FBO Industry

The global expansion of business aviation has quietly created a specialized layer of aviation infrastructure: the Fixed-Base Operator (FBO). In simple terms, an FBO is a commercial enterprise authorized by an airport to provide aviation services such as fueling, hangaring, maintenance, and passenger handling to private, corporate, and general aviation aircraft. Unlike airline terminals designed for scheduled passenger traffic, FBOs primarily support non-scheduled aviation activities including business jets, charter operations, and private aircraft movements.

Operationally, FBOs function as the ground infrastructure backbone of private aviation, enabling aircraft operators to refuel, park, service, and prepare aircraft efficiently while providing premium facilities for passengers and crew. Services typically extend beyond aircraft support to include concierge assistance, crew lounges, flight planning, and luxury passenger terminals which makes FBOs the private-aviation equivalent of airport terminals. As business aviation continues to expand globally, FBOs are evolving from simple fuel providers into integrated service platforms for private aviation operations.

Broad Categories of FBO Models

While service offerings vary across airports and markets, FBOs typically fall into three operational categories:

-

-

- Full-service FBOs – Provide comprehensive aviation services including fueling, hangaring, maintenance, passenger lounges, and concierge facilities.

- Fuel-focused or line-service FBOs – Primarily focused on fuel supply, aircraft parking, and basic ramp services.

- Specialized or niche FBOs – Facilities tailored to specific operations such as charter aviation, aircraft maintenance, training, or helicopter services.

-

Together, these operators form a critical interface between airports, aircraft operators, and passengers, making FBOs one of the most important yet often overlooked components of the global aviation ecosystem.

The FBO Business Model and Revenue Economics

While FBOs offer a wide range of services from aircraft handling to passenger facilities the economic engine of the business is primarily driven by aircraft fuel sales and infrastructure utilization. Most FBOs operate through long-term lease agreements with airport authorities, allowing them to develop facilities such as hangars, fuel farms, and private terminals while generating revenue from aircraft operators and passengers.

Fueling remains the dominant revenue stream because nearly every aircraft movement requires refueling services, giving FBOs a recurring and volume-based income source. Beyond fuel, additional revenue is generated from aircraft parking, hangar rentals, ground handling services, and passenger-related amenities. Over the past decade, many FBO operators have expanded their offerings to include premium passenger terminals, concierge services, and aircraft management support, creating diversified income streams while improving customer experience for business aviation clients.

Once facilities such as hangars and terminals are established, incremental aircraft movements generate relatively strong margins, particularly when supported by high fuel throughput and premium service offerings.

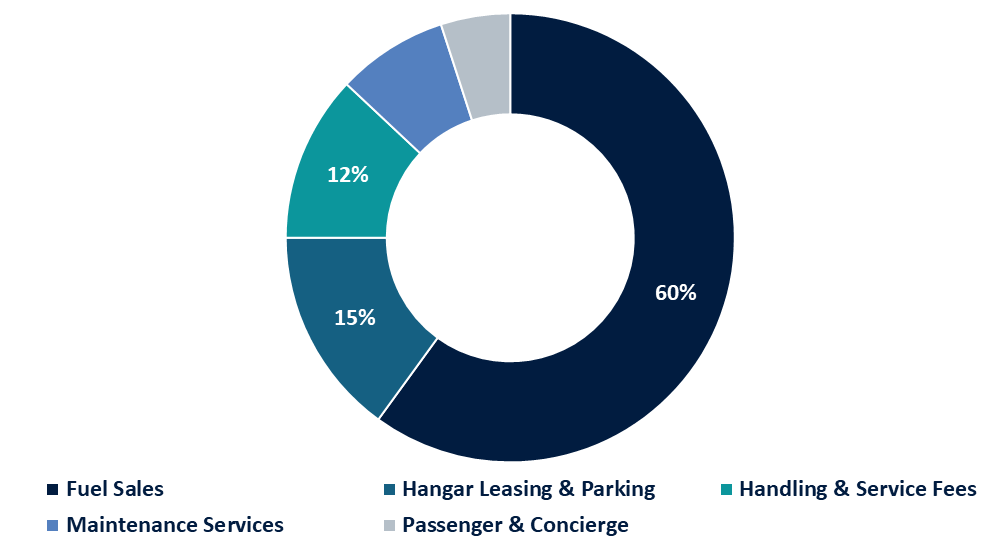

Typical Revenue Composition of FBO Industry

-

-

- Fuel Sales: Typically account for 50–70% of total FBO revenue, primarily through Jet-A fuel supply to business jets and charter aircraft.

- Hangar Leasing and Aircraft Parking: Long-term hangar rentals and short-term ramp parking can contribute 10–20% of revenues, particularly at high-traffic airports.

- Handling and Service Fees: Ground handling, de-icing, GPU services, and towing operations often generate 10–15% of revenues.

- Maintenance and Technical Services: Some FBOs offer aircraft maintenance and repair support, creating additional technical service income.

- Passenger and Concierge Services: VIP lounges, customs handling, catering, and luxury ground transport increasingly serve as high-margin ancillary services.

-

Key Economic Characteristics of FBO Operations

-

-

- Capital-Intensive Infrastructure: Hangars, fuel storage facilities, and private terminals require significant upfront investment.

- High Dependence on Fuel Volume: Profitability often scales with aircraft movements and fuel throughput.

- Location-Driven Economics: FBOs at major business aviation hubs typically achieve higher margins due to higher aircraft traffic and premium service demand.

-

For aviation investors and airport stakeholders, this combination of recurring fuel demand, infrastructure-based revenue, and premium service offerings makes the FBO model one of the most attractive segments within the broader general aviation ecosystem. Well-positioned FBOs at major business aviation hubs often generate EBITDA multiples in the range of 6×–10× during acquisitions, reflecting the sector’s strong cash-flow characteristics and investor interest.

The Global FBO Market Landscape and Competitive Structure

With the rise of corporate jet fleets, charter services, and private aviation demand, the FBO market has grown into a sizeable aviation services sector. The FBO market is projected to exceed $40 billion by 2030, reflecting steady growth driven by increased private aviation activity and new airport infrastructure developments.

Geographically, North America remains the dominant market, supported by the world’s largest fleet of business aircraft and a dense network of general aviation airports. Europe and the Middle East follow with established private aviation hubs such as London, Paris, Geneva, and Dubai, while Asia-Pacific is emerging as the fastest-growing region due to increasing wealth creation and business aviation adoption. The industry structure is moderately consolidated, with several large global networks operating alongside numerous independent regional FBO operators.

Major operators have expanded through acquisitions and multi-airport networks to capture aircraft traffic across key aviation corridors. For example, Signature Aviation operates more than 200 service locations across 27 countries, making it the largest global FBO network. Strategic consolidation has become a defining trend as operators seek to expand geographic coverage and strengthen customer relationships with aircraft operators and charter companies.

Major Global FBO Operators

-

-

- Signature Aviation – The world’s largest FBO network with 200+ locations across 27 countries.

- Atlantic Aviation – One of the largest operators in North America with 100+ locations across the United States.

- Jet Aviation – Global business aviation services provider operating around 30 FBO facilities worldwide.

- ExecuJet (Luxaviation Group) – International FBO operator with facilities across Africa, Europe, Asia-Pacific, the Middle East, and the Americas.

- Jetex – UAE-based premium FBO network known for luxury terminals and global trip support services.

-

For aviation stakeholders and investors, this evolving competitive landscape highlights an important strategic dynamic i.e. scale and location increasingly determine market leadership in the global.

Airport–FBO Relationship and Concession Models

Unlike airlines that operate directly within airport terminals, FBOs typically function through formal concession or lease agreements granted by airport authorities. Airports designate specific areas of their property for general aviation services and authorize qualified FBO operators to provide fueling, aircraft handling, hangaring, and passenger facilities. In this structure, the airport remains the infrastructure owner while the FBO acts as a commercial service provider responsible for developing and operating aviation support facilities.

Through long-term land leases or facility concessions, airports enable private operators to invest in hangars, fuel storage systems, and private terminals while ensuring compliance with operational and safety standards. In many cases, airports also define minimum standards that FBO operators must meet in terms of facility size, fuel capacity, staffing levels, and service capabilities to maintain operational consistency across the airport.

The concession structure creates a mutually beneficial economic relationship. Airports generate predictable revenue through land leases, fuel flowage fees, and concession payments, while FBO operators benefit from access to airport infrastructure and aircraft traffic.

Common FBO Concession and Lease Models

-

-

- Land Lease Model: Airports lease designated land parcels to FBO operators, who then invest in and construct hangars, terminals, and fuel infrastructure.

- Facility Lease Model: Airports build core infrastructure and lease operational facilities to an FBO operator for service delivery.

- Exclusive FBO Concession: Some airports authorize a single operator to provide all general aviation services.

- Multiple-FBO Model: Large business aviation airports often allow multiple FBO operators to promote competition and service quality.

-

Typical Revenue Flows Between Airports and FBOs

-

-

- Ground Lease Payments: Long-term leases (often 20 to 40 years) for airport land and facilities.

- Fuel Flowage Fees: Airports typically charge a per-gallon fee on aviation fuel sold by FBO operators.

- Concession or Percentage Fees: Some agreements include a share of revenues from services such as hangar rentals or handling operations.

- Infrastructure Investment Commitments: FBO operators frequently invest millions of dollars in hangars, fuel farms, and passenger terminals as part of concession agreements.

-

For airport authorities, this model transforms general aviation infrastructure into a stable, long-term revenue stream, while for FBO operators it provides access to high-value aviation traffic and long-duration operational rights at strategic airports. The effectiveness of this partnership model has been a key factor in the global expansion of the FBO industry.

Investment Case: Why Private Equity Is Entering the FBO Industry

In recent years, the FBO sector has attracted significant interest from private equity and infrastructure investors, largely due to its stable cash flows and strong linkage to the growth of business aviation. Unlike airlines, which are highly cyclical, FBO operators generate recurring revenues from fuel sales, hangar leasing, and aircraft handling services, making the business model relatively resilient. As a result, many investors increasingly view FBO platforms as infrastructure-like assets with predictable long-term returns.

A notable example of this trend occurred in 2021 when a consortium led by Blackstone Infrastructure Partners, Cascade Investment, and Global Infrastructure Partners acquired Signature Aviation, the world’s largest FBO network, in a deal valuing the company at approximately $4.7 billion. This transaction highlighted the growing institutional interest in scalable FBO networks that can expand across multiple airports and capture rising private aviation demand.

Why Investors are Targeting FBO Industry

- Predictable cash flows from fuel sales, hangar rentals, and service fees.

- Exposure to private aviation growth, particularly corporate and charter jet activity.

- Network expansion opportunities through consolidation across multiple airports.

- Strong operating margins, with mature FBO markets often achieving 20–30% margins.

Conclusion

FBOs have evolved into a critical infrastructure layer within the global aviation ecosystem, supporting the rapid expansion of business and private aviation. Beyond traditional fueling and ground handling, modern FBOs increasingly operate as integrated service platforms combining aviation operations, premium passenger facilities, and infrastructure-based revenue streams. As aircraft movements and private aviation demand continue to grow, the role of FBOs in enabling efficient, high-quality ground services will become even more central to airport operations worldwide.

From an investment perspective, the sector presents a compelling proposition. The combination of recurring fuel demand, long-term airport concessions, infrastructure-backed assets, and premium service offerings creates a resilient business model that continues to attract institutional investors and strategic operators. As consolidation accelerates and new markets emerge, FBO operators that secure strategic airport locations, scalable service networks, and differentiated customer experiences are likely to shape the next phase of growth in this specialized segment of the aviation industry.