Executive Summary

Banking-as-a-Service (BaaS) represents a fundamental restructuring of financial services delivery, transitioning from vertically integrated models to open ecosystem architectures. This paradigm enables non-bank entities to embed regulated financial products directly into customer experiences through API-driven connectivity, creating seamless integration of banking functionality. Globally, regulators and platforms are enabling rapid adoption: account ownership and digital payment use have risen materially, and open-API programs in jurisdictions such as the UK and Brazil have generated large transaction volumes and new value pools.

The global BaaS ecosystem is experiencing exponential growth, propelled by shifting consumer expectations, regulatory evolution, and technological advancement. Forward-thinking financial institutions are leveraging BaaS to access new revenue streams and customer segments, while non-bank organizations are deploying embedded finance to enhance customer value propositions and create additional monetization channels.

Success in this evolving landscape requires precision strategy, robust partnership governance, and deliberate organizational transformation. This analysis examines the BaaS ecosystem’s structural dynamics, growth trajectories, and strategic imperatives for financial services leadership.

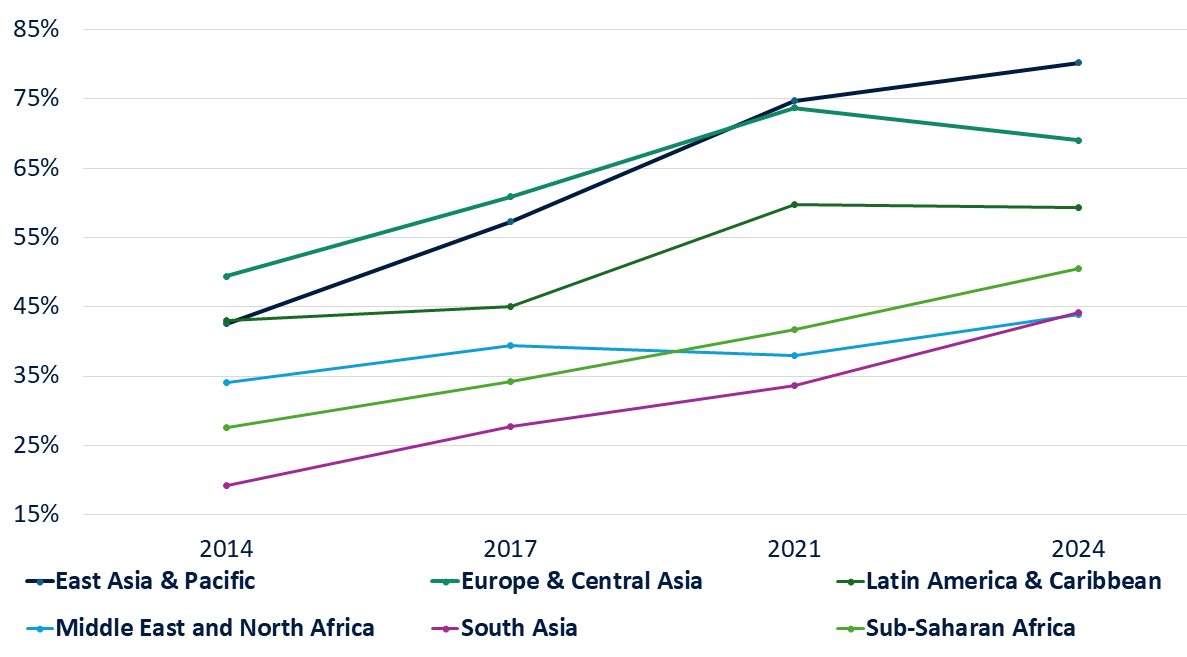

Made or Received a Digital Payment (% age 15+)

Defining Banking-as-a-Service: From Open Banking to Full-Service Platforms

BaaS evolved from regulatory mandates like Europe’s PSD2 and parallels in Brazil (Pix), India (Account Aggregator), and Singapore (Finance-as-a-Service). These frameworks forced data portability, creating fertile ground for platform models. Today BaaS encompasses:

-

-

- Core banking modules (accounts, cards, payments)

- Compliance-as-a-Service (AML, KYC, sanctions screening)

- Lending-as-a-Service (credit decisioning engines, balance-sheet lending)

- Treasury-as-a-Service (liquidity management, FX hedging)

-

BIS notes BaaS partnerships now extend beyond traditional banks to big-tech and super-app ecosystems, redistributing value across the chain.

Banking-as-a-Service Ecosystem Roles and Value Contributions

|

Ecosystem Role |

Primary Value Proposition | Revenue Model |

Strategic Motivation |

|

Licensed Banking Providers |

Regulatory compliance, banking infrastructure, risk management | Fee-based revenue, infrastructure monetization | New revenue streams, customer segment access, ecosystem relevance |

|

Technology Intermediaries |

API integration, technical infrastructure, operational support | Platform fees, transaction-based pricing | Technology monetization, ecosystem orchestration, data insights |

|

Distribution Partners |

Customer relationships, distribution channels, brand trust | Revenue sharing, enhanced customer value, data monetization | Customer retention, additional revenue streams, competitive differentiation |

Why Baas Matters Now: Three Structural Drivers

1. Customer journeys are platform centric.

Consumers and small businesses increasingly expect financial services within non-financial apps (marketplaces, ERP, payroll, retail), which creates a large distribution arbitrage for firms that can embed banking features. As per estimates, the embedded-finance segment in Europe generated nearly €25 billion in 2023 and projects continued rapid expansion.

2. Regulatory enabling via APIs and open finance.

Jurisdictions with mandated open banking / open finance frameworks (UK, Brazil, parts of LATAM and APAC) show higher adoption: Open Banking UK reports growing active use and ~£4.5bn monthly open-banking payments (H1 2023) while Brazil recorded ~4.8 billion successful API calls in June 2023 after central-bank standardization. These implementations lower integration friction and raise trust.

3. Financial inclusion & digital penetration.

The data shows account ownership rising from ~51% (2011) to ~79% (2024/25), reflecting both mobile money and digital accounts as the foundation for embedded delivery and data-driven credit. This trend expands addressable markets, especially in emerging economies.

Regional Strategic Positioning

Europe leads in maturity. PSD3/FIDA (2026 transposition) will expand open finance to insurance, investments, and pensions which will potentially adding over €60 billion incremental revenue by 2030. German/Dutch platforms (Solaris, Treezor, Swan) already serve 200+ brands each.

United States emphasizes volume over margin. CFPB’s Section 1033 rule (2026–2030 phase-in) will standardize data access but regulatory intensity rose. Fed/FDIC/OCC issued multiple consent orders in 2024–2025 against sponsor banks for weak oversight. Successful players (Unit, Synctera, Treasury Prime) differentiate through “orchestration layers” that abstract compliance complexity.

Asia-Pacific favors super-app integration. China’s WeChat Pay/Alipay embed lending at 40–50% lower CAC than standalone apps. India’s ONDC + UPI layer drives 15 billion monthly transactions.

Latin America & Africa focus on inclusion. Brazil’s Pix (200 million users) + open finance Phase 3 (2025) enables embedded credit for 70 million unbanked. World Bank models show 25–30% MSME credit gap closure via platform models.

Implementation Framework and Future Evolution

Successfully navigating the BaaS transition requires deliberate strategic planning, organizational adaptation, and technological investment. Institutions should approach this transformation through a structured framework addressing both immediate opportunities and longer-term evolution.

1. Critical Success Factors

Implementing effective BaaS strategies demands excellence across several dimensions:

-

-

- API Infrastructure: Developing robust, secure, and well-documented APIs is foundational to BaaS participation. These interfaces must balance accessibility with security, providing seamless integration while maintaining regulatory compliance and risk management.

- Partnership Governance: Establishing clear partner selection criteria, risk assessment protocols, and ongoing monitoring frameworks is essential for managing third-party relationships. Appropriate supervisory approaches and AML considerations require continued refinement, particularly following lessons from cases like Wirecard.

- Organizational Alignment: Successful BaaS implementation often requires creating specialized business units with distinct operating models, talent strategies, and performance metrics. These units must balance innovation with risk management, navigating potential cultural tensions with traditional banking operations.

-

2. Future Evolution and Strategic Considerations

The BaaS landscape continues to evolve rapidly, with several emerging trends set to reshape competitive dynamics:

-

-

- AI Integration: Artificial intelligence, particularly agentic AI, promises to further automate financial services delivery and personalize customer experiences. AI adoption could reduce certain banking cost categories by up to 60%, though net savings may be limited to 10 to 20%.

- Regulatory maturation: As BaaS models proliferate, regulatory frameworks continue to evolve. The European Banking Authority and other regulators are developing more sophisticated approaches to overseeing embedded finance and API-based banking relationships.

- Precision Banking: Leading institutions are moving beyond broad segmentation to deliver hyper-personalized financial services at individual customer level. This precision approach requires leveraging data analytics and AI to create tailored propositions for specific customer segments and use cases.

-

Conclusion

Banking-as-a-Service represents a structural transformation of financial services from vertically integrated silos to open, collaborative ecosystems. This shift creates substantial opportunities for institutions that successfully navigate the transition, including new revenue streams, enhanced customer relevance, and improved operational economics.

The future competitive landscape will be defined by precision rather than scale, with specialized capabilities creating sustainable advantage across specific domains. Success requires deliberate strategic choices regarding ecosystem positioning, partnership strategies, and operational models.

Financial institutions must approach BaaS as a fundamental strategic imperative rather than a tactical initiative. This demands leadership commitment, organizational adaptation, and sustained investment in the technological and cultural capabilities necessary to thrive in an increasingly modular financial services ecosystem. The institutions that prosper will be those that embrace collaboration while maintaining distinctive value propositions aligned with evolving customer expectations and market structures.

Explore how BaaS can unlock new revenue pathways for your organization – connect with our strategy team to build your roadmap.