Strategic Imperative: Military EO/IR Systems as the Foundation of Modern Battlespace Awareness

Electro-Optical and Infrared (EO/IR) systems have transitioned from being auxiliary imaging tools to becoming the primary sensory backbone of modern military operations. In an environment defined by contested domains, asymmetric threats, and compressed decision timelines, the ability to see, interpret, and act in real time has become a decisive advantage. EO/IR systems today are not merely supporting ISR (Intelligence, Surveillance, Reconnaissance); they are increasingly embedded at the core of target acquisition, threat detection, navigation, and mission execution across air, land, and maritime platforms. As warfare evolves toward multi-domain operations, EO/IR capabilities are emerging as the first layer of battlefield intelligence, enabling forces to operate effectively in both permissive and denied environments.

This evolution signals a fundamental shift in how military EO/IR systems are valued and procured. The market is no longer driven purely by optical performance or sensor resolution; instead, emphasis is moving toward integrated sensing ecosystems that combine hardware, software, and analytics. As a result, EO/IR providers are increasingly expected to move up the value chain, aligning their offerings with broader C4ISR frameworks and autonomous systems.

Key strategic shifts shaping EO/IR’s role:

-

-

- Transition from imaging systems → real-time intelligence enablers

- Increasing integration with AI/ML for automated target recognition and tracking

- Central role in multi-domain operations (MDO) and network-centric warfare

- Rising importance in unmanned and autonomous platforms, especially UAVs

- Convergence with other sensing modalities (radar, EW) through sensor fusion architectures

- Growing demand for edge processing and low-latency decision support in contested environments

-

Value Capture in EO/IR: From Components to Control of the Mission Stack

The EO/IR value chain is often misunderstood because technical sophistication does not directly translate into economic power. At a structural level, the stack progresses from detector materials (HgCdTe, InSb) → focal plane arrays → optics → sensor modules → stabilized payloads (gimbals, targeting pods) → mission systems & ISR software. While the lower layers carry high entry barriers and deep engineering complexity, they operate largely in a spec-driven, qualification-heavy environment where pricing is constrained, substitution risk exists, and differentiation is incremental. In contrast, the upper layers particularly payload integration and mission systems benefit from program-level ownership, where vendors are selected not for components, but for end-to-end operational capability.

What fundamentally shapes value capture is defense procurement logic, not just technology. EO/IR is almost always acquired as part of a platform program (fighter aircraft, UAVs, armored vehicles, naval systems) or as an integrated ISR package. Once a system is qualified on a platform, it typically remains embedded across long lifecycle programs (often 15+ years), creating downstream value through upgrades, maintenance, and software enhancements. This results in a clear hierarchy: component suppliers compete on specifications and cost, while system integrators compete on trust, integration depth, and lifecycle ownership.

Where value concentrates across the stack:

-

-

- Lower tiers (detectors, optics): high barriers but limited pricing power due to standardization and regulatory constraints

- Mid-layer (sensor modules): increasingly commoditizing, especially in UAV and portable systems

- Upper layer (gimbals, targeting systems): strong value capture driven by platform integration complexity and qualification cycles

- Top layer (mission systems, AI, ISR software): highest control point defines decision-making, not just data capture

-

Firms that remain component-focused are structurally exposed to margin compression, while those that move upward into payload integration, system architecture, or data exploitation layers gain disproportionate influence over both procurement decisions and long-term revenue streams. In practice, the industry is shifting from a product hierarchy to a control hierarchy, where the ability to connect sensing with actionable outcomes determines who captures value.

Platform-Led Economics: How Platform Demand Drives the Military EO/IR Business

Every force structure decision a defense ministry makes i.e. how many UAVs to field, how aggressively to modernize armor, how many vessels to commission translates directly into sensor procurement. The current procurement landscape is being shaped by three distinct platform economics: the unmanned air surge, the soldier modernization wave, and maritime surveillance.

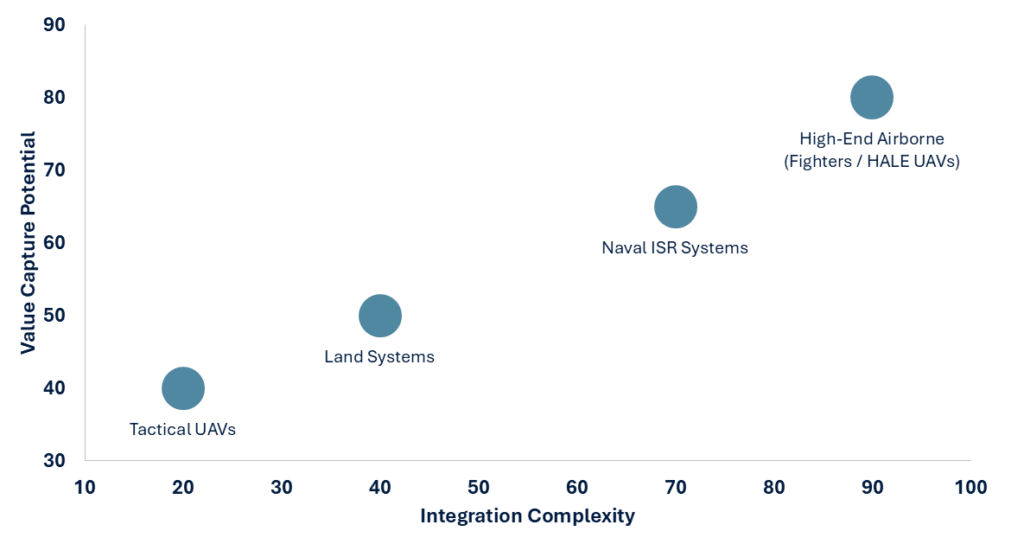

Platform vs Value Capture in EO/IR Systems

The unmanned vector is the most visible demand driver, but it is not monolithic. The FY2026 global defense budget reflects a turbulent landscape that favors affordable, modular, and rapidly fieldable unmanned systems particularly small UAS and loitering munitions while legacy MALE-class programs face growing cost and schedule scrutiny.

General Atomics’ Gray Eagle, for instance, was placed on the chopping block by Army leadership in 2025 as part of a broader acquisition overhaul that canceled procurement of legacy systems, a direct signal that EO/IR suppliers tied to aging MALE platforms need to reposition toward next-generation airframes.

On the soldier modernization side, the demand signal is exceptionally clear and contractually anchored. For example, L3Harris holds a full-scale production IDIQ for the ENVG-B, the Army’s fused thermal and image-intensified goggle, valued at nearly $1 billion over 10 years, with the first order placed in April 2024 at $256M and a second at $263M following in January 2025.

What this platform map ultimately tells a supplier is that the demand architecture is bifurcating. Large legacy airborne platforms are being rationalized, but the disaggregated end of the market i.e. small UAS payloads, soldier-worn sensors, vehicle-mounted systems is growing in volume and contract frequency. The Marine Corps, for example, reached a saturation point on short-range small UAS in FY2026 and shifted toward longer-range, longer-endurance platforms illustrating that even within the unmanned category, platform saturation creates demand cliffs that suppliers must anticipate. The companies winning in this environment are those reading platform-level acquisition intent early enough to shape their roadmap before the RFP.

Strategic Control Points: Supply Chain Resilience and Sovereign Capability in EO/IR

Beneath the surface of EO/IR innovation lies a decisive battleground i.e. control over critical technologies, materials, and production ecosystems. The EO/IR supply chain is structurally constrained by limited global access to detector fabrication, advanced optics, and cryogenic systems, making it highly sensitive to export controls and geopolitical alignment. This has elevated EO/IR into a sovereign capability domain, where nations are actively reducing dependence on foreign suppliers.

A clear example is India’s push toward indigenous EO/IR development through the Defense Research and Development Organization, which has developed multi-platform EO/IR systems for airborne, naval, and land surveillance, reducing reliance on imported payloads. More recently, indigenous sensor suites integrating EO/IR with radar and electronic warfare systems have been deployed on patrol aircraft, demonstrating a shift from component import to full-stack capability development.

At the same time, countries are not pursuing sovereignty in isolation. They are building Industry–University–Research (IUR) ecosystems to accelerate capability development in denied technologies. Programs such as DRDO’s Industry Academia Centers of Excellence (DIA-CoEs) bring together academia, startups, and defense labs to develop advanced electro-optical technologies, AI-enabled imaging, and next-generation sensing systems. Similar models are visible globally across NATO and allied ecosystems, where collaborative R&D is used to de-risk technology development while maintaining strategic control. This dual approach localized manufacturing + collaborative innovation is emerging as the dominant response to supply chain vulnerabilities.

For EO/IR companies, this environment changes the basis of competition. Success increasingly depends on alignment with national programs, participation in collaborative R&D ecosystems, and control over critical supply nodes because in today’s defense landscape, supply chain positioning is as strategic as product capability itself.

Strategic Transition: From Imaging Vendors to Integrated Intelligence Providers

The EO/IR industry is undergoing a structural shift from delivering high-performance imaging hardware to enabling end-to-end battlefield intelligence. As modern defense architectures prioritize speed of decision-making over data collection, the competitive advantage is moving toward companies that can integrate sensing, processing, and actionable outputs within a unified system.

For companies looking to enter or scale within this market, the pathway is no longer linear. Success depends on strategic positioning within the value chain rather than standalone product excellence.

-

-

- Enter via component specialization (detectors, optics) where deep-tech capability exists, but plan upward integration

- Target platform-specific niches (e.g., UAV payloads, naval surveillance systems) aligned with platform-led demand

- Build or partner for AI/analytics layers to move closer to the decision-making interface

- Collaborate within defense ecosystems (IUR models, local partnerships) to meet sovereignty and procurement requirements

-

Ultimately, EO/IR companies that remain hardware suppliers will compete on price, while those that evolve into integrated intelligence enablers will define the future of the battlespace.