Aviation MRO Landscape

Aviation Maintenance, Repair and Overhaul (MRO) covers the full set of activities required to keep aircraft airworthy across the airframe, engines, avionics and line-replaceable components. Practically this spans fast-turn, on-airport line maintenance (A checks, daily checks and troubleshooting), scheduled base maintenance (C- and D-check–level inspections conducted in hangars over days or weeks), and specialized component and engine shops that repair, overhaul or replace systems and powerplants.

Ownership and provider models are important determinants of strategy and margins. The market is a mix of:

-

-

- Airline-captive / in-house MROs (airlines operating maintenance to control cost/time-to-return on their own fleet).

- OEM-captive facilities (engine and component centers run or affiliated with manufacturers offering warranty, life-cycle services and proprietary OEM tooling).

- Independent third-party MROs (multi-brand shops competing on flexibility, turnaround and aftermarket supply-chain services).

- Specialist component and engine shops (highly technical centers of competence that capture higher value per labor hour).

-

Ownership structure shapes how maintenance work is allocated. Airlines tend to keep critical activities in-house or with OEM-affiliated MROs, while independent providers primarily benefit from outsourced work. This balance is evolving as airlines reassess operating costs, supply-chain resilience, and the advantages of local maintenance capabilities.

Where The Market is Heading: Three Short Signals for Stakeholders

-

-

- Digital + predictive maintenance adoption: Operators and MROs are accelerating use of data analytics, digital twins and predictive algorithms to reduce AOG time and extend on-wing intervals, making condition-based maintenance a key differentiator.

- Engine and component shop growth: Engine MROs (driven by new-generation turbofans and fleet renewals) are growing as a share of total spend which provides an attractive, and capital-intensive segment for investors and OEMs.

- Geographic rebalancing and localization: Asia, India in particular, is emerging as the fastest-growing market for incremental MRO demand as major OEMs and engine manufacturers are expanding facilities and local partnerships to capture outsourced work that was previously sent overseas. Recent facility investments and greenfield projects signal strong near-term capacity build-out.

-

Technology Adoption in Aviation MRO

The dominant technology theme in MRO is a shift from calendar-based maintenance to condition and data-driven approaches. Leading operators and OEMs are deploying predictive analytics, digital twins and AI to reduce Aircraft on Ground (AOG) time, optimize shop planning and extend on-wing intervals.

Concurrently, market participants are commercializing point solutions and embedding them in operational workflows. OEMs and large MRO groups are integrating AI assistants and digital inspection tools to speed fault diagnosis and knowledge transfer across their workforces. Independent software suites are being packaged with PBH and component support offerings. Also, partnerships between aerospace OEMs and cloud/AI vendors are accelerating at scale.

-

-

- GE’s collaboration with Microsoft and internal rollout of AI tools (e.g., AI assistants for technical staff) demonstrates how OEMs are embedding AI across maintenance workflows to accelerate troubleshooting and reduce manual effort. MROs should evaluate partnerships that combine domain expertise with scalable cloud & ML tooling.

- Honeywell and other major suppliers now offer integrated predictive maintenance suites and workforce-intelligence modules, making it easier for MROs and airlines to adopt capabilities without building everything in-house. This lowers the barrier to entry but raises governance and vendor-lock concerns.

-

Vendors and integrators are therefore offering packaged predictive suites, digital-twin services and generative-AI assistants rather than point tools. The near-term priority for MROs is to focus investments on data integration, governance, and a limited set of high-ROI use cases (AOG reduction, shop throughput and inventory optimization) rather than broad technology experimentation.

Strategic Transactions & Partnerships Reshaping Aviation MRO

The past 18 months have seen a marked acceleration in strategic transactions and industrial partnerships across the MRO value chain, driven by persistent shop-capacity tightness, durability issues on new-generation engines, and reorientation by airlines toward resilience and localization. Financial players and aftermarket specialists are consolidating capabilities that capture high-margin spare-parts, component repair and engine-shop value evidenced by large acquisitions that both broaden product portfolios and secure proprietary repair technologies.

At the same time OEMs are selectively expanding local service footprints through joint ventures with national carriers and local partners to keep work closer to demand centers and to manage political/regulatory friction.

Commercial-scale technology and service collaborations are also reshaping how maintenance is delivered. Large OEMs and systems integrators are bundling digital services, cloud platforms and AI capabilities with traditional maintenance offerings to create integrated service propositions (predictive analytics + spare-parts fulfilment + PBH-type agreements).

-

-

- Large aftermarket consolidations: Private equity and strategic buyers are acquiring high-margin aftermarket businesses to scale parts and repair capabilities. TransDigm’s 2026 acquisitions of Jet Parts Engineering and Victor Sierra Aviation are emblematic of this trend.

- OEM vertical integration via acquisitions: Engine and component makers are buying specialized repair shops to secure repair know-how and shorten lead times. Safran’s acquisition of Component Repair Technologies (CRT) is a recent example of creating such regional centers of excellence.

- Regional capacity and JV expansion: OEM–airline and OEM–local partner JVs that expand regional shop capacity are materially reshaping where outsourced work will flow. Such projects are particularly visible in China and India.

-

Capital Flows and Investor Thesis – Why MRO is Attracting Strategic Capital

The aviation MRO sector has emerged as a compelling investment frontier due to its combination of resilient demand, high aftermarket margins and structural supply constraints that underpin longer-duration cash flows. Unlike cyclical airline operations, MRO services benefit from fleet ageing and delivery delays that extend maintenance cycles, creating predictable demand streams. As a result, both strategic and financial investors are allocating capital to established MRO platforms and specialized service providers.

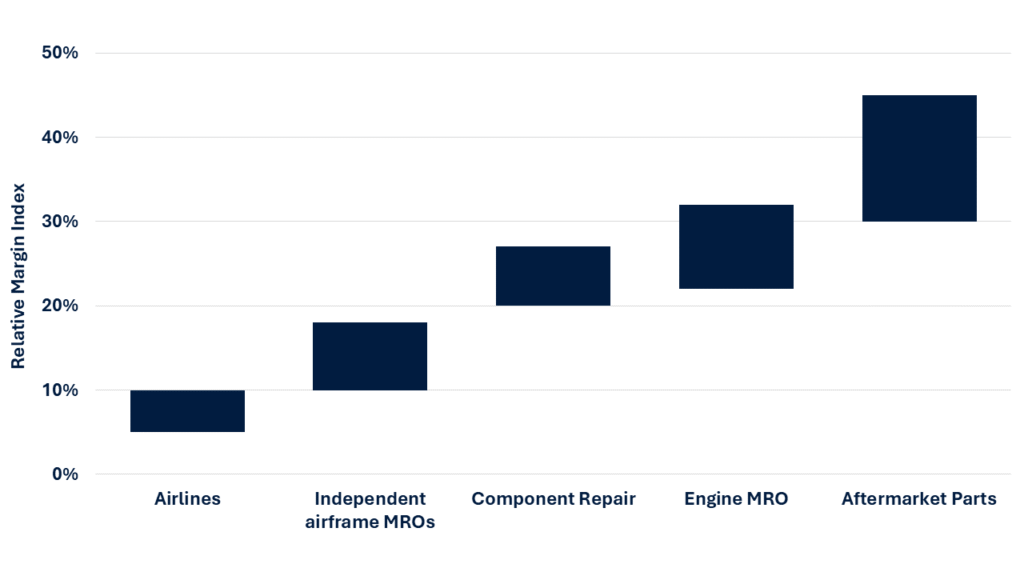

Relative Margin Index Across the Aviation Value Chain

For example, MRO Holdings Inc. received a strategic growth investment from Bain Capital in 2024 to scale maintenance and modification services across the America, reflecting private equity confidence in MRO’s recurring revenue profile. Concurrently, AE Industrial Partners launched an aerospace MRO services platform with its investment in Air Transport Components, signaling that buy-and-build strategies targeting niche repair capabilities are gaining traction in capital markets.

Recent activity also underscores broader investor conviction in aftermarket consolidation and capability depth. The acquisition of West Star Aviation by Greenbriar Equity Group, supported by KKR-backed financing, illustrates how private capital is refinancing and expanding established maintenance providers to capture outsized aftermarket margins and scale. These transactions typify a broader investor strategy of combining stable demand drivers with operational leverage and digital enablement to deliver differentiated value in a market projected to grow significantly over the next decade.

Conclusion: Aviation MRO as a Structural Opportunity

Fleet growth, delayed aircraft deliveries, next-generation engine complexity, and tightening regulatory and workforce constraints are collectively shifting value toward maintenance, repair and aftermarket services. In this environment, scale, certification depth, data access and capital strength increasingly determine competitive advantage, explaining the accelerating convergence of OEMs, independent MROs, financial sponsors and technology providers.

Airlines must reassess build-versus-buy choices through a resilience and lifecycle-cost lens. MRO operators need to prioritize selective scale, technology enablement and partnerships. Investors should focus on segments where durability, pricing power and contractual visibility intersect. Those who move early, anchored by a clear thesis on where value will accrue, will shape the next phase of the global MRO landscape, rather than merely participate in it.