How Algorithmic Trading Works and Common Types of Algorithmic Trading Strategies

Algorithmic trading operationalizes an investment thesis into an end-to-end execution workflow: ingest market data, translate it into signals, apply risk checks, and route orders with minimal latency and strict traceability. In practice, this runs as an event-driven pipeline where market data feeds (price/volume/order book), signal engines (rules- or model-based), and execution engines (smart order routing, slicing, and venue logic) interact continuously.

Algorithmic trading strategies can be broadly grouped into alpha-generation strategies and execution-focused strategies, each serving a distinct role in the investment lifecycle. Alpha strategies aim to identify repeatable market inefficiencies using price trends, statistical relationships, or event-based triggers, while execution algorithms focus on minimizing transaction costs, market impact, and slippage for large or frequent orders. In recent years, institutional emphasis has shifted toward risk-adjusted, capacity-aware strategies, reflecting tighter regulations, higher volatility regimes, and increased scrutiny on market stability.

From a practitioner’s standpoint, the most widely deployed strategy categories include:

-

-

- Trend-following and momentum strategies, which capitalize on sustained price movements using technical indicators or predictive signals.

- Mean reversion and statistical arbitrage, exploiting temporary deviations from historical correlations between securities.

- Arbitrage strategies, targeting price mismatches across instruments, venues, or timeframes, often requiring low-latency infrastructure.

- Market making and liquidity provision, earning bid–ask spreads while actively managing inventory and adverse selection risk.

- Execution algorithms such as VWAP, TWAP, and POV, designed not to outperform the market but to efficiently access it, which now account for a significant share of institutional trading volumes globally.

-

Together, these strategies form the backbone of modern electronic markets, where competitive advantage increasingly lies not just in signal quality, but in robust risk controls, execution discipline, and regulatory alignment.

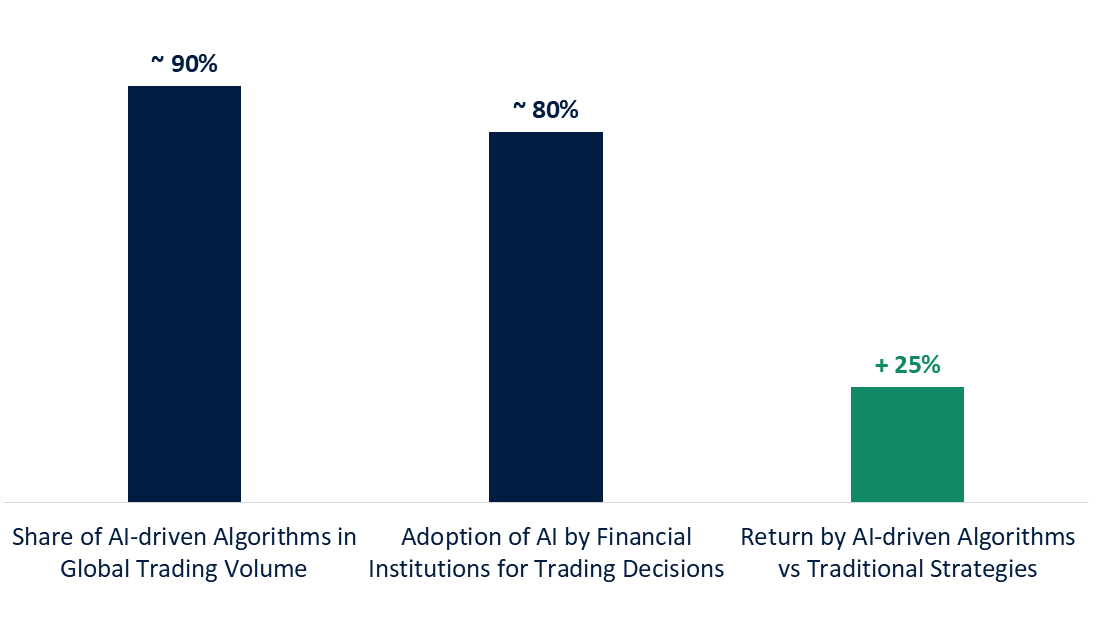

AI-driven Algorithm Trading

How Regulators Are Shaping the Future of Algorithmic Trading

Across major financial markets, regulatory authorities have been responding to the rapid growth of algorithmic trading by strengthening oversight frameworks, promoting transparency, and balancing innovation with market integrity. In the United States, algorithmic strategies are regulated within the broader securities regulatory regime, where the Securities and Exchange Commission (SEC) and the Financial Industry Regulatory Authority (FINRA) require firms engaging in algorithmic trading to adhere to supervision, risk controls, and audit standards. These bodies monitor compliance with trading rules, risk management procedures, and surveillance systems to mitigate systemic and conduct risks arising from high-speed automated strategies.

In Europe, algorithmic and high-frequency trading fall under the regulatory ambit of MiFID II (Markets in Financial Instruments Directive II) and related technical standards, with the European Securities and Markets Authority (ESMA) actively coordinating supervisory priorities among national regulators. ESMA and affiliated forums have placed algorithmic trading top of their agenda, reflecting ongoing focus on market abuse prevention, system stability, and cross-border coordination among financial and energy regulators.

Emerging markets like India are advancing comprehensive regulatory frameworks to govern both institutional and retail participation in algorithmic trading. The Securities and Exchange Board of India (SEBI) has introduced a new regulatory regime specifically aimed at “safer participation of retail investors,” mandating that brokers obtain exchange approval for each algorithm, tag orders with unique identifiers for audit trails, and ensure algo providers are empanelled and compliant before deployment. This framework reflects a clear regulatory priority to enhance transparency and investor protection as retail automation grows.

These regulatory developments illustrate a broader global trend: jurisdictions are transitioning from foundational rules conceived in earlier decades toward dynamic, technology-aware governance that accounts for innovations such as algorithmic execution, API-driven retail access, and increasingly sophisticated automated strategies, all while seeking to preserve market fairness, stability, and investor confidence.

Competitive Landscape and Strategic Positioning in Algorithmic Trading

The competitive landscape is anchored by both proprietary trading firms and platform providers, with established market makers and technology firms driving innovation and infrastructure enhancements. Key global players such as Citadel Securities, Virtu Financial, Jane Street, Flow Traders, GTS Securities, Optiver, and IMC Trading continue to dominate institutional algorithmic execution and liquidity provision, leveraging proprietary quantitative models and ultra-low-latency systems to sustain competitive advantages.

Meanwhile, platform providers like QuantConnect and marketplace ecosystems typified by Tradetron are expanding access and community-driven strategy deployment, enabling both institutional quants and sophisticated retail participants to design, backtest, and execute automated strategies at scale.

Recent initiatives, partnerships, and ecosystem developments also illustrate dynamic competitive shifts:

-

-

- Exchange empanelment and technology recognition — The National Stock Exchange in India recently authorized Tradetron as an algorithmic trading technology provider, enhancing systematic trading access and reflecting a maturing market infrastructure.

- Middleware and execution partnerships — Global Fintech platforms and execution vendors regularly collaborate to extend algorithmic capabilities to institutional and digital asset clients, exemplified by partnerships reported in financial technology coverage.

- Product and platform evolution — Across the industry, best-in-class algorithmic trading platforms are integrating advanced order management systems, built-in execution tactics (VWAP/TWAP), and AI analytics to meet complex strategy and compliance needs, reshaping competitive positioning in both institutional and retail segments.

-

Overall, competitive differentiation increasingly centers on technology depth, regulatory compliance alignment, cross-asset execution breadth, and the ability to serve a widening spectrum of users from hedge funds and prop desks to quant developers and algorithmic retail traders.

Risk Management and Governance in Algorithmic Trading

As algorithmic trading scales across asset classes and participant types, risk management and governance have become critical. Industry estimates suggest that algorithmic and high-frequency strategies now account for well over 60–70% of trading volumes in major equity markets, materially increasing the potential for technology-driven, rapid-loss scenarios if controls fail. Regulators globally have therefore converged on a clear principle: firms deploying algorithms must demonstrate ex-ante risk controls, real-time supervision, and post-trade accountability, ensuring that speed and automation do not undermine market stability or investor protection.

From an institutional perspective, governance frameworks are increasingly designed around the concept of “human accountability over machine decisions.” This includes formal model approval committees, documented testing and stress scenarios, and clearly defined ownership between trading, technology, and compliance teams. Recent regulatory reviews in the UK, EU, and Asia have consistently highlighted that failures tend to arise not from strategy logic alone, but from weak change management, insufficient kill-switch readiness, and inadequate monitoring during abnormal market conditions.

An advanced algorithmic trading risk and governance framework integrates robust controls, real-time oversight, and adaptive technologies to mitigate market, operational, and systemic risks, ensuring compliance with regulations like those from the FCA and MiFID II while leveraging AI for predictive analytics.

It emphasizes pre-trade validations to prevent erroneous orders, post-trade analysis for anomaly detection, and governance structures that embed accountability across development, deployment, and monitoring phases, ultimately reducing potential losses by up to 50% through proactive measures as seen in quantitative hedge funds.

-

-

- Pre-Trade Risk Controls and Testing: Incorporate automated checks for order limits, price collars, and velocity logic to validate trades before execution, with rigorous development and backtesting protocols that align with FCA guidelines, minimizing flash crash risks by ensuring algorithms are stress-tested against historical data scenarios.

-

-

-

- Real-Time Monitoring and AI Integration: Utilize dashboards and machine learning algorithms for continuous surveillance, detecting subtle patterns and adapting to market volatility in milliseconds, as advanced systems can identify anomalies that human oversight might miss, enhancing response times and compliance.

- Governance and Compliance Structures: Establish independent risk committees, regular audits, and clear policies for algorithmic ownership and updates, integrating risk considerations into core investment strategies to foster accountability and regulatory adherence, with frameworks like those in RTS6 promoting segregation of duties to prevent unauthorized activities.

- Post-Trade Analysis and Mitigation: Implement tools for ongoing risk assessment, including kill switches and incident reporting, to monitor performance and refine strategies, supported by technological safeguards that have proven effective in reducing operational risks in high-frequency trading environments.

-

Conclusion

Algorithmic trading has evolved from a niche institutional capability into a core pillar of modern market structure, reshaping how liquidity is provided, risk is managed, and capital is deployed across global financial markets. The true differentiator is no longer speed or automation alone, but the ability to integrate robust strategy design, regulatory alignment, resilient technology, and disciplined governance into a coherent operating model. Markets where algorithmic participation is highest are also those where expectations around transparency, control, and accountability are most stringent signaling a structural shift rather than a cyclical trend.

As regulators tighten oversight and competition intensifies, sustainable advantage will increasingly depend on explainable models, adaptive risk frameworks, and scalable infrastructure that can withstand market stress while meeting supervisory expectations. In this environment, algorithmic trading is best viewed not as a race for marginal speed gains, but as a long-term exercise in institutional maturity, operational excellence, and trust.