Executive Summary: Power Electronics as the New Performance Backbone

Automotive power electronics has moved from a supporting subsystem to a core enabler of vehicle performance, efficiency, and differentiation particularly in electrified platforms. As OEMs transition toward high-voltage architectures, advanced driver-assistance systems, and software-defined vehicles, power electronics is becoming the decisive bottleneck and opportunity area across the value chain. Silicon carbide (SiC) and gallium nitride (GaN) technologies are accelerating this shift, enabling higher switching frequencies, reduced thermal losses, and compact system designs that materially impact vehicle range and charging performance.

The market for automotive power electronics is driven primarily by inverter and on-board charger demand in battery electric vehicles. At the same time, supply chain vulnerability stemming from semiconductor capacity constraints and dependence on a small set of advanced-material suppliers continues to challenge OEM program timelines and cost targets. For power electronics manufacturers, the strategic imperative is clear: invest in next-generation semiconductor integration, secure resilient upstream partnerships, and deliver system-level efficiency gains that OEMs can translate into tangible customer value.

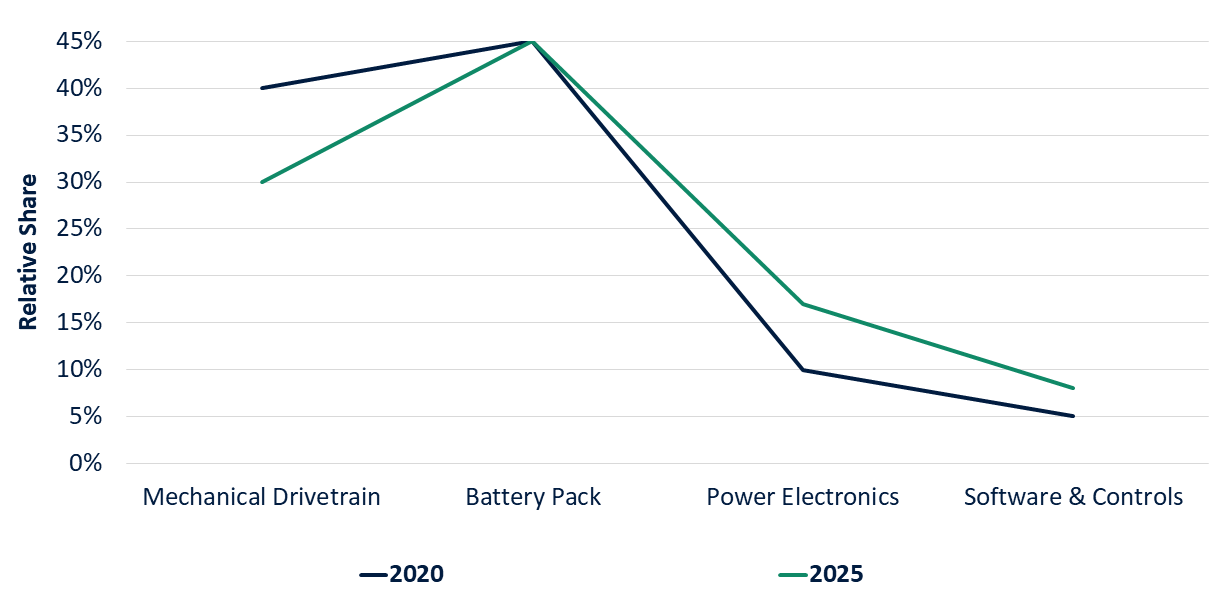

Conceptual Shift in EV Drivetrain Value Pools

Technology Architecture: The Evolving Automotive Power Electronics Stack

In modern vehicles, especially battery electric vehicles (BEVs) and hybrids, the power electronics stack is the central interface that manages energy flow between the battery, electric motor, charging system, and auxiliary loads. This architectural layer encompasses traction inverters, DC-DC converters, on-board chargers (OBCs), and increasingly software-enabled energy management modules that regulate voltage, current, and switching behaviours in real time. These components collectively determine drive efficiency, thermal performance, and system robustness.

Within the broader power electronics domain, the migration toward wide-bandgap (WBG) semiconductors primarily silicon carbide (SiC) and gallium nitride (GaN) is accelerating, underpinned by their superior high-voltage switching, higher thermal conductivity, and reduced conduction losses versus conventional silicon devices. This trend supports higher efficiency at elevated voltages (e. g., 800 V+ architectures) and enables more compact, lighter, and thermally resilient subsystem designs.

At a system level, OEMs are integrating advanced control algorithms, multi-level inverter topologies, and adaptive energy management to optimize performance across duty cycles. This evolution reflects the industry’s shift from discrete component assemblies to highly integrated power modules with embedded diagnostics and software-defined control, which in turn are becoming differentiators for range performance, charging speed, and overall vehicle efficiency.

System-Level Innovations: Inverters, On-Board Chargers, DC-DC Converters, and Thermal Management

Recent product and material advancements are substantially improving the performance, efficiency, and reliability of key power electronics subsystems in electric and hybrid vehicles. OEMs and Tier-1 suppliers are focusing on integration, higher power density, and thermal solutions to meet rising performance benchmarks and tighter packaging constraints:

1. Inverters

Recent industry developments show a shift toward SiC-based inverter platforms, which deliver 3–7 percent higher system efficiency and enable higher switching frequencies, ultimately translating into extended vehicle range and reduced cooling requirements.

OEMs are also adopting more integrated inverter-motor designs, where the inverter is co-packaged with the e-drive. This reduces cabling losses, improves electromagnetic compatibility, and unlocks packaging efficiencies. This approach increasingly visible in next-generation 800-V platforms.

2. On-Board Chargers (OBCs)

OBCs are undergoing rapid evolution as charging expectations rise, with OEMs migrating from traditional 6–7 kW units to 11–22 kW bidirectional architectures supporting vehicle-to-home (V2H) and vehicle-to-grid (V2G) capabilities.

Wide-bandgap semiconductors, especially GaN devices, are enabling significant power-density improvements up to 30% to 40% reduction in size and weight while maintaining high conversion efficiency during both AC charging and energy export.

The industry is also trending toward multi-function “unified power boxes,” combining OBC, DC-DC converter, and power distribution into a single module, thereby reducing system complexity and improving thermal and software control integration.

3. DC-DC Converters

Innovations with wide bandgap (WBG) materials such as GaN promise >97 percent conversion efficiency in next-gen DC-DC converter designs, enabling smaller, lighter modules that support 48 V and high-voltage systems.

4. Unified Power Modules

Suppliers are integrating multiple functions (e.g., inverter + OBC + DC-DC) into unified power modules, reducing size by up to 40% while lowering harness complexity. Thermal potting and advanced cooling materials are being introduced to support higher power density and durability in automotive applications.

5. Domain Controllers as Power-Management Anchors

Automakers are consolidating dozens of distributed ECUs into a handful of domain or zone controllers. As this happens, power management is shifting upward into centralized compute layers.

This creates opportunities for power-electronics OEMs to supply hardware modules with standardized software interfaces that integrate directly into these compute zones. The result is tighter synchronization between propulsion power flows, charging behavior, and thermal strategies.

6. Software-Defined Power Management (SDPM)

Vehicles are becoming software-defined, and power electronics are following. Emerging platforms allow OTA-updatable control algorithms for switching behavior, thermal limits, grid-interaction modes, and charging optimization. This creates an entirely new monetizable layer for suppliers where value shifts from static hardware to upgradable functionality delivered over the vehicle lifecycle.

These innovations underscore a systemic shift toward integrated, high-efficiency, thermally optimized power electronics architectures that align with OEM goals for range, efficiency, and manufacturability.

Strategic Implications for Automotive Power Electronics OEMs

Power-electronics suppliers can no longer compete solely on component performance. The shift toward high-voltage platforms, centralized compute, and wide-bandgap semiconductors demands a more strategic posture.

1. Become System Integrators, Not Component Vendors

OEMs increasingly prefer suppliers capable of delivering pre-validated, thermally optimized, functionally integrated power modules. This reduces development time, minimizes packaging risk, and aligns with the industry push toward consolidated hardware domains.

2. Build Deep Semiconductor Partnerships

With SiC and GaN becoming foundational to next-generation vehicles, long-term collaborations with wafer manufacturers and device suppliers are becoming essential. Co-development of automotive-grade device packaging, thermal designs, and gate-drive strategies provides greater control over performance, cost, and supply continuity.

3. Invest in Embedded Software Competency

As power electronics become software-defined, suppliers must expand into firmware, diagnostics, OTA enablement, and cloud-linked energy-management algorithms. Differentiation will come from the ability to deliver configurable power behavior, not just efficient switching.

Conclusion

The competitive frontier in automotive power electronics is shifting from discrete component capability to integrated, software-driven systems engineered for high voltage, high density, and long-term reliability. Suppliers that embrace this shift will capture more strategic value across the EV ecosystem.

Winners will be those who:

-

-

- Deliver highly integrated power modules that compress vehicle complexity.

- Establish long-term semiconductor and materials partnerships to secure next-gen technology supply.

- Build scalable software frameworks that enable OTA updates, adaptive control, and grid-connected functionality.

- Engineer hardware and software together as a unified platform rather than separate disciplines.

-

The future power-electronics landscape will favor suppliers who operate as true system partners offering OEMs faster integration, higher performance, and continuous upgradability across the vehicle lifecycle.