Between 75% and 96% of all maritime accidents are attributed to human error. Over 90% of global trade moves by sea and in 2025, maritime cyberattacks doubled compared to the prior year. These three facts alone explain why autonomous naval vessels have moved from experimental curiosity to strategic imperative and why the maritime industrial base, from shipbuilders to component suppliers to repair yards, must begin repositioning now.

The International Maritime Organization is finalizing its non-mandatory MASS Code for adoption in May 2026. Navies from United States to the United Kingdom to South Korea are accelerating unmanned vessel procurement and threat actors are increasingly targeting the very digital systems that make autonomy possible.

Understanding The Autonomy Spectrum

The IMO defines four degrees of vessel autonomy, ranging from crewed ships with automated decision support (Degree 1) to fully autonomous vessels with no human involvement (Degree 4). This distinction matters operationally and commercially because it shapes design requirements, crew training obligations, classification standards, and insurance frameworks.

Most vessels currently in operation or advanced testing fall within Degrees 1 and 2, semi-autonomous systems where human operators remain in the loop, either onboard or from shore-based remote operation centers (ROCs). The remotely operated segment currently represents the dominant share of autonomous vessel deployments, as operators seek standoff capabilities while retaining human control in high-risk scenarios.

Fully autonomous operations remain limited to controlled environments such as Norway’s Yara Birkeland, a battery-electric container ship conducting short coastal voyages, and Kongsberg’s successful autonomous inland waterway trials in Belgium, where the vessel Zulu completed a 16.5-kilometre circuit on the Rupel River with autodocking, auto-crossing, and automatic navigation systems. In June 2022, HD Hyundai’s Avikus completed the first transoceanic autonomous voyage of a large LNG carrier, covering over 10,000 kilometers from the Gulf of Mexico to South Korea.

The semi-autonomous segment, combining automation with human oversight, currently represents the dominant share of deployments globally, accounting for roughly 70% of the market in 2025. This reflects a pragmatic reality where fully autonomous AI systems are not yet mature enough to handle every scenario at sea, from severe weather to equipment malfunction, without human fallback. Classification societies have developed their own notation systems for autonomous vessels, creating additional layers of standards that shipbuilders must navigate.

The trajectory is clear, i.e. autonomy is graduating from pilot projects to operational deployment, and each degree introduces distinct requirements for shipbuilders, equipment manufacturers, and service providers.

Global Naval Defense Programs: The Primary Demand Signal

Military and law enforcement applications remain the dominant driver of autonomous vessel investment. Defense-oriented vessels account for approximately 70% of U.S. autonomous ships market, and similar patterns hold across allied navies.

United States: The U.S. Navy’s journey from DARPA’s Anti-Submarine Warfare Continuous Trail Unmanned Vessel (ACTUV) program which produced the Sea Hunter trimaran in 2016, demonstrating continuous autonomous operation over 5,000 nautical miles to today’s fleet of Ghost Fleet Overlord vessels illustrates the scale of ambition. Ghost Fleet USVs collectively steamed more than 267,000 miles, with 70% in autonomous mode, carrying mission payloads including live missile firings from containerized vertical launch systems.

In 2025, the Navy merged its Large and Medium Unmanned Surface Vessel programs into the Modular Attack Surface Craft (MASC) program. MASC prioritizes non-exquisite vessels built to commercial standards that multiple shipyards can produce, repair, and maintain, a deliberate signal to broaden the industrial base. The FY2026 prototyping phase is underway, with the Navy seeking first deliveries within 18 months of prototype awards. The newly established Unmanned Surface Vessel Squadron One (USVRON-1) and its Chimera detachments are already operating Sea Hunter, Seahawk, Ranger, Mariner, and the purpose-built NOMARS vessel Defiant, launched in March 2025.

United Kingdom: In March 2025, the Royal Navy received its first autonomous mine-hunting system developed by Thales, employing AI and advanced sensors to detect and neutralize naval mines without endangering personnel.

Asia-Pacific: South Korea is investing heavily in intelligent navigation systems and integrated ship platforms. Japan continues advancing semi-autonomous systems for commercial shipping under stringent cybersecurity guidelines. Australia’s partnership with Anduril on the Ghost Shark extra-large autonomous underwater vehicle represents one of the most ambitious UUV programs globally.

Undersea Dimension: In February 2025, Kongsberg Discovery delivered its HUGIN Superior autonomous underwater vehicle to the U.S. Navy, designed for mine countermeasures, seabed warfare, and infrastructure inspection, with full ocean depth capability and over 70 hours of endurance. DARPA’s Manta Ray, a glider-like submersible designed to hibernate on the ocean floor until activated, adds further depth to the autonomous naval portfolio.

The collective message for the maritime industrial base is unambiguous, i.e. procurement pipelines are opening, and they favour companies that can deliver modular, software-rich, commercially maintainable platforms.

The Regulatory Clock: IMO MASS Code and National Frameworks

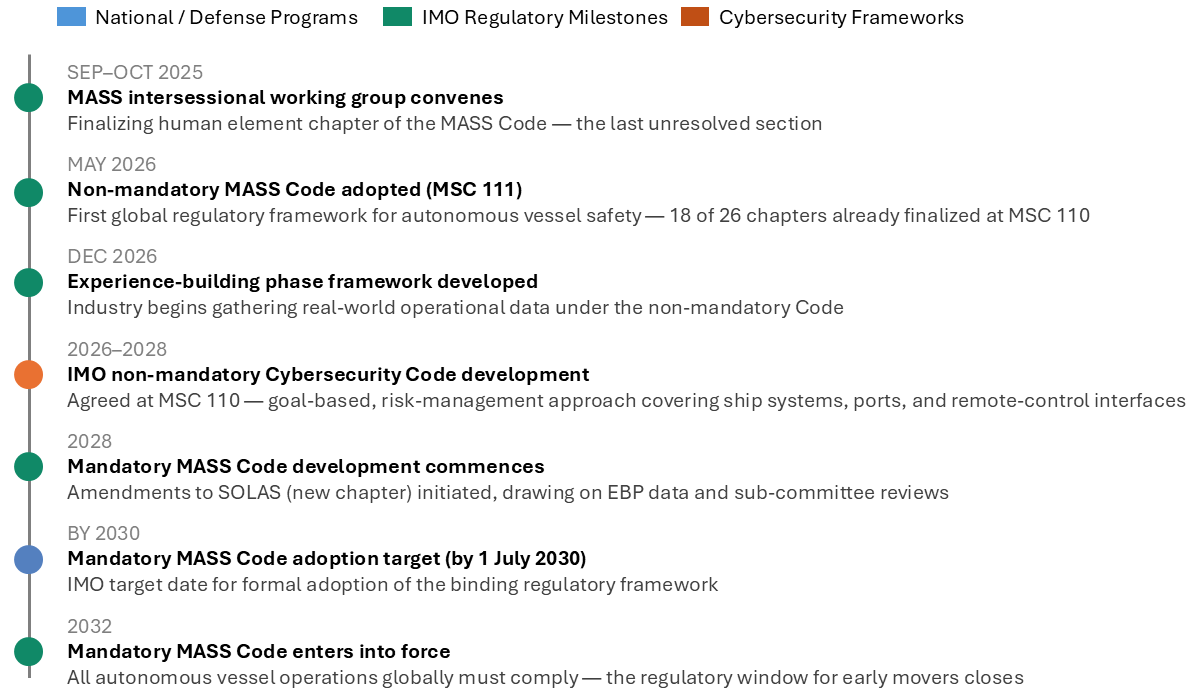

The IMO’s Maritime Safety Committee has been developing the MASS Code across multiple sessions. At MSC 110 (June 2025), 18 of the Code’s 26 chapters were finalized, with only the human element chapter remaining. The revised roadmap sets the following milestones:

-

-

- May 2026 (MSC 111): Adoption of the non-mandatory MASS Code

- December 2026 (MSC 112): Framework for the experience-building phase

- 2028: Development of the mandatory Code begins, with amendments to SOLAS

- By 1 July 2030: Adoption of the mandatory MASS Code

- 1 January 2032: Mandatory Code enters into force

-

A critical decision at MSC 110 established that unmanned ships must be able to assist people in distress at sea meaning even crewless vessels will require search and rescue capability planning. This will directly impact hull design, onboard systems, and operational protocols.

Separately, the IMO agreed at MSC 110 that a non-mandatory Cybersecurity Code should be developed, marking the beginning of a formal regulatory stream that will likely expand to cover ship systems, ports, and remote-control interfaces.

Classification societies are also issuing their own technical requirements and guidelines, such as IACS Unified Requirements E26 and E27, effectively becoming gatekeepers for autonomous vessel certification.

IMO MASS Code Roadmap & Convergence of Global Autonomous Vessel Milestones, 2025–2032

Maritime Cybersecurity: The Escalating Existential Risk

Autonomous vessels dramatically expand the attack surface for cyber adversaries. Unlike traditional ships, where cybersecurity concerns centered on navigation and cargo systems, autonomous vessels present interconnected vulnerabilities across AI-driven navigation, sensor fusion, satellite communications, shore control center links, and supply chain software.

The scale of the threat is accelerating. Maritime cyberattacks doubled in 2025, led by an explosion of malware and distributed denial-of-service incidents. Also, approximately 23,400 malware detections and 178 ransomware attacks were reported across 1,800 vessels in the first half of 2024 alone. The “Lab Dookhtegan” attack on Iranian state-owned tankers demonstrated how a compromised satellite communications provider can grant fleet-wide access. The attackers penetrated the satcom provider, seized control of ship-to-shore VOIP services, stole corporate documents, and ultimately destroyed the ships’ modems by overwriting partitioned memory, requiring physical hardware replacement.

NATO’s Cooperative Cyber Defense Centre of Excellence (CCDCOE) has identified nine distinctive threat categories specific to autonomous vessels: attacks disrupting radio frequency signals; attacks deceiving or degrading sensors; interception or modification of communications; attacks on operational technology systems; attacks on information technology systems; attacks on AI used for autonomous operations; supply chain attacks; attacks through physical access; and attacks on shore control centers.

GPS spoofing and AIS manipulation, which have surged in geopolitically sensitive regions like the Black Sea and Persian Gulf, pose particularly acute risks for autonomous vessels that depend heavily on satellite-based positioning without traditional fallback mechanisms.

For the maritime industrial base, cybersecurity is not merely an IT concern, but it is becoming a design requirement, a procurement criterion, and a regulatory obligation. Shipbuilders will need to embed “secure by design” principles into hull and systems architecture from the outset, not as a retrofit afterthought. Ship repair and retrofit companies will face growing demand for cybersecurity hardening of existing fleets transitioning toward greater automation.

AI agent-assisted attacks will become more prevalent with 2025 marking as the beginning of an era of autonomous attacks with largely or fully AI-directed hacking campaigns. The maritime sector, responsible for carrying over 90% of international commerce, is an increasingly high-value target.

Strategic Implications for the Maritime Industrial Base

The shift toward autonomous naval vessels is fundamentally altering where value resides in the maritime supply chain. Traditional shipbuilding has centered on steel fabrication, propulsion systems, and outfitting. Autonomous vessels shift the value center toward sensors, software, AI navigation systems, communication infrastructure, and systems integration.

Several implications stand out for industry participants:

For shipbuilders, the MASC program’s emphasis on “non-exquisite” commercial-standard vessels signals that navies want hulls that are affordable, rapidly producible, and maintainable by multiple yards. This opens opportunities for mid-tier shipyards and commercial builders that can demonstrate modular construction capability and containerized payload integration. The ability to build autonomy-ready hulls with pre-wired sensor arrays, redundant power systems, and software-upgradeable architectures will become a competitive differentiator.

For ship repair and maintenance companies, the autonomous vessel fleet will generate an entirely new service category. These vessels require specialized maintenance of AI systems, sensor calibration, software lifecycle management, and cybersecurity auditing. The U.S. Navy’s explicit requirement that MASC vessels be repairable at commercial facilities, rather than dedicated naval shipyards, creates a significant addressable market for commercial repair yards.

For equipment and component suppliers, demand is intensifying across navigation systems, collision avoidance sensors, LiDAR and radar arrays, satellite communication terminals, autonomous control software, and electric/hybrid propulsion systems. Suppliers with dual-use (military and commercial) product lines will be especially well positioned as both naval and commercial autonomy programs scale.

For the broader supply chain, tariff pressures are adding complexity. The 25% tariff on steel and aluminum imports implemented by U.S. in March 2025, along with the Section 301 investigation into Chinese shipbuilding dominance, are reshaping procurement strategies. Regionally, Asia-Pacific holds the largest share of the autonomous vessel market driven by massive smart shipping investments from South Korea, Japan, and China. India’s Maritime Vision 2030 aims to capture 5% of global shipbuilding orders through smart yard initiatives, and Saudi Arabia’s Ras Al-Khair complex is targeting autonomous-ready shipbuilding capability.

Meanwhile, the physical security dimension persists. There were 116 incidents against ships in 2024 including 94 boardings and 6 hijackings underscoring the operational demand for autonomous patrol and surveillance vessels that can operate in high-risk areas without jeopardizing human lives.

Deal Activity Signals: Consolidation, Partnerships, and Capital Inflows

The autonomous maritime sector is experiencing a surge of strategic deal-making that reveals how seriously both defense primes and venture-backed entrants are positioning for this market. The pattern is consistent where technology companies are partnering with established shipbuilders to combine software-defined autonomy with proven hull fabrication at scale, while capital markets are rewarding companies that can demonstrate production readiness.

The most consequential partnership of 2025 was Anduril Industries’ alliance with South Korea’s HD Hyundai Heavy Industries, announced in November, to co-develop a new class of modular autonomous surface vessels targeting U.S. Navy’s MASC program. The first prototype is already being fabricated in Korea, with future production to shift to a reactivated Foss Shipyard in Seattle. This model, foreign shipbuilding expertise paired with domestic defense technology integration, may well become the template for how allied nations collaborate on autonomous naval platforms going forward.

Saronic Technologies raised $600 million in a Series C round in February 2025 at a $4 billion valuation, then followed with a reported $1.75 billion raise in early 2026 catapulting its valuation to $9.25 billion. The company also secured a $392 million Navy production Other Transaction Authority contract through 2031, acquired Gulf Craft (April 2025) to expand shipbuilding capacity, announced a $300 million investment to create 1,500 jobs at a Franklin shipyard (December 2025), and formed strategic partnerships with Palantir for autonomous naval capabilities and Vigor Marine Group for West Coast maintenance and repair.

Marine Thinking, a Canadian autonomous ship and fleet solutions provider, entered a SPAC merger with Eureka Acquisition Corp in October 2025 at approximately $130 million pre-money valuation, targeting a NASDAQ listing, one of the first public-market vehicles dedicated specifically to autonomous vessel technology.

Conclusion

The IMO’s MASS Code will create the first global regulatory framework by 2026, with mandatory enforcement by 2032. Naval procurement programs across U.S., UK, Australia, South Korea, and elsewhere are moving from prototyping to production and cybersecurity threats are escalating at a pace that demands embedded defenses.

The decisions that maritime industry leaders make in the next 24 months will determine which companies emerge as qualified, certified, and operationally proven suppliers when procurement scales and which find themselves scrambling for compliance with diminishing competitive leverage.

For shipbuilders, repair yards, equipment suppliers, and maritime service providers, the window of competitive advantage is defined by the next three years. Companies that align their capabilities, partnerships, and workforce with the autonomous transition today will define the maritime industrial base of the next decade.