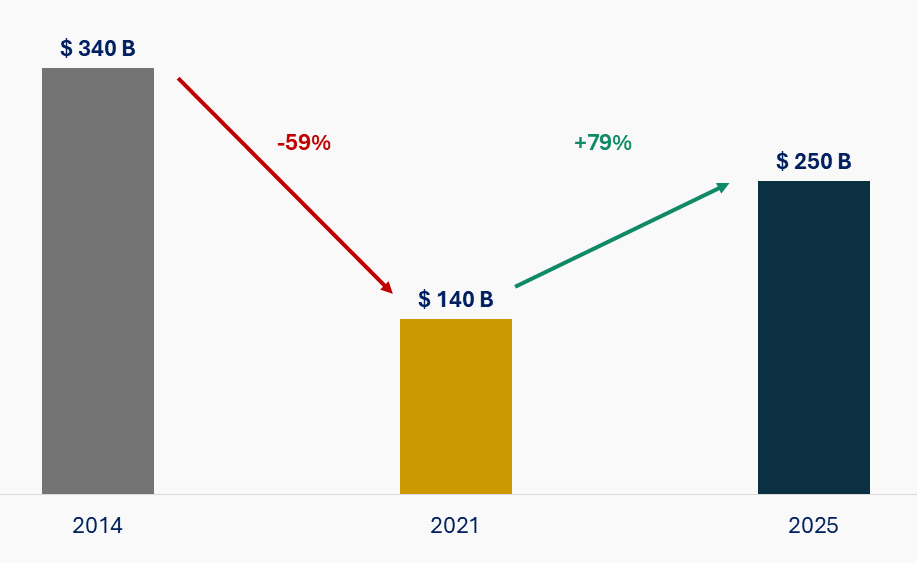

Annual upstream offshore investment fell from around USD 340 billion in 2014 to roughly USD 140 billion at the 2021 trough, before climbing back toward USD 250 billion in 2025. This is the V-shaped recovery that underpins the entire equipment thesis: a near-60% peak-to-trough collapse followed by a near-80% rebound off the bottom.

Upstream offshore investment has rebounded sharply off its 2021 trough, the foundation of the current equipment cycle.

Two structural forces explain why this recovery is more durable than the false starts of the past. First, deepwater has become dramatically more competitive i.e. the average development cost of a new deepwater field has roughly halved over the last decade, from about US$14 to around US$8 per barrel of oil equivalent, as operators standardize designs and re-use proven subsea architectures. Second, sanctioning discipline has improved. The volume of approved greenfield deepwater investment reached close to US$60 billion in a single recent year led by Guyana, Brazil and Norway marked the strongest year for deepwater project sanctions in a decade.

The practical signal for equipment vendors is the contract book. Offshore engineering, procurement and construction awards reached roughly US$46 billion in 2025, translating into a tangible pipeline of around 220 subsea trees, some 2,750 kilometers of subsea umbilicals, risers and flowlines (SURF), 1,700 kilometers of pipeline, more than 90 fixed platforms and over a dozen floating production units. These are the order intakes that convert macro-optimism into manufacturing schedules.

Subsea Systems: The Beating Heart of the Offshore Equipment Market

If offshore is the growth story, subsea is its engine. Subsea production systems such as trees, wellheads, manifolds, controls and the SURF that connects them are where the deepest pools of capital and the sharpest technology competition now sit. Expenditure on subsea facilities is on a roughly 10% compound annual growth path between 2024 and 2027, with total spending expected to exceed USD 42 billion by the end of that period. Deepwater developments alone are likely to account for close to 45% of the subsea market.

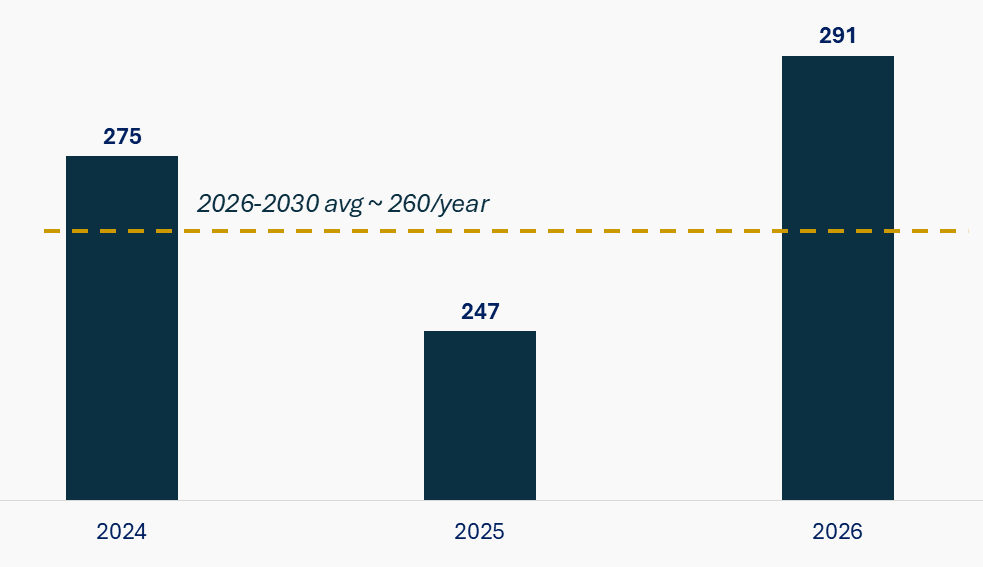

The subsea tree, the valve assembly that controls flow at the wellhead, is the market’s most-watched leading indicator. Tree awards softened to around 247 units in 2025, a roughly 10% decline year-on-year as a handful of mega-projects paused between sanction waves. That dip is widely read as a timing artefact rather than a structural turn. Contracts are forecast to recover to roughly 291 units in 2026, and cumulative visible demand across 2026–2030 is close to 1,290 units, averaging about 260 per year. Strikingly, just two operators, ExxonMobil and Petrobras, are expected to account for around 27% of that demand, concentrated in Guyana’s Stabroek basin and Brazil’s pre-salt.

A soft 2025 for subsea tree awards is expected to give way to a multi-year demand plateau.

When a small number of operators drive a large share of demand and increasingly buy through multi-year frame agreements rather than one-off tenders, the suppliers embedded in those frameworks enjoy unusual visibility and pricing power. Positioning for the right portfolios, early, has become the single most important commercial decision for equipment players.

Rigs and Floating Production: Scarcity Returns to the Drillfloor

On the drilling side, years of fleet attrition, scrapping and a near-total halt to newbuild ordering have produced a structurally tight market for high-specification floating rigs. Leading-edge ultra-deepwater drillships are now commanding day rates that approach or exceed USD 500,000, with the newest high-pressure “20K” assets fetching above USD 600,000. Such levels have not been seen since the previous cycle peak. Premium fleets are running near full utilization, with limited availability through the middle of the decade.

The order book reflects genuine, multi-year commitment from blue-chip operators. Contract and option awards through 2025 spanned Brazil, US Gulf, Norway and Romania, with national and international majors extending programs well into the second half of the decade. Tendering has strengthened across the “Golden Triangle” of North and South America and West Africa, while demand for harsh-environment rigs in Norway is expected to accelerate from late 2026, a signal that the recovery is broadening beyond the warm-water basins.

For equipment and service providers, tight rig supply is a margin tailwind and a scheduling risk in equal measure. It hardens day rates and reinforces operator appetite for solutions that reduce time on the critical path, i.e. faster well construction, pre-engineered hardware and digitally optimized drilling, precisely the areas where differentiated equipment earns a premium.

The Consolidation Wave: M&A, Joint Ventures and the Race for Scale

Perhaps the most consequential development for the equipment landscape is structural rather than cyclical. A sweeping wave of consolidation that is redrawing the competitive map. The strategic logic is consistent where operators increasingly want fewer, larger, fully integrated partners who can take system-level responsibility for a development, and suppliers are reshaping themselves to meet that demand.

1. A New Offshore Services Champion

The agreed merger of Saipem and Subsea7, to be renamed Saipem7, is the headline transaction. Structured as a roughly 50/50 combination, the group would carry combined revenue in the order of €21 billion, a project backlog of around €43 billion, a fleet of more than 60 vessels and operations spanning over 60 countries, with management targeting around €300 million in annual synergies. Approved by shareholders and expected to complete in the second half of 2026, it creates a contractor of unprecedented scale across subsea construction, offshore wind and decommissioning.

2. Equipment Majors Integrate Up and Across

In parallel, the equipment majors are integrating both vertically and across the production life-cycle. The completion of a roughly USD 7.8 billion acquisition of a leading production-chemicals and artificial-lift specialist by a major oilfield-services group, targeting some USD 400 million in annual pre-tax synergies, pushes that group deeper into the less cyclical “production and recovery” space, complementing earlier moves into carbon capture. The same group’s subsea joint venture booked around USD 4 billion of orders in 2025 and is targeting roughly USD 9 billion over the following two years, anticipating a subsea-tree award run-rate some 20% higher in 2026–2027.

These alliances are not merely financial. A landmark global framework under which an integrated subsea alliance won the first award for a deepwater development delivering standardized trees, tubing hangers and a pressure-protection manifold. This illustrates the model operators now prefer early engagement, transparent system-level optimization and repeatable, pre-qualified hardware rather than bespoke engineering for every field.

3. The Integrated, Configure-To-Order Model Wins Share

The clearest proof that integration pays is in the order book of the pure-play subsea integrator. Its subsea backlog stood at roughly USD 15.9 billion entering 2026, having booked around USD 10.1 billion of subsea orders in 2025 and delivered on a three-year goal of more than USD 30 billion in cumulative subsea inbound. Group revenue rose about 9% to USD 9.9 billion with adjusted earnings up roughly a third. More than 80% of that inbound came through integrated EPCI, a decisive shift away from the fragmented, lowest-bid procurement of previous cycle, and a model now being extended into new basins including a deepwater alliance in India.

Scale and integration are compressing the supplier base into a smaller set of system-level partners. For operators, this simplifies delivery but concentrates negotiating leverage for smaller suppliers. It raises the bar to remain relevant. The strategic response, whether to specialize, partner, or position for acquisition, should be decided deliberately.

Technology as the New Competitive Battleground

Across the equipment chain, the differentiators are converging on three themes: standardization, electrification and digitalization. Each aimed squarely at cutting cost, schedule and emissions simultaneously.

-

-

- Standardization: Pre-engineered, configure-to-order subsea systems replace bespoke design with modular building blocks. Reaching a 100th standardized-tree delivery milestone signals that the model has moved from pilot to mainstream, shortening lead times and de-risking execution.

- Electrification: All-electric subsea production systems and subsea-to-shore power are displacing hydraulic actuation and offshore diesel generation, improving reliability and reducing both cost and carbon. Subsea compression is extending the productive life of mature fields by up to 15 years in some North Sea cases deferring costly abandonment.

- Digitalization: Digital twins, AI-assisted drilling and remote operations are compressing time on the critical path and turning installed equipment into a recurring, data-driven services revenue stream rather than a one-off sale.

-

Substantial capital, on the order of hundreds of billions of dollars through 2030, is expected to flow into methane abatement, electrification and carbon capture retrofits on existing offshore assets, while the same subsea engineering skills are increasingly redeployed into carbon storage. For equipment vendors, the energy transition is reframing as an adjacency to be captured, not a threat to be managed.

Where the Capital Is Flowing: Regional Hotspots

-

-

- Brazil: The pre-salt remains a subsea powerhouse, with the national operator’s multi-year frame agreements and a steady cadence of FPSO sanctions anchoring tree and SURF demand for the rest of the decade.

- Guyana & Suriname: The Stabroek basin is the single most important deepwater growth engine, with a long line of FPSO sanctions feeding sustained subsea equipment orders. Recent awards extend an unbroken run of subsea contracts since first development.

- West Africa: Angola, Nigeria and Mozambique are re-emerging, with renewed deepwater exploration commitments and large gas developments reactivating subsea and floating-production demand.

- Norway & the North Sea: Premium-priced harsh-environment work, and life-extension projects sustain a high-value, and technology-intensive market. The rig demand set to tighten further from late 2026.

- The Middle East: Major gas and condensate programs are converting into platform, pipeline and subsea awards, supported by some of the lowest-cost barrels in the world.

- India & Asia-Pacific: Domestic deepwater ambition is rising with multi-billion-dollar operator capital investment for east-coast basins and a new integrated-EPCI alliance specifically targeting future Indian deepwater developments. A notable shift for a market historically dominated by shallow-water and onshore activity.

-

Strategic Implications

Value is concentrating around a smaller number of integrated players, a handful of anchor operators and a defined set of repeatable technologies. We see four priorities for leadership teams across the value chain:

-

-

- For equipment suppliers: Map demand to the operators and basins that actually carry it, and compete for a place in their multi-year frame agreements rather than chasing one-off tenders.

- For operators: Use a smaller, integrated supplier base to lock in schedule certainty and standardized designs, while actively managing the concentration risk that fewer partners create. Build dual-source resilience into long-cycle programs.

- For technology owners: The premium for time and capital efficiency is real and persistent. Prioritize standardization, electrification and digital services that move work off the critical path and create recurring revenue.

- For investors: A capital-intensive, technology-driven industry undergoing consolidation presents significant opportunities for M&A, joint ventures, and targeted market entry. However, success depends heavily on timing investments in line with project sanction cycles and rig-supply dynamics.

-