Cross-border M&A is back on the CEO agenda but it is no longer “just” a valuation and synergy exercise. In today’s environment, deal success is increasingly determined by a different set of constraints: economic-security regulation, foreign investment screening, foreign subsidies scrutiny, shifting tariff regimes, and a materially higher probability that politics will intervene mid-process.

The result is a new deal reality: winners are not only the best price-makers; they are the best risk-underwriters. They build regulatory strategy into the investment thesis, design optionality into structure and financing, and manage stakeholder narratives as rigorously as they manage diligence.

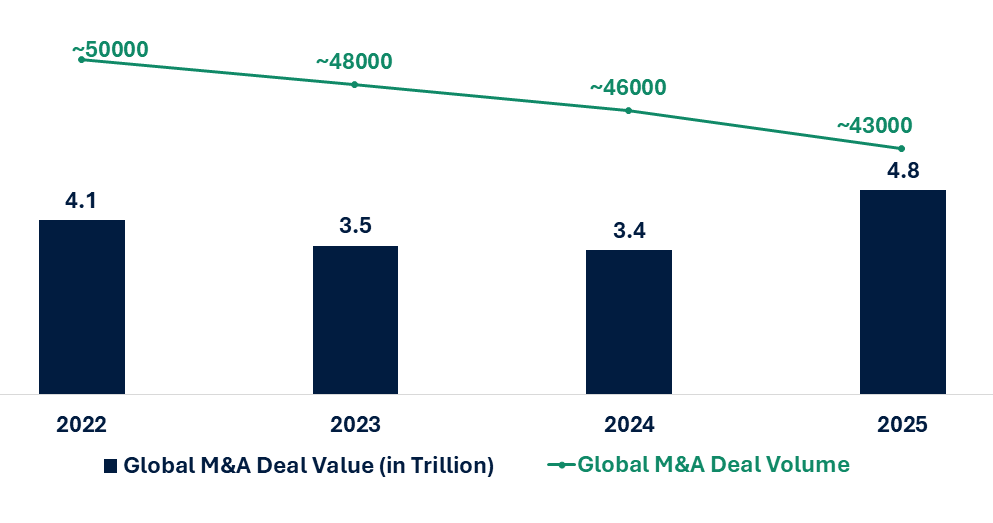

Global M&A Deal Value and Volume (2022-2025)

The Next Phase of Cross-Border M&A: Volume Recovery Meets Strategic Friction

By late 2025, M&A value and mega-deal momentum strengthened, including a meaningful pickup in cross-border activity. Global dealmaking value above $4.8 trillion in 2025, with cross-border deals up 45% to ~$1.25 trillion.

At the same time, the composition of deal flow reflects volatility:

-

-

- Deal values have been more resilient than deal counts, indicating a barbell market where large, strategic deals clear while mid-market activity remains more rate- and risk-sensitive.

- Infrastructure-adjacent and AI-driven assets are drawing cross-border capital at speed. For example, data-center dealmaking in 2025 surpassed 100 transactions totaling nearly $61 billion through November.

-

The Rise of Regulation as a Primary Deal-Shaping Force

1. Foreign investment screening is now a mainstream constraint

Foreign investment review is no longer limited to defense primes and semiconductors. Economic security framing has widened the aperture to include data, critical infrastructure, advanced manufacturing, healthcare supply chains, and dual-use technologies.

Europe: The EU’s coordination mechanism continues to scale. The European Commission reported 477 investments notified under the EU FDI screening cooperation mechanism in 2024, with most cases closed quickly and a smaller subset moving to deeper assessment.

United States: CFIUS remains a central gating item for many inbound (and certain non-controlling) transactions. The U.S. Treasury’s CFIUS Annual Report for CY 2024 provides official filing and process visibility.

What is structurally different now

-

-

- Reviews are more multi-agency and more “whole-of-government,” increasing the number of stakeholders who can effectively delay outcomes.

- Mitigation is more common and more operational (e.g., governance restrictions, data localization/segregation, supply assurances), meaning it can alter the synergy case and post-close operating model.

-

2. The EU Foreign Subsidies Regulation is changing timelines and information burdens

The EU Foreign Subsidies Regulation (FSR) introduced a new, standstill-notification regime for certain M&A transactions creating an additional regulatory lane beyond classic merger control.

Multiple trackers indicate that filings have been substantial, exceeding early expectations. For example, by mid-2025 there had been well over a hundred M&A-related notifications, reinforcing that FSR is operationally material for cross-border deals involving non-EU financial contributions. For technical grounding, the European Commission’s own FSR Q&A provides clarity on notification concepts and threshold mechanics.

If your group has meaningful non-EU financial contributions, FSR analysis must start early because the data-collection burden can become the critical-path item.

Trade Fragmentation as a Direct Driver of Valuation and Deal Structure

Volatility is increasingly transmitted through trade policy: tariffs, export controls, sanctions, industrial policy, and shifting rules of origin. The WTO’s trade monitoring has recorded a high volume of measures and ongoing policy churn, reflecting elevated policy activism.

The IMF has repeatedly highlighted geo-economics fragmentation as a downside risk to trade, investment, and growth, with potential macro costs that range widely by scenario and adjustment capacity.

Practical deal impacts

-

-

- Cost structure volatility: Tariffs and export controls can reprice a target’s input economics and customer competitiveness within a single policy cycle.

- Stranded synergies: Synergies tied to cross-border sourcing, data flows, or technology transfer can be impaired or prohibited post-signing.

- Carve-out premiums/discounts: Businesses with “clean” geographic footprints and localized supply chains can command a premium because they are easier to clear and operate.

-

A Modern Cross-Border Deal Thesis: Three Risk Layers

A robust cross-border investment thesis now needs to explicitly quantify three layers of risk and the mitigations available.

Layer 1: Regulatory clearance risk (probability and time-to-clear)

-

-

- Identify all relevant regimes: merger control, FDI screening, sector regulators, FSR (EU), and (where relevant) export controls/data governance.

- Model timeline scenarios, not just a single “expected close.” A “slow-clear” case can destroy IRR even if the multiple is attractive.

-

Layer 2: Operability risk (what you can actually do after close)

-

-

- Can you integrate data, technology, and key functions across borders?

- Will mitigation conditions require stand-alone governance, ring-fencing, or restricted information flows?

- Does the synergy case rely on items that may become sensitive (AI models, customer data, semicon IP, pharma/medtech supply)?

-

Layer 3: Tradability risk (how policy changes reprice the business)

-

-

- Sensitivity-test margins and revenue exposure to tariff changes, licensing requirements, and sanctions risk.

- Assess supplier concentration and chokepoints for critical inputs.

-

How Leading Executives Are Rewriting Cross-Border Deal Strategy

1. Start with a regulatory thesis, not a legal checklist

High-performing acquirers define a proactive “regulatory thesis” early:

-

-

- Why the transaction is pro-competitive / pro-security-of-supply

- Where commitments are acceptable vs value-destructive

- What remedies are feasible without breaking the operating model

-

This is increasingly important in jurisdictions where economic security narratives influence outcomes.

2. Design optionality into structure

In volatile cross-border environments, structure is a strategic instrument:

-

-

- Staged acquisitions / call options to reduce upfront exposure and allow learning.

- Joint ventures where control and governance can be engineered to reduce screening friction.

- Ring-fenced entities or “clean teams” that allow diligence and integration planning without triggering early regulatory concerns.

- Carve-outs where sensitive assets (or geographies) are excluded to improve clearability.

-

3. Re-architect diligence from “financial and legal” to “operational sovereignty”

Traditional diligence misses the real failure modes. Modern diligence must include:

-

-

- Data mapping (where data resides, where it flows, who can access it)

- Technology classification (dual-use exposure; export-control adjacency)

- Supply chain stress testing (single-source risks; policy chokepoints)

- Customer concentration under sanctions/tariff scenarios

-

4. Rebase the valuation model to include regulatory economics

Executives increasingly embed:

-

-

- A clearance probability adjustment (expected value approach)

- A time-to-close distribution (impact on financing costs and IRR)

- A mitigation cost range (capex/opex of ring-fencing, compliance systems, governance)

-

This is how top teams avoid paper synergies that never become realizable cash flow.

Closing Perspective

Cross-border M&A has returned to the strategic agenda, but under a fundamentally different operating reality. Regulatory scrutiny, trade fragmentation, and economic-security considerations now determine not only whether a deal can close, but whether value can ultimately be realized.

For CEOs and boards, the critical question has shifted from deal feasibility to post-close operability. Transactions that do not account for regulatory conditions, integration constraints, and policy volatility upfront increasingly suffer from delayed timelines, impaired synergies, and suboptimal capital outcomes.

Leading acquirers are responding by embedding regulatory and trade considerations directly into deal design i.e. structuring ownership, governance, and integration with clear-eyed realism. In a volatile global environment, cross-border M&A will continue to create value, but only for organizations that treat discipline, not momentum, as the primary source of advantage.