Executive Summary

The global cyber insurance market is at a critical inflection point. Once viewed as a straightforward risk-transfer mechanism, it has rapidly evolved into a complex and indispensable component of corporate cybersecurity strategy. However, the market is characterized by a severe hardening of conditions: premiums are soaring, coverage is narrowing, and underwriting scrutiny is intense.

For C-suite leaders and board members, navigating this landscape is no longer a task for the insurance department alone; it requires a strategic, cross-functional approach that aligns risk management with business continuity. This briefing analyzes the forces shaping the $13.5 billion market and provides a framework for organizations to secure robust coverage, improve their security posture, and treat cyber insurance as a strategic asset rather than a mere compliance checkbox.

The Market Paradox: Unprecedented Growth Meets Unprecedented Scrutiny

The demand for cyber insurance is exploding, driven by the escalating frequency, sophistication, and cost of cyberattacks. A recent ransomware attack occurs every 11 seconds, and the global average total cost of a data breach has reached nearly $4.5 million. With ransomware accounting for 41% of claims and supply chain vulnerabilities impacting 45% of organizations, policies now emphasize parametric triggers and AI-driven risk assessments to expedite payouts and reduce denials, which hover at 27%.

This evolution incentivizes controls such as zero-trust architectures, yielding 20-30% premium discounts for fortified entities. In this environment, cyber insurance has shifted from a niche product to a board-level imperative. This demand has fueled remarkable market growth. The global cyber insurance market is projected to expand at a CAGR of 24% over next decade. This growth, however, belies a fundamental market correction. After years of soft market conditions, insurers are now enforcing rigorous discipline, leading to a pronounced hard market.

Market leaders like Chubb, AXA XL, and Travelers are commanding 55% of volumes through advanced underwriting and parametric offerings. Disruptors such as Coalition and At-Bay gain traction via data-centric platforms, partnering with tech giants like Microsoft for threat intelligence, capturing 15% annual growth in SME segments. M&A activity, up 20%, exemplifies consolidation, witness SecurityScorecard’s alliances enhancing quantification models by 40%.

Deconstructing the Hard Market: A Confluence of Systemic Pressures

The current hard market is not a temporary fluctuation but a structural response to systemic risks. Three primary forces are driving this transformation:

-

-

- Loss Ratios and Ransomware Epidemic: Insurers faced unsustainable loss ratios, often exceeding 70%, primarily fueled by the rampant surge in ransomware attacks. These attacks are not only costly in terms of extortion payments but also in associated incident response, business interruption, and regulatory fines.

- Systemic Risk Concerns: The interconnected nature of digital ecosystems creates systemic risk. A single vulnerability in widely used software (e.g., the Log4j flaw) or a critical cloud service provider can trigger a cascade of claims across thousands of policies simultaneously, threatening insurer solvency.

- Information Asymmetry: Initially, insurers lacked historical data and expertise to accurately price cyber risk. They are now aggressively closing this gap through sophisticated modeling and demanding detailed security information from applicants.

-

The New Underwriting Reality: From Checkbox to Rigorous Audit

The application process has transformed. Underwriters now act as de facto cybersecurity auditors. Generic questions have been replaced by exhaustive, technical questionnaires requiring evidence-based responses. Key areas of scrutiny include:

-

-

- Multi-Factor Authentication (MFA): Is it enforced universally, especially for remote access and privileged accounts?

- Endpoint Detection and Response (EDR): Is a next-generation solution deployed and actively managed?

- Privileged Access Management (PAM): How are administrative credentials controlled and monitored?

- Backup and Recovery: Are backups segmented from the main network, regularly tested, and immutable?

- Security Awareness Training: Is there a documented, recurring program with phishing simulations?

-

Failure to demonstrate maturity in these areas will result in significantly higher premiums, sublimits on critical coverage like ransomware, or outright declination.

The Evolution of Cyber Insurance Underwriting Requirements

|

Era |

Primary Focus (Soft Market) | Primary Focus (Hard Market) | Impact on Premium & Coverage |

|

Pre-2019 |

Basic security hygiene (firewall, antivirus). |

Limited scrutiny; broad terms. |

Lower premiums, broader coverage. |

| 2020-2022 | Specific controls (MFA, backups). | Increased questioning on key controls. |

Rising premiums, introduction of sublimits. |

|

2023-Present |

Security Posture & Resilience. | Evidence-based audits, third-party attestations, continuous monitoring. |

Risk-based pricing; stringent terms; coverage tied to security practices. |

Strategic Implications: Beyond the Policy Document

In this new reality, a reactive approach to cyber insurance is fraught with risk. Leadership must adopt a strategic posture centered on three pillars:

-

-

- Treat Insurance as a Strategic Dialogue, Not a Transaction: The application process is an opportunity to demonstrate your organization’s cyber maturity to a sophisticated third party. Prepare for it as you would for a board presentation or a regulatory exam. Involve your CISO, CIO, and risk management team early.

- Align Insurance with Your Cybersecurity Investment Strategy: Use the underwriting requirements as a roadmap for strategic security investments. Implementing robust EDR or PAM solutions not only improves your insurability but also directly reduces your risk of a catastrophic breach. This creates a virtuous cycle of risk reduction and cost management.

- Prepare for the Claims Process Before an Incident: A policy is only as good as the recovery it enables. Ensure your incident response plan is integrated with your policy’s requirements. Know your obligations for breach counsel, forensic investigators, and public relations firms – often pre-approved by the insurer. Conduct tabletop exercises that include notifying your insurer.

-

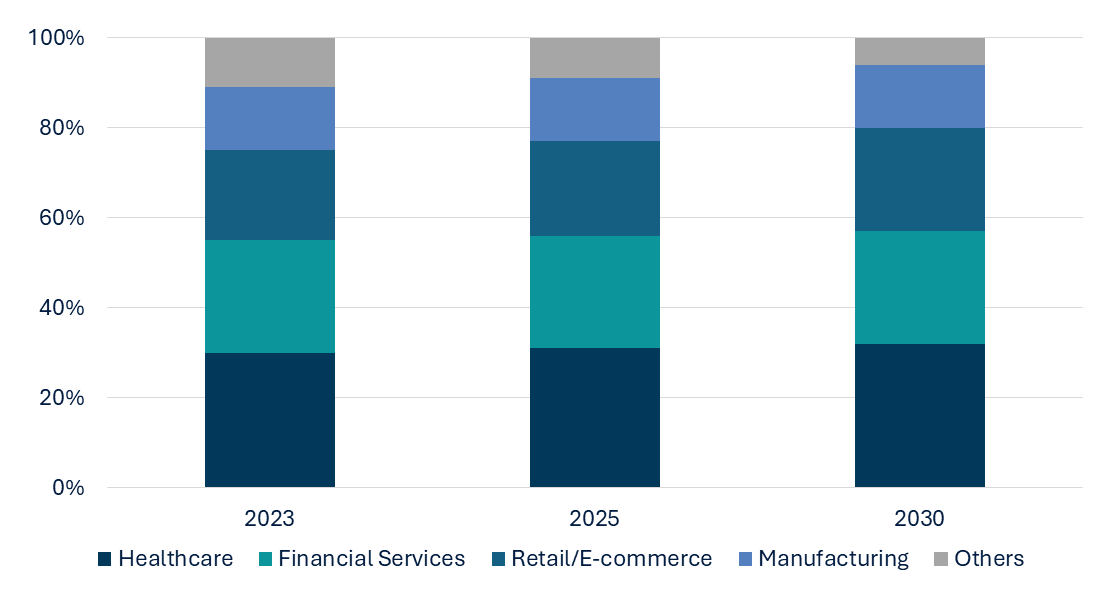

Global Cyber Insurance Premiums by Industry Vertical

The Future Outlook: Risk Sharing and Parametric Triggers

Looking ahead, the market will continue to evolve toward more sophisticated risk-transfer mechanisms. We anticipate:

-

-

- Greater Use of Co-insurance and Deductibles: Insurers will mandate that organizations retain a larger portion of the risk, ensuring alignment of incentives.

- Rise of Parametric Insurance: Policies with pre-agreed payouts triggered by specific, objective events (e.g., a confirmed ransomware event on critical servers) will gain traction, offering faster payouts for business interruption.

- Integration with Cybersecurity Services: Policies will increasingly bundle insurance with proactive services like threat intelligence, security assessments, and incident response retainer, transforming insurers into true risk partners.

-

Conclusion: From Cost Center to Strategic Enabler

The era of easy cyber insurance is over. The hard market is a permanent correction that demands a strategic response. Organizations that view cyber insurance as a mere cost center will face exorbitant premiums and inadequate coverage. Leaders must conduct comprehensive risk audits to align coverage with evolving regulations like NIS2 in Europe and SEC mandates in the US, averting fines that constitute 25% of breach costs. The protection gap remains acute, 80% of large firms are insured, versus just 10% of SMEs – unlocking over USD 70 billion in potential by 2033 through tailored, scalable products.

The winning strategy is to reframe cyber insurance as a strategic enabler of resilience. By leveraging the underwriting process to benchmark and improve security posture, aligning investments with risk reduction, and preparing meticulously for incident response, organizations can not only secure favorable insurance terms but also build a more defensible and resilient enterprise. The mandate for leadership is clear: integrate your cyber insurance strategy with your overall cybersecurity and business continuity framework or accept significantly higher levels of unmitigated risk.

Secure your coverage and strengthen your resilience, schedule a cyber risk assessment with our experts today.