Executive Summary

For decades, the thermal management system in an automobile was engineering plumbing covering a radiator, a water pump, a thermostat, and a network of hoses. It sat in the background, reliably unglamorous, while powertrain engineers and designers commanded attention and capital.

The electrification of the global automotive fleet has elevated thermal management from a peripheral subsystem to a decisive enabler of vehicle performance, range, safety, and longevity. A battery electric vehicle demands two to three times the thermal management content of a conventional internal combustion engine vehicle. Where a traditional ICE powertrain required a cooling package worth approximately USD 300–400, a modern EV platform embeds USD 800–1,200 or more in thermal hardware and controls across battery packs, power electronics, drive motors, and cabin conditioning. This structural step-change in content-per-vehicle is now the single most powerful growth lever in the automotive components sector.

Market Sizing and Growth Trajectory

The automotive thermal management systems market has entered a phase of sustained, structurally-driven expansion. The 2026 global market is valued at approximately USD 71.7 billion, with forecasts projecting growth to USD 97.0 billion by 2033. While the compound annual growth rate of 4.4% appears moderate, it masks a fundamental recomposition of the market, as legacy ICE cooling demand plateaus and is progressively replaced by high-value EV thermal architectures.

Two forces are compounding growth beyond what headline vehicle production numbers would imply. First, the thermal content per vehicle is expanding as OEMs adopt unified, multi-loop thermal platforms, the value of thermal systems per unit is rising faster than vehicle volumes. Second, the battery thermal management sub-segment is on a materially steeper trajectory. Having reached approximately USD 5.1 billion in 2025, this segment is growing at a CAGR exceeding 23% and is projected to approach USD 26.9 billion by 2033, driven by the need for active liquid cooling, advanced heat pump integration, and thermal safety compliance.

From a regional standpoint, Asia-Pacific dominates with approximately 41% of global revenue, driven by China, Japan, and South Korea being home to both the largest EV production bases and the leading thermal component manufacturers. North America accounts for roughly 35–40% of market value, buoyed by large vehicle formats (SUVs, pickup trucks) that require more intensive thermal solutions. Europe is the fastest-evolving regulatory environment, with Euro 7 emission standards and ambitious decarbonization targets driving adoption of advanced HVAC and cooling architectures.

The Electrification Catalyst: Why EVs Are Rewriting Thermal Economics

The transition from ICE to electrified powertrains is not simply adding thermal complexity; it is fundamentally restructuring the thermal architecture of the vehicle. An internal combustion engine generates enormous waste heat, but its thermal management requirements are well-understood and component costs are relatively modest. An EV, by contrast, must actively manage heat across multiple and interdependent subsystems, i.e. the battery pack, power electronics, electric motors, and cabin climate each with narrower temperature tolerances and higher consequences of thermal failure.

1. Battery Thermal Management: The Core Value Driver

Lithium-ion battery cells operate optimally within a narrow window of 20–40°C. Deviations in either direction degrade performance, reduce cycle life, and in extreme cases trigger thermal runaway, a cascading exothermic failure that remains the most significant safety concern in EV engineering. Active liquid cooling has become the industry standard for mid-range and premium EVs, offering more precise and uniform temperature control than air-based alternatives.

Effective thermal management directly impacts the metrics that matter most to consumers and OEMs alike: driving range, charging speed, and battery warranty cost. Systems that improve thermal efficiency by 20% can extend battery lifespan by up to 30%, translating into material reductions in warranty reserves and total cost of ownership. For OEMs competing on range and reliability, thermal engineering is increasingly a source of competitive differentiation rather than commodity procurement.

2. Heat Pump Integration and Cabin Efficiency

The shift to heat pumps which capture and redistribute waste heat from the drivetrain to warm the cabin is one of the most consequential technology adoptions of the past three years. Traditional resistive heaters in early EVs consumed substantial battery energy, particularly in cold climates, reducing winter range by 30–40%. Advanced heat pump systems, such as those developed by Valeo and Hanon Systems, dramatically improve energy utilization by harvesting thermal energy that would otherwise be rejected to ambient air.

Nissan’s 2026 LEAF exemplifies this approach, incorporating a thermal management system that captures waste heat from the motor and onboard charger to maintain battery temperature in cold conditions. Valeo’s CES 2026 Innovation Award-winning compact 5-Way Refrigerant Valve demonstrates how integrated, software-controlled valve systems can route heat flows across multiple loops, optimizing energy use in real time.

Technology Frontiers: From Radiators to Intelligent Thermal Architectures

The technology roadmap for automotive thermal management is advancing along several parallel vectors, each with distinct implications for component suppliers, system integrators, and vehicle OEMs.

1. Unified Multi-Loop Thermal Platforms

Leading OEMs and suppliers are converging on unified thermal architectures that integrate battery cooling, powertrain thermal control, and HVAC into a single, software-managed system. Approximately 65% of major OEMs are now designing multi-loop thermal platforms for their next-generation EV architectures. These unified systems reduce the number of discrete components, lower weight, and enable dynamic thermal load balancing. For instance, pre-conditioning the battery during regenerative braking or diverting excess cabin heat to warm the battery pack in cold starts.

2. AI-Driven Predictive Thermal Control

Smart thermal control systems using sensor arrays and machine learning algorithms are moving from concept to production. MAHLE and DENSO are both investing in AI-enabled thermal controllers that anticipate thermal loads based on driving patterns, ambient conditions, route topology, and charging schedules. These systems shift thermal management from reactive temperature regulation to predictive energy optimization, extracting measurable range gains and reducing component stress.

3. Advanced Materials and Phase-Change Technologies

Beyond system-level architecture, materials science is opening new performance envelopes. Phase-change materials that absorb and release latent heat at specific temperatures are being explored for passive battery thermal buffering, particularly for plug-in hybrids and urban-duty EVs where active cooling may be oversized for typical operating conditions. Meanwhile, next-generation coolants and refrigerants with lower global warming potential are being mandated by evolving environmental regulations, adding another dimension to supplier R&D agendas.

Competitive Landscape: Who Is Winning and Where

The automotive thermal management market is concentrated among a handful of globally scaled Tier-1 suppliers, each with distinct strengths in geography, technology, and customer relationships. DENSO Corporation (Japan) leads with an estimated 18–22% market share in EV thermal systems, followed by Valeo (France), MAHLE GmbH (Germany), Hanon Systems (South Korea), and BorgWarner (USA). Robert Bosch, Continental AG, and Modine Manufacturing occupy significant but narrower positions.

The competitive dynamics are noteworthy for several reasons. Japanese and European suppliers continue to hold the highest market shares, reflecting decades of embedded OEM relationships and deep systems integration capabilities. However, Chinese suppliers such as Sanhua Intelligent Controls and Yinlun Machinery are scaling rapidly, leveraging cost advantages and proximity to the world’s largest EV production base. The emergence of Chinese thermal component providers as credible alternatives to established Western and Japanese incumbents is among the most consequential competitive shifts in the sector.

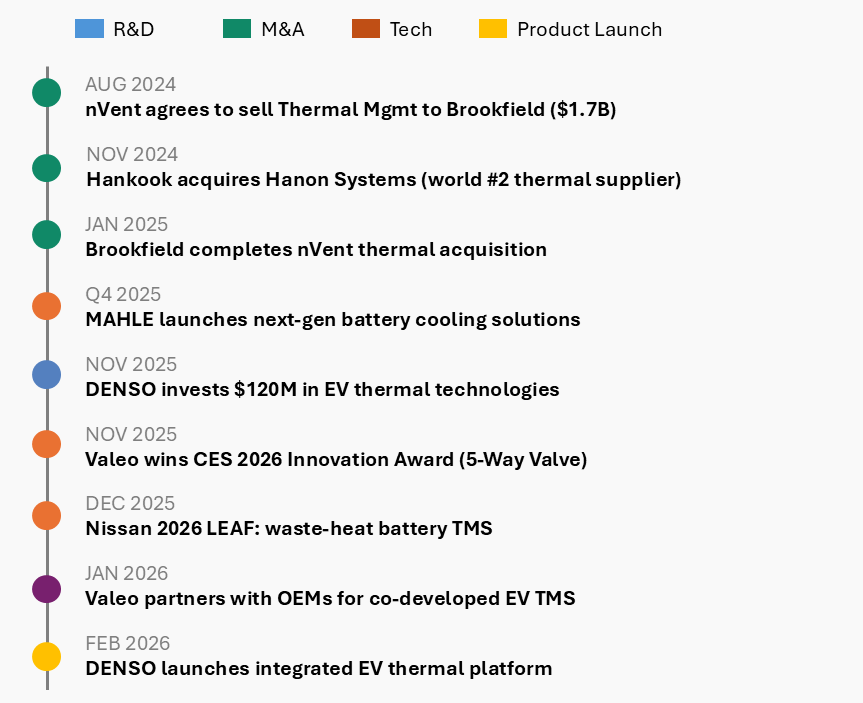

Hanon Systems’ acquisition by Hankook & Company Group in January 2025 reshaped the competitive map by combining the world’s second-largest thermal management supplier with Hankook’s tyre and energy storage capabilities, creating a vertically integrated mobility platform spanning rolling resistance, thermal systems, and battery technology.

Strategic Activity Tracker: M&A, Joint Ventures, and Market Expansion

The strategic activity in automotive thermal management over the past eighteen months has been intense and directionally significant. Corporate development teams across the sector are deploying capital through acquisitions, divestitures, joint ventures, and targeted R&D investments, each reflecting a clear thesis about where value is migrating within the thermal value chain.

Recent Strategic Transactions and Developments (Aug 2024 – Feb 2026)

Landmark Transactions

Hankook & Company Group / Hanon Systems: Completed in January 2025, this acquisition gave Hankook full ownership of the world’s second-largest automotive thermal management provider, with 40 manufacturing sites in 19 countries. The strategic thesis centers on creating a unified mobility platform integrating tyres, batteries, and thermal management. A portfolio uniquely positioned to serve EV OEMs with a systems-level value proposition.

nVent / Brookfield Asset Management: In January 2025, Brookfield completed its USD 1.7 billion acquisition of nVent’s Thermal Management business, which includes the RAYCHEM and TRACER brands. The transaction signals private equity’s conviction in mission-critical thermal solutions, with Brookfield positioning the standalone business for accelerated growth in data centers and industrial applications alongside automotive adjacencies.

Robert Bosch / Johnson Controls-Hitachi HVAC JV: Bosch’s acquisition of the HVAC solutions business from the Johnson Controls–Hitachi joint venture represents a USD 4.6 billion bet on convergence across building, industrial, and automotive thermal systems. Bosch is increasingly leveraging shared sensor, compressor, and control technologies across these domains.

Technology Partnerships and R&D Investment

DENSO: Invested USD 120 million in November 2025 in advanced thermal management technologies for EVs, encompassing automated climate and battery control systems. In February 2026, DENSO launched a fully integrated EV thermal platform designed for system-level efficiency gains.

Valeo: Won the CES 2026 Innovation Award for its compact 5-Way Refrigerant Valve for EV heat pump systems and entered co-development partnerships with major OEMs for next-generation thermal platforms. Valeo’s compact heat pump units, launched in December 2025, target space and energy optimization in smaller EV architectures.

MAHLE: Expanded battery cooling solutions through new product launches and entered joint ventures to globalize its thermal system technologies. MAHLE’s smart thermal control systems, integrating sensors and AI, entered production validation in late 2025.

Strategic Implications for Industry Stakeholders

1. For OEMs

Thermal management can no longer be treated as a procurement line item delegated to purchasing teams. It is a platform-level architecture decision with direct implications for range, charging speed, warranty cost, and brand perception. OEMs that co-develop integrated thermal platforms with their Tier-1 partners rather than sourcing discrete components will realize superior system efficiency and faster time-to-market.

2. For Tier-1 Suppliers

The competitive landscape is bifurcating. Suppliers with full-system integration capabilities spanning compressors, valves, heat exchangers, controls software, and sensors are capturing disproportionate value. Those limited to single-component offerings face commoditization pressure, particularly as Chinese suppliers scale global operations. M&A, joint ventures, and technology partnerships are not optional strategies; they are survival imperatives.

3. For Investors and Private Equity

The thermal management sector offers a compelling investment thesis: structural demand growth underpinned by regulatory mandates and electrification tailwinds, a consolidating supplier landscape with clear platform winners, and increasingly software-defined product architectures that create recurring revenue and differentiation moats. The Brookfield/nVent and Hankook/Hanon transactions demonstrate that sophisticated capital is already moving at scale.

4. For Technology Entrants

Startups and adjacent-industry players bringing capabilities in AI-driven controls, advanced materials, sensor fusion, or data center thermal expertise have a genuine window of opportunity. The transition from mechanical to intelligent thermal systems is creating adjacencies that did not exist five years ago. The key to market entry is not product innovation alone, but the ability to integrate into the automotive qualification and validation ecosystem.

Conclusion: From Supporting Role to Strategic Centre

The automotive thermal management sector is no longer a quiet corner of the automotive supply chain. It is a USD 71.7 billion market with a structurally rising trajectory, driven by forces that are durable, regulatory, and technology led. Companies that master integrated thermal architectures combining hardware precision with software intelligence will occupy pivotal positions in the next generation of mobility platforms.

For decision-makers across the automotive and mobility value chain, the message is clear: thermal management has graduated from an engineering function to a strategic function. Capital allocation, partnership strategy, and technology roadmaps must reflect this shift.