Executive Summary

In an era defined by exponential data growth and AI-driven workloads, Power Distribution Units (PDUs) have evolved from mere power strips to critical enablers of operational efficiency, risk mitigation, and sustainability in data centers. As global data center energy demands are projected to double by 2030 due to AI proliferation, investing in advanced PDUs particularly intelligent variants offers substantial returns through energy optimization, reduced downtime, and enhanced scalability.

PDUs serve as the backbone of electrical power delivery in modern data centers, distributing utility or uninterruptible power supply (UPS) feeds to racks of servers, networking equipment, and storage systems. Unlike consumer-grade power strips, PDUs are engineered for high-density environments, offering robust surge protection, circuit breakers, and compatibility with single-phase or three-phase inputs. They form the final link in the data center power chain from utility transformers to UPS systems, floor-mounted PDUs, and ultimately rack-mounted units that connect directly to IT loads.

With the rise of hyperscale and edge computing, PDUs must handle increasing rack densities, often exceeding 50 kW per rack in AI-optimized facilities, demanding features like hot-swappable modules and multi-output transformers for flexibility.

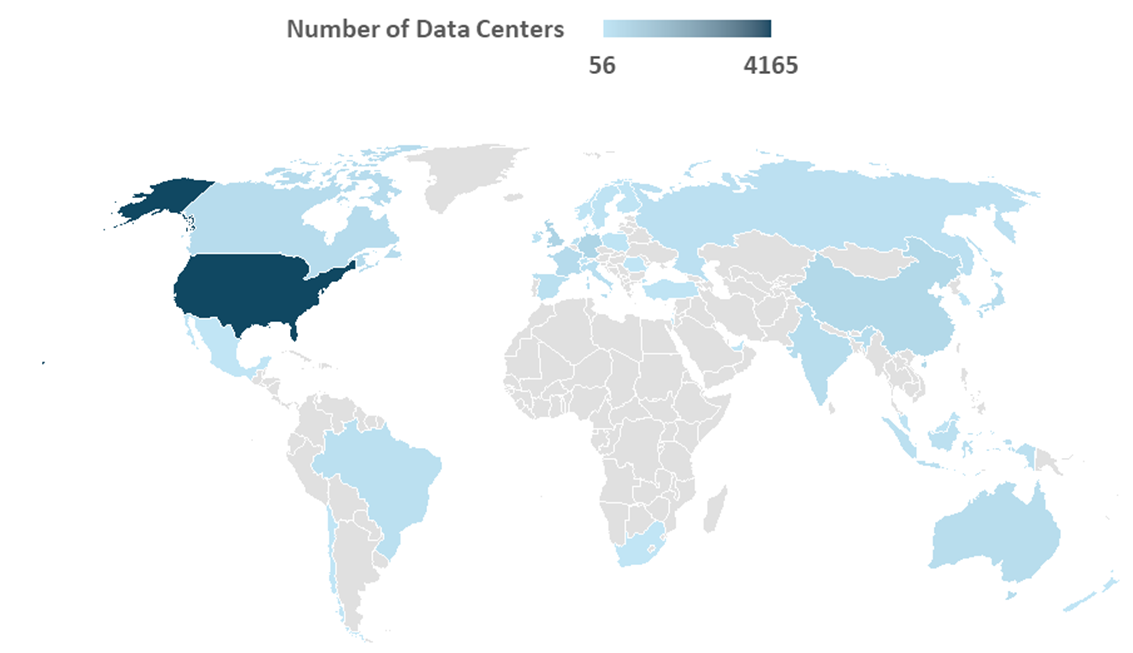

Data Centers across the Globe

Technological and Architectural Trends: Rack Densities, Intelligent and Modular PDUs

PDUs are rapidly transforming to meet the demands of AI-intensive data centers, where rack power densities are surging and traditional air cooling is reaching its limits. AI workloads, powered by advanced GPUs like Nvidia’s Blackwell series, are pushing average rack densities from 15-40 kW in legacy setups to 100-140 kW in new deployments, with some hyperscale AI clusters exceeding 200 kW per rack. This shift is driving global data center electricity demand higher, with projections indicating a 50-165% increase by 2030 compared to 2023 levels, largely attributable to AI accelerated servers.

Intelligent PDUs are becoming essential, featuring per-outlet monitoring, remote switching, and integrated sensors for real-time power and environmental management. The intelligent PDU market is forecasted to grow at a CAGR of 8-9% through 2032, reflecting widespread adoption for predictive analytics and efficiency gains. Concurrently, liquid cooling has emerged as the standard for high-density racks, with adoption rates projected to reach nearly 50% in server racks, enabling PUE improvements to 1.1-1.2 and supporting sustainable operations amid rising regulatory pressures.

Key trends shaping PDU architecture include:

-

-

- Modular and high-capacity designs: Hot-swappable modules and three-phase inputs for seamless upgrades in dynamic AI environments.

- Hybrid cooling integration: PDUs with sensors monitoring coolant flow alongside power metrics in direct-to-chip or immersion systems.

- Sustainability features: Dynamic load shifting and heat reuse to align with ESG goals, as data centers face grid constraints and escalating energy costs.

-

These advancements position advanced PDUs as critical for resilience, with operators prioritizing them to achieve rapid ROI through 10-20% energy savings and minimized downtime in an increasingly power-constrained landscape.

Supply Chain Dynamics and Geopolitical Influences in the PDU Market

The PDU supply chain remains a complex, globally integrated network heavily reliant on raw materials like copper and aluminum, electronic components such as semiconductors and circuit boards, and assembly hubs predominantly in Asia-Pacific, where China and Taiwan account for over 60% of production.

Major vendors including Schneider Electric, Eaton, and Vertiv navigate this ecosystem amid persistent bottlenecks in transformers and high-voltage cables, exacerbated by surging demand from AI-driven data centers. However, supply chain disruptions have intensified, with over 55% of North American firms reporting shortages in semiconductors and microcontrollers, leading to extended lead times of 12-18 months for critical components and hindering timely deployments in hyperscale facilities.

Geopolitical tensions have profoundly reshaped the PDU supply chain, introducing volatility through trade wars, conflicts, and regulatory shifts. In 2025-2026, escalating US-China trade disputes imposed tariffs that inflated production costs by 10-20%, while export controls on semiconductors disrupted intelligent PDU manufacturing, critical for AI workloads.

A recent example of proactive supply chain adaptation in the PDU sector is Taiwan-based Powertech Industrial Co., which in July 2025 accelerated its diversification by redirecting over 60% of its procurement budget to Vietnamese suppliers to mitigate risks from escalating US-China trade tensions and tariff uncertainties. This move supported the near-certification and expanded production of its high-end PDUs for data center and edge AI applications, contributing to an optimistic operational outlook into 2026.

These dynamics underscore the need for resilience strategies such as diversified sourcing to mitigate costs and ensure continuity. As geopolitical risks evolve into a “new era” of multipolar threats, PDU manufacturers are investing in modular designs and local assembly to buffer against disruptions, potentially reducing TCO by 15-20% for end-users.

Strategic Initiatives by PDU OEMs: Recent Activities and Implications

In the year 2025, PDU original equipment manufacturers (OEMs) pursued targeted mergers and acquisitions (M&A) and joint ventures (JVs) to bolster their capabilities in high-density data center power management, driven by AI-driven demand surges. A key example is Eaton’s agreement to acquire Resilient Power Systems in July 2025, a move aimed at enhancing its modular power solutions for data centers. This acquisition strengthens Eaton’s portfolio in resilient, scalable PDUs, addressing the growing need for uninterrupted power in hyperscale environments.

Similarly, in November 2025, Eaton signed an agreement to acquire Boyd Thermal for $9.5 billion, expanding its thermal management capabilities that complement PDU systems in liquid-cooled environments, addressing overheating challenges in high-power racks. Vertiv, another key player, announced its acquisition of a custom rack solutions manufacturer in July 2025, bolstering its high-density infrastructure offerings, including integrated PDUs for AI-optimized racks.

The implications of such activities are profound for 2026 and beyond, positioning PDU OEMs to mitigate supply chain risks, and accelerate innovation amid escalating data center power needs. By acquiring specialized firms and forming JVs, companies are enhancing ROI through synergies like 10-15% efficiency gains in power distribution.

Conclusion

Power Distribution Units are no longer peripheral components within the data center stack; they are becoming strategic control points for power reliability, utilization, and governance. As rack architecture evolve, power availability tightens, and outage tolerance declines, the value of a PDU is increasingly measured by its ability to deliver predictable performance under stress, credible data for decision-making, and faster recovery when failures occur. In this context, incremental feature enhancements are insufficient. What matters is engineering rigor, measurement integrity, and alignment with system-level power architectures.

For PDU OEMs, this shift presents a clear strategic choice. Those that continue to compete on hardware commoditization will face margin pressure and diminishing differentiation. Those that position PDUs as power integrity platforms anchored in defensible data, operational transparency, and future-ready design will secure deeper relevance in customer infrastructure decisions and more durable competitive advantage in an increasingly power-constrained world.